Advertisement

The Art of Understanding 401(k) Plan Fees

Understanding 401(k) plan fees has become a hot topic in recent years. But, in today’s volatile economy—where every dollar counts and is counted— it’s not more important than ever to understand, document, and monitor such fees.

In fact, 401(k) plans are increasingly viewed by many as their primary source of retirement income. This is especially true with the younger generation, who fear that Social Security may not live as long as they will.

Today’s 401(k) industry has grown to more than 60 million participants, $3 trillion in participant assets, and $30 billion in annual fees.

The Employee Retirement Income Securities Act (ERISA) established rules that govern 401(k) plans and the responsibilities for those offering the plan — the plan sponsors and fiduciaries (those with discretionary authority or control over the plan assets or administration).

This authority over plan assets does not refer to investment managers, but rather to plan sponsors — those individuals who decide which funds will be allowed or offered in the 401(k) plan. If a broker is involved, he or she is usually not considered a fiduciary and will explicitly disclaim and fiduciary responsibility.

Fiduciary Responsibilities Under ERISA

Section 404(a) of ERISA is very clear regarding fiduciary responsibilities.

First, fiduciaries are to make all decisions solely in the interest of the participants and beneficiaries for the exclusive purpose of: 1) providing benefits to the participants and 2) defraying the reasonable expenses of administering the plan.

Second, fiduciaries are held to the standards of a “prudent expert” when carrying out their duties. Third, they are charged with diversifying the plan’s assets to minimize the risk of large losses.

In a participant-directed plan, this charge would address the funds offered to participants. Lastly, fiduciaries manage the plan in accordance with the plan documents and instruments — as long as those documents are consistent with ERISA.

ERISA consultant and employee benefits attorney Fred Reish states: “Plan fiduciaries need to invest the same level of due diligence in the execution of their fiduciary responsibilities as they would choosing a doctor or a surgeon for a family member.”

ERISA Requires Prudence

ERISA does not require that plan sponsors purchase the cheapest 401(k) provider or consultant. However, it does require that plan sponsors have a prudent process to determine what is in the best interest of their participants. Plan sponsors should:

- Examine the existing plan in order to understand the components of the total plan costs; determine how much is currently paid and to whom; and request itemized documentation of services and fees.

- Compare providers and services, and take into account fee methodology and how fees change over time.

- Establish a consistent process to periodically benchmark 401(k) costs. This may take the form of a fee and investment benchmarking or a full RFP. Both approaches should include some form of investment quality comparison.

Just as construction company executives are expected to understand the costs associated with projects, plan sponsors are expected to understand the fees 401(k) participants will incur as a result of their decisions. Defraying the reasonable expenses of administering the plan implies that plan sponsors understand what is currently being paid.

Unfortunately, this is often not the case. In addition, legal battles and new disclosure requirements have recently come into play. In the fall of 2006, a number of lawsuits were filed on behalf of participants against plan sponsors charging a breach of fiduciary duty surrounding the fees that plan sponsors allowed plan participants to pay.

These recent lawsuits imply that plan fiduciaries should not only be responsible for determining the reasonableness of fees, but also for disclosing, monitoring, and negotiating them.

Types of Plan Fees

The three components of 401(k) plan costs are administrative, plan consulting, and investment fees.

Administrative fees encompass all fees that are not directly related to managing the investment and include recordkeeping, technology, trustee, compliance and legal documentation, and employee communication.

Plan consulting fees include any and all compensation paid to an advisor or broker. Advisors (typically registered investment advisors) are paid an advisory fee and, in many cases, act as investment fiduciaries. Brokers are paid a commission and, as previously mentioned, do not act as investment fiduciaries.

Investment fees include all revenue collected from the investment vehicles. This includes a registered mutual fund expense ratio or a subadvised fund management fee.

How Fees are Paid

Administrative fees are paid by either the 401(k) participant or the plan sponsor. Investment fees are (in most cases) paid by plan participants. In practice, most total 401(k) plan costs are paid by plan participants. It should also be noted that as plan assets increase, so do the percentages of fees paid by participants.

For plans with assets greater than $250 million, participants pay 99 percent of plan costs. Unfortunately, if asked today, most plan sponsors cannot enumerate how much participants are paying. Yet in most cases, participants pay the majority of their total plan costs. It’s easy to see why the fiduciary requirement of reasonableness is so important to these participants.

ERISA Requires Reasonable Fees

ERISA does not require that the plan sponsor pay reasonable fees; fees that the company pays are not a fiduciary matter. However, ERISA does require that the fiduciaries ensure that participants pay no more than reasonable fees. Therefore, plan sponsors typically pay only a small amount of fees.

Trends

The Good News: Over the last 10 years, total plan costs have been on the decline. This can be attributed to asset growth, competition driving margins lower, and more efficient recordkeeping. These changes have allowed industry and plan sponsors to shift some or all of the administrative fees to plan participants, while lowering total plan fees.

The Bad News: Most plan providers have adopted pricing strategies that charge minimal or no administrative fees to plan sponsors and that provide little disclosure of the proposed total cost of the plan.

What Drives 401(k) Pricing?

What makes one plan more or less expensive than another? After identifying the categories of fees and who pays them, the next step is to discuss the primary drivers of 401(k) pricing.The first two drivers (plan service and consulting fees) are probably the most obvious and easiest to understand. The remaining two drivers (plan assets and average account balance) are related to demographics.

Nonstandard Investments

It would be expected that a construction project that was unusual in scope would require additional revenue. Similarly, any fund or vehicle that creates additional demands on the service provider’s recordkeeping system increases plan fees.

Outside guaranteed income contracts (GICs) that are not manufactured by or proprietary to the service provider are in this category, as are employer stocks or funds not normally available on the provider’s platform.

For example, a plan sponsor decides to move its recordkeeping from Provider X, but continues to use Provider X’s index fund as an investment option within the plan. (These services are typically available for larger plans, but at a cost.)

Plan sponsors should carefully consider the benefits and costs of offering these investments to determine if they are appropriate from a fiduciary standpoint.

Multiple, Complicated, or Antiquated Payroll Transmittals

Data submitted through non-electronic methods or by plans with multiple payroll systems, locations, and/or frequencies typically generate additional recordkeeping fees.

Onsite Employee Meetings at Multiple Locations

Labor and travel are expensive in both the construction and 401(k) industries. Labor and travel to deliver onsite group or individual enrollment and investment education meetings are a direct cost to the provider. Plan fiduciaries should evaluate the use of onsite meetings vs. other potentially more efficient ways to communicate (such as Webinars or teleconferences).

Investment Management Objectives

Passively managed funds that track an index (index funds) generally have significantly lower management fees than actively managed funds (whose objective is to outperform a certain benchmark, index, or asset class). Any analysis of index vs. actively managed costs should include an “apples to apples” comparison of investment options for both quality and approach.

Investment Advice

Many providers offer online investment advice, usually delivered through a third-party firm. Fees typically range for 0.3 percent to 1 percent or more of the employee account balance. Although these fees are only applied to participants who use this service, fiduciaries should consider these fees when selecting a service provider.

Consulting Fees

Following ERISA, plan fiduciaries should first establish relevant criteria to evaluate a potential consultant’s capabilities and services. This often becomes difficult, since many brokers are simply priced into a provider quote with little or no explanation of fiduciary status and services.

Also, unless the plan sponsor is invoiced directly by the consultant, the consulting fees are likely built into the investment expense.

Because plan consulting fees must be reasonable, fiduciaries must determine how much of the investment fees are related to actual plan investment management, services and administrations, and consulting. So, fiduciaries should read the compensation disclosure document provided by the plan consultant and ask the consultant to produce an itemized list of services and related fees.

Plan Assets and Average Account Balance

These two items are generally the most significant demographic factors that impact 401(k) plan pricing because they affect both the costs of providing services and provider revenue.

For example, let’s say a plan has $5 million in assets and 200 participants, with an average per participant balance of $25,000. From this cost perspective, the provider will have to keep records of participant files, process phone calls, and provide communication materials (statements, flyers, notices, etc.) for 200 participants.

In the 1980s and 1990s, many 401(k) provider pricing structures were inversely proportional to the number of plan participants. In an effort to build market share, many providers offered lower pricing to plan sponsors with more employees, regardless of plan size or average account balance.

This led more than 100 providers to exit the 401(k) recordkeeping business. Recently, providers have begun to consider the costs associated with each 401(k) plan participant and price accordingly. This change has driven many providers to offer “revenue per participant” pricing models that are based on plan assets and average account balances.

If plan sponsors pursue this type of pricing model with their current/potential providers, then the providers typically convert the revenue to an asset-based fee once the “revenue per participant” is negotiated. This asset-based fee may either be built into the investment expense or charged against the assets, in addition to the investment expense.

How Asset and Average Account Balances Affect Pricing

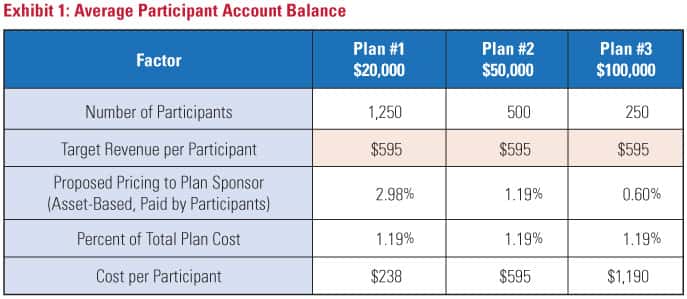

In Exhibit 1, a provider creates pricing models for three different 401(k) plans, each with $25 million in plan assets. Let’s assume that the provider has agreed to $595 as the required “revenue per participant.”

For plan #2, $595 per participant equals a total asset management fee of 1.19 percent in the first year. A plan sponsor who deducts $595 from participants’ accounts would be inundated with complaints, yet the implicit asset-based fee that is deducted from participants’ accounts goes unnoticed.

In fact, plan participants and all mutual fund investors are much more accepting of asset-based fees than direct participation fees.

As further shown in Exhibit 1, it’s obvious why average account balance is the key driver of plan pricing. A 1.19 percent total asset-based fee generated only $238 per participant for a plan with a $20,000 average account balance. Yet, a plan with the same asset-based fee and an average account balance of $100,000 generates an average revenue of $1,190 per participant.

This is one of the many reasons why it’s important for plan sponsors to benchmark fees and services and their plan demographics change.

Revenue Sharing

Now that we’ve discussed the components of total plan costs and the drivers that impact pricing, the question that remains is: “How do providers receive revenue?” The answer is as simple as “revenue sharing,” yet as complicated as the numerous forms that revenue sharing can take.

Revenue sharing includes any payments made by investment managers from revenue generated from the expenses of the fund and paid to service providers or consultants.

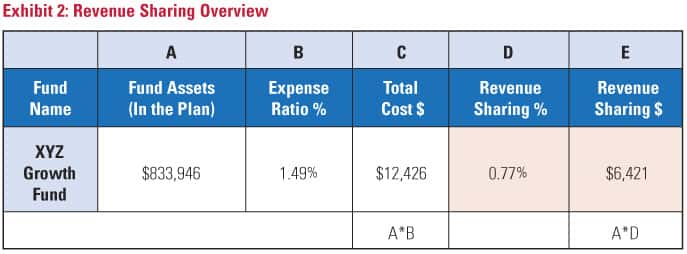

Based on Exhibit 2, the 401(k) plan participants are paying $12,426 for $833,946 invested in the XYZ Growth Fund. In this case, the service provider is receiving $6,421, and the remaining $6,005 is the net management fee retained by XYZ.

Revenue sharing may appear in the form of revenue paid by the service provider to the plan consultant/broker or third-party administrator (TPA). It could also be revenue that is applied to offset plan service fees.

The common thread to revenue sharing is that it is generated through the investment management expenses and paid to other parties.

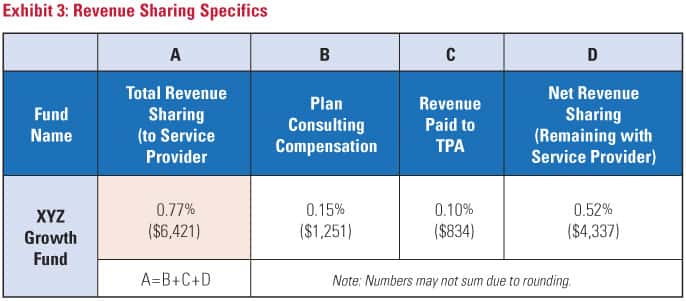

Exhibit 3 provides a hypothetical breakdown of the 0.77 percent revenue sharing illustrated in Exhibit 2. Taken together, they illustrate that a 1.49 percent investment management fee results in 0.77 percent of gross revenue sharing to the service provider, of which 0.15 percent is paid to the plan consultant and 0.10 percent is paid to the TPA.

Exhibit 2 illustrates the presence and amount of revenue sharing, while Exhibit 3 details the parties and amounts of revenue sharing received. In the past, some revenue sharing information was not readily available, but recent disclosure requirements allow plan sponsor more access. Even so, cash instruments (such as GICs) still present a level of complication when trying to determine true revenue sharing.

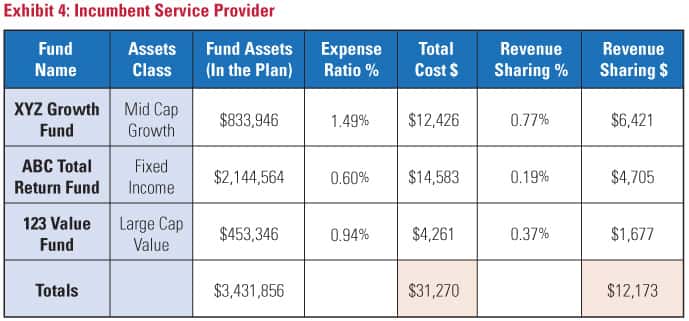

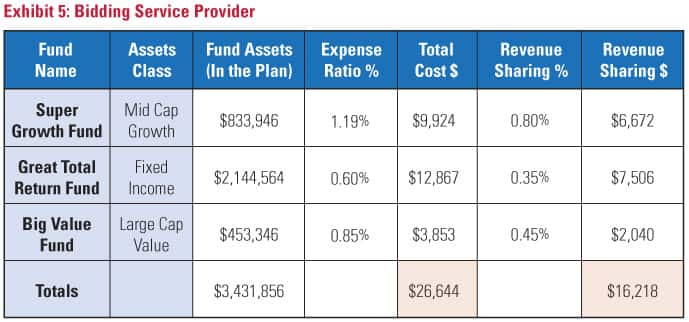

Exhibits 4 and 5 examine total cost and revenue sharing comparisons for a hypothetical 401(k) plan with $3,431,856 in plan assets. The bidding provider has 14.8 percent lower total costs; however, the incumbent provider has 33.2 percent higher net revenue.

In other words, the bidding provider’s total expenses compared to the plan sponsor are lower, but its net revenue is higher. An obvious question is how can Super Growth Fund (with an expense ratio of 1.19 percent) pay a revenue share of 0.80 percent while XYZ Growth Fund (with an expense ratio of 1.49 percent) pays a lower revenue share?

One issue that can affect revenue sharing is whether the fund is issued by the provider (a proprietary fund). In many cases, proprietary funds pay a higher revenue share back to the provider than “outside” fund options. If a fund is well-known, its managers may choose not to pay a high revenue share, leveraging its name recognition instead.

Share Classes

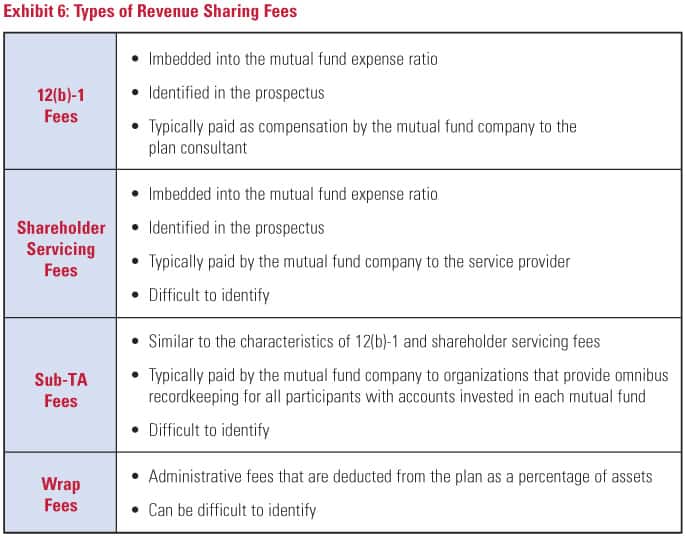

Exhibit 6 details four types of revenue sharing fees. Many investment providers (mutual fund companies and financial service firms) offer several versions of the same fund with different expense ratios (management fees); these are known as share classes.

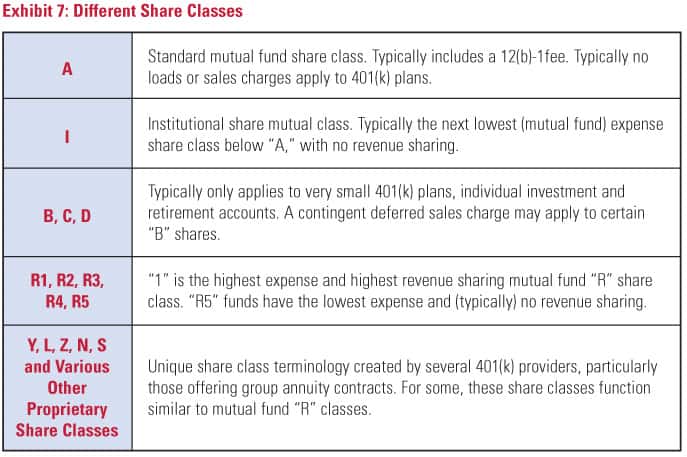

Exhibit 7 describes at least 15 different 401(k) share classes. Multiple share classes were created to allow service providers more expense collection flexibility based on the growing demands of plan sponsors.

Historically, participants have paid an average of 95 percent or more of total 401(k) plan expenses. What happens over time? As plan assets grow, so does provider and consultant/broker revenue, which explains why plan sponsors should conduct a fee benchmark every three to five years, or as demographic changes take place in the plan.

Conclusion

The market declines of 2008 have decreased plan assets by as much as 25 percent or more. Provider revenue has declined as well, but taking participant deferrals into consideration, plan assets can rebound surprisingly quickly.By understanding, documenting, and monitoring plan fees, plan sponsors and other fiduciaries can comply with ERISA 401(a) and keep 401(k) plans on the right track for the benefit of the plan participants.