Advertisement

Sidecar = Suboptimal

Perhaps you noticed the recent proposal which would authorize a plan sponsor to use automatic features in creating so called “sidecar” savings account for financial emergencies.1 Contributions would be taken on an after-tax basis and invested in capital preservation investments. The account could be a part of or separate from the tax-qualified plan.

Few plan sponsors have adopted existing, available “sidecar” accounts.2 Recent experience with MyRA suggests most financial institutions will not be interested in creating/maintaining “sidecar” accounts.3 There is nothing in this proposal that would likely change that outcome. More importantly, a “sidecar” is suboptimal. It would not qualify under the “standard” set by the General Accountability Office (GAO) as “the most appropriate and least damaging option.”4 Many of today’s individual account retirement savings plans already deploy better options for financial emergencies.

One More Time – Our “Retirement Savings Crisis”

This is another proposal designed to address what some are deeming the “retirement savings crisis.” Many claim a “retirement savings crisis” is looming as many Baby Boomer workers reach traditional retirement age without accumulating assets sufficient to maintain their pre-retirement standard of living.5 Whether or not you agree that we are in “crisis” mode,6 most other policy proposals to date have focused on the more impactful issues workers face in the retirement savings accumulation stage:

- A lack of access to an employer-sponsored retirement savings plan during a portion of their working career,

- Eligible participants decisions to forego participation, or

- Participant contribution percentage elections that are too low to accumulate sufficient assets.

The “sidecar” proposal is focused on the substantial leakage from retirement savings plans from hardship withdrawals, and post-separation, pre-retirement distributions.7 Leakage is any pre-retirement withdrawal of retirement savings.

Importantly, unless plan sponsors take action to curtail or eliminate hardship withdrawals, legislation that takes effect in 2019 will likely trigger increases in the number of hardship withdrawals and more leakage of retirement savings.8 In my last plan sponsor role, I removed in-service, hardship withdrawals in 1996, coincident with adding 21st Century loan processing (electronic banking) so, after separation, participants could not only continue loan repayments but could also initiate a tax-preferred loan. The result: leakage was dramatically reduced.

Because the “sidecar” requires action by plan sponsors and because it would divert monies and attention from more significant issues affecting participation in the qualified plan, many, perhaps most plan sponsors won’t adopt these provisions. For comparison, most plan sponsors have not adopted existing “sidecar” accounts where monies would be more readily available for emergency purposes. Only a few adopted the Deemed IRA - available for the past sixteen years.9 Most 401(k) plans do not permit non-Roth, after-tax contributions.10 There are no limits on accessing funds from Deemed IRA “sidecar” accounts. And, plans that permit after-tax contributions will typically limit withdrawals of those monies to meet financial emergencies, sometimes subject to completing a specified period of service of as little as two years.

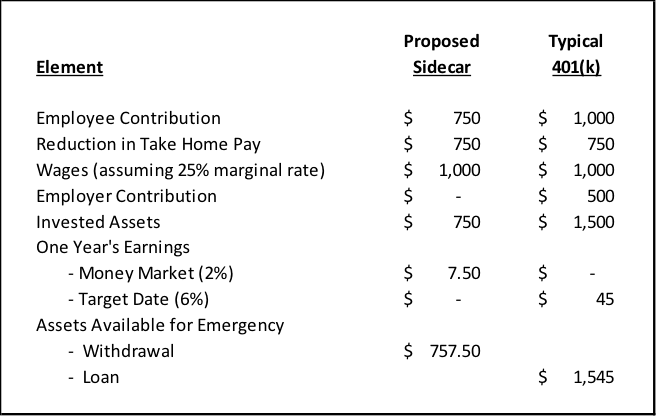

So, deemed IRA and non-Roth, after-tax contributions can offer easy access to assets to respond to emergencies using existing 401(k) and IRA functionality - without the hassle of creating a separate, side-car account. More importantly, those “sidecar” accounts won’t divert monies or attention from the qualified plan, nor do they limit investments to capital preservation. So, “sidecar” accounts are already available. But, some plans already offer a better alternative. Consider the following comparison11:

So, by leveraging tax preferences and employer financial support, a participant will have much greater capacity to deal with emergencies at the same reduction in take-home pay. Just as important, money was not diverted for an emergency that may never arise or for an emergency that might be met through other means. In other words, the proposed “sidecar” is suboptimal.

Some will criticize plans that use 401(k) loans in this manner because loans must be repaid. Comparatively, the “sidecar” account would be automatically “replenished.”

Others criticize the use of loans because few plans provide for repayment after separation.

Some might find fault with the above comparison since the 401(k) includes employer contributions - that workers would fund the emergency account only after contributing enough to receive the full employer contribution. However, surveys show that as many as half of all participants do not contribute enough to receive the full employer contribution.12 Perhaps some divert monies in anticipation of emergencies.

Other criticisms might include claims that workers will borrow excessively. That has not been our experience. More importantly, loans are not leakage, unless they are not repaid. Loans need not result in lower investment returns – and may actually increase household wealth. Further, liquidity via plan loans may increase retirement savings – because participants won’t have to restrict their contributions to what they believe they can afford to earmark for a distant, future retirement.13

Got better ideas on how to reduce leakage? Send them in: [email protected]

1S.3218, Strengthening Financial Security Through Short-Term Savings Act. “… An employer may make available to employees a stand-alone, short-term savings account, using an automatic contribution arrangement … An employer that offers employees a short-term savings account shall deduct amounts from each participating employee's wages … and transfer such amounts to a savings account ...” Accessed 7/25/18 at: https://www.congress.gov/bill/115th-congress/senate-bill/3218/text

2R. Steyer, UNMET, Deemed IRA’s potential untapped by DC plans, 5/2/11. Accessed 7/25/18 at: http://www.pionline.com/article/20110502/ONLINE/110509998/deemed-iras-po...

3J. Towarnicky, Betamax, Edsel, New Coke and … now MyRA Joins An Elite Class of Marketing Failures, 07/31/17, Accessed 7/25/18 at: https://www.psca.org/blog_jack_2017_2 The “sidecar” account has a maximum of $10,000, the MyRA, $15,000. The “sidecar” account would be a savings account, MyRA offered a single, government-backed capital preservation investment.

4U.S. Government Accountability Office (GAO), Policy Changes Could Reduce the Long-term Effects of Leakage onWorkers’ Retirement Savings, GAO 09-715, August 2009. “There are many reasons why participants may choose to use their retirement savings prior to retirement, and some of these choices may involve a rational trade-off between immediate financial emergencies and future retirement needs. … Participants facing sudden and unanticipated hardships would also benefit from the assurance that they are using the most appropriate and least damaging option, thereby minimizing the negative impacts on their overall retirement preparedness.

5For example, to avoid unnecessary leakage, employers should not approve participants for hardship withdrawals until they are certain that participants have exhausted the plans’ loan provisions. … Ensuring that participants choose the path that causes the least harm to their retirement accounts and continue to make retirement contributions whenever possible may help mitigate the adverse impacts of leakage that otherwise will linger into retirement.” Accessed 7/25/18 at: https://www.gao.gov/assets/300/294520.pdf For example, see: J. Divine, Retirement Is a Bigger Crisis Than Health Care, U.S. News/Money, 5/24/17 Accessed 7/25/18 at: https://money.usnews.com/investing/articles/2017-05-24/retirement-saving... See also: A. Semuels, This Is What Life Without Retirement Savings Looks Like, Atlantic, 2/22/18, Accessed 7/25/18 at: https://www.theatlantic.com/business/archive/2018/02/pensions-safety-net... See also: T. Ghilarducci, T. James, There is a retirement crisis. And workers can’t fix it alone, Marketwatch, 1/26/18, Accessed 7/25/18 at: https://www.marketwatch.com/story/there-is-a-retirement-crisis-and-worke...

6A. Biggs, S. Schieber, Is There a Retirement Crisis?, National Affairs, Summer 2014, Accessed 7/25/18 at: https://www.nationalaffairs.com/publications/detail/is-there-a-retiremen... See also: A. Biggs, Is There a Retirement Crisis? Examining Retirement Planning in the Household and Government Sectors, Mercatus Research Paper, 10/3/17. “In response to a widespread perception that households are undersaving for retirement, policymakers have proposed expanding Social Security and establishing supplementary retirement saving plans run by state governments. … It appears that, on average, households are doing at least as well in saving for retirement as governments are in funding retirement plans on households’ behalf.” Accessed 7/25/18 at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3046833 , See also: J. Towarnicky, Retirement in America – A Life Of Poverty? 06/29/18, Accessed 7/25/18 at: https://www.psca.org/blog_jack_2018_32 Retirement in America - Individual Account Retirement Savings Plans ARE Good Enough! 07/05/18, Accessed 7/25/18 at: https://www.psca.org/blog_jack_2018_33 Can ≠ Will: Yesterday’s 401(k) ≠ Tomorrow’s 401(k), 07/09/18, Accessed 7/25/18 at: https://www.psca.org/blog_jack_2018_34

7U.S. Government Accountability Office (GAO), Note 3, Supra

8J. Towarnicky, Hardship Withdrawals – An Attractive Nuisance Becomes More Attractive, 02/09/18. “…President Trump has signed the Bipartisan Budget Act of 2018 into law (which) … includes provisions that make hardship withdrawals more attractive – removing barriers, increasing available monies, and removing the suspension of contributions.” Accessed 7/25/18 at: https://www.psca.org/blog_jack_2018_5 Note that three of the senator cosponsors for S.3218 voted in favor of the Bipartisan Budget Act of 2018.

9R. Steyer, Note 2, Supra

10PSCA, 60th Annual Survey, 2018. 14.6% of surveyed plans allow for after tax 401(a) contributions.

11A “typical” 401(k) has a 50% match on the 1st 6% of pay. This example assumes the $1,000 is part of the first 6% of pay contributed. This example assumes that the match is 100% vested 1st day and that the plan permits individuals to borrow 100% of the first $10,000 in the account. The PSCA 60th Annual Survey shows that 41% of plans had immediate, 100% vesting.

12 Vanguard, How America Saves, 2018. “In 2017, … the average employee-elective deferral required to maximize the match was 7.0% of pay; the median value, 6.0%. … participants saved 6.8% of their income on average … The median participant deferral rate was 6.0% …” Accessed 7/25/18 at: https://pressroom.vanguard.com/nonindexed/HAS18_062018.pdf

13J. Towarnicky, Qualified Plan Loans, Evil or Essential. Benefits Quarterly, 2nd Quarter 2017. Accessed 7/25/18 at: https://www.ifebp.org/inforequest/ifebp/0200570.pdf