Advertisement

The "Other" Retirement Planning Model (First of a Series)

In my last plan sponsor role, I very much enjoyed one of my work assignments - leading a pre-retirement planning seminar. It was offered at least five times a year. It was a two day affair, offsite, with food and spirits. Most attendees had long service. They usually were in their mid-50’s and had 15, 20, 25 or more years of participation in our 401(k) plan. That employer also offered, then and now, a defined benefit pension plan and employer financial support for retiree medical coverage. So, most in attendance had successfully prepared (at least financially) for retirement.

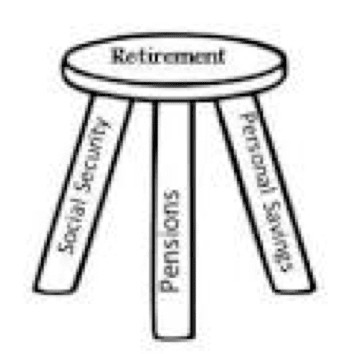

I had joined that enterprise in my mid-30’s with no accrued, vested pension nor had I accumulated retirement savings. A few in the audience had also joined our firm after service elsewhere. So, I added a second, non-traditional retirement planning model (with many retirement income sources) to my predecessor’s traditional three legged stool. Picture this:

|

|

The three legged stool was always deemed better. Why? Because a three-legged stool is guaranteed not to wobble - the ends of its legs always form a plane … even on an uneven floor or where the legs are not all exactly the same length. However, a stool with four or more legs must be on level ground – or it will wobble. It’s math. As time goes on, more and more workers I meet can’t rely on that traditional three-legged stool. Like me, they end up with the other retirement planning model. Income is needed from a variety of sources. When I presented this material, I would have an artist draw a perfectly balanced three-legged stool on the flipchart. After explaining that model, I would then draw my own (I have no artistic capability), then add one leg after another. I had a lot of fun with my wife Debbie’s benefits and income (she must continue working to support my retirement). My presentation ended with two jokes – don’t rely on mom and dad (inheritance) nor count on lottery winnings as a retirement income source.

Last week, I had the privilege of attending the “2018 Housing Wealth in Retirement Symposium.” Dr. Laurie Goodman confirmed the size of senior’s home equity marketplace - 26 million American households age 65 or older with median household net worth of $319,250, where $143,400 is in the form of home equity (45%).1 We also heard from Dr. Wade Pfau on how the home equity from a reverse mortgage can make all the difference when a retiree is confronted with “sequence of returns” investment risk in the years soon after retirement.2

Because home equity is such a large part of assets in retirement, you should expect more of your participants will want to consider accessing home equity. So, you may want to incorporate housing choices (downsizing, accessing home equity, etc.) in pre-retirement planning or financial wellness programs – to highlight the opportunity the reverse mortgage may present to the Baby Boomer and future generations.

1. Laurie Goodman, Founder and Co-director of the Housing Finance Policy Center, Urban Institute.

2. Wade Pfau, Using Reverse Mortgages In A Responsible Retirement Income Plan, February 27, 2017. The sequence of returns on an asset portfolio can significantly impact retirement income. Two retirees with identical wealth can have entirely different outcomes – even if investments have the same average return over time. So, “… coordinating retirement spending from a reverse mortgage reduces strain on the investment portfolio … Reverse mortgages can help sidestep this (sequence of returns) risk by providing an alternative source of retirement spending after market declines, creating more opportunity for the portfolio to recover.” Accessed 20180326 at: https://retirementresearcher.com/using-reverse-mortgages-responsible-ret...