Advertisement

Delivering Financial Wellness: How to move from 'idea' to 'action.'

Mark Singer, CFP®, President and Founder, Financial Literacy Toolbox will present on financial wellness at PSCA’s 71st National Conference. Click here for the full agenda.

Financial Literacy Challenge

Financial stress may be the result of Ineffective personal financial management and poor financial habits. Seventy-one percent of surveyed Americans report they would have some or significant difficulty coping with a one week delay in their next paycheck.1 Forty-four percent say they either could not cover an emergency expense costing $400 or would cover it by selling something or borrowing money.2 In one study, less than one third could correctly answer three relatively simple financial literacy questions.3 This lack of financial capability may show up in benefit plan participation. For example, one survey of 4+ million workers showed over 1 million missed out on an estimated $1.4 billion in employer match. The authors then estimated if the same results applied to all Americans who participate in a retirement savings plan, an estimated $24 billion/year of employer match is left on the table each year!4

Employer Response to Date

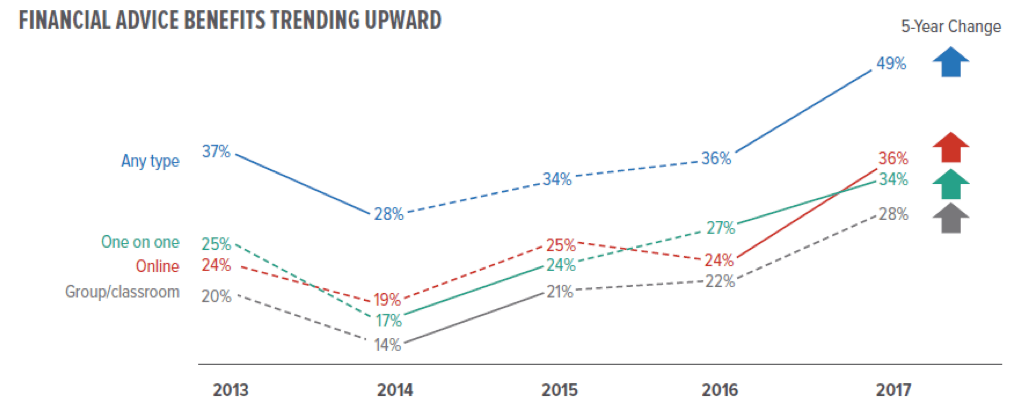

The Society for Human Resource Management reports significant increases in employer-provided financial wellness:5

The concept of “financial wellness” or “financial advice” includes quite a diversity of programs but is generally thought to include education and/or counseling on topics beyond the life events typically addressed by traditional employee benefit plans – life, disability, medical, retirement (savings and investments). The diversity of services offered by providers is significant including but not limited to: financial self-assessments, tools to create/track financial progress, customized financial education, advice on financial privacy and security, college savings, debt management, etc.

Potential First Steps

As a plan sponsor, concurrent with or prior to introducing a financial wellness initiative, you may want to give your traditional benefit plans a wellness checkup. Yesterday, today and tomorrow, your enterprise has likely made a significant investment in traditional benefits. Leadership will want you to confirm participation in those plans is optimal.

Don’t overlook the many examples of financial wellness innovations and opportunities possible in traditional benefit plans – particularly in your retirement savings plan6. Some places to start might include7:

- Retirement Savings (IRC §401(k)) – Improving participation and contributions through perennial automatic enrollment and escalation for all eligible employees, adopting a qualified default investment alternative, updating plan loan provisions to 21st Century functionality (electronic banking, line-of-credit structure, etc.) so that it might effectively address emergency and student debt repayment needs, eliminating hardship withdrawals, etc.

- Educational Assistance (IRC §127) – Improve/market the opportunity for workers to acquire or improve work-related skills to increase their most valuable asset (the ability to earn a living), defray student loan debt, etc.

- Paycheck Insurance (IRC §79, IRC §105) – Increasing participation in life and disability coverage,

- Emergency Assistance (IRC §7872) - Compensation loans selectively made available for emergency assistance (auto repair, meeting health plan deductible, advance for educational assistance, etc.)

- Health Savings Accounts (IRC §223, IRC §125) – Choice architecture (behavioral economics) in terms of health coverage and contribution defaults to encourage preparation and saving for future medical/long term care premiums, as well as long term care and other out of pocket medical expenses.

If you have questions or wish to discuss, contact me at [email protected].

1. Getting Paid in America, 2017, American Payroll Association, http://www.nationalpayrollweek.com/documents/2017GettinngPaidInAmericaSu...

2. Report on the Economic Well-Being of U.S. Households in 2016, Board of Governors of the Federal Reserve System, May 2017. In 2013, the same survey confirmed 50% of Americans indicated they could not accommodate a $400 expense. https://www.federalreserve.gov/publications/files/2016-report-economic-w...

3. Olivia S. Mitchell and Annamaria Lusardi, Financial Literacy and Economic Outcomes: Evidence and Policy Implications, January 2015. Their three questions were: (1) Suppose you had $100 in a savings account and the interest rate was 2% per year. After 5 years, how much do you think you would have in the account if you left the money to grow? (More than $102, Exactly $102, Less than $102, Do not know/Refuse to answer); (2) Imagine that the interest rate on your savings account was 1% per year and inflation was 2% per year. After 1 year, how much would you be able to buy with the money in this account? (More than today, Exactly the same, Less than today, Do not know/Refuse to answer); and 3) Please tell me whether this statement is true or false. “Buying a single company’s stock usually provides a safer return than a stock mutual fund.” (True, False, Do not know/Refuse to answer). http://pensionresearchcouncil.wharton.upenn.edu/wp-content/uploads/2015/...

4. Financial Engines, Missing out: How much employer 401(k) matching contributions do employees leave on the table? May 2015, https://financialengines.com/docs/financial-engines-401k-match-report-05... See also: https://www.psca.org/blog_jack_2018_6

5. Society for Human Resources Management, 2017 Employee Benefits: Remaining competitive in a Challenging Talent marketplace,https://www.shrm.org/hr-today/trends-and-forecasting/research-and-survey...

6. J. M. “Jack” Towarnicky, My Financial Wellness Solution: The 401(k) as a Lifetime Financial Wellness Solution, Society of Actuaries, May 2017, https://www.soa.org/essays-monographs/2017-financial-wellness-essay-coll...

7. Always check with tax and legal counsel before taking any action. We are providing this information to you solely in our capacity as individuals with knowledge and experience in the industry and not as legal advice. The issues presented here may have legal implications, and we recommend discussing this matter with your tax and legal counsel prior to choosing a course of action. This publication was prepared to support the informational needs of the Plan Sponsor Council of America and its members on the issues discussed. The publication focuses on the needs of our association and the issues of interest to association members. The publication is not and should not be used as a substitute for legal, accounting, actuarial, or other professional advice.