Advertisement

True-up, Catch-up, What's up?

“The wonderful thing about second chances is that they exist.”1

True Up – Internal Revenue Code (IRC) §§401(k) and 403(b) plans, and Health Savings Accounts (HSA)

Many Individual account savings plans and some HSAs offer an employer match. Some calculate the match each payday. Some calculate the match on a cumulative, year-to-date basis. Some “true-up” the match after the end of the plan year so workers receive the same employer contribution amount regardless of when contributions are made during the year. The “true-up” is a “second chance” for workers who:

- Failed to enroll earlier in the year, or

- Failed to contribute enough each paycheck to obtain the full employer financial support.

Given the diversity of worker finances where many, if not a majority, live paycheck to paycheck, plan sponsors should consider the need for a “true-up” provision – in your 401(k), 403(b), and/or in your HSA.

|

|

It's time to take immediate action if: - Your plan has a “true-up” provision and allows flexibility in contribution rates. Issue a specific, targeted communication to encourage workers to increase contributions as needed to obtain the full employer match. |

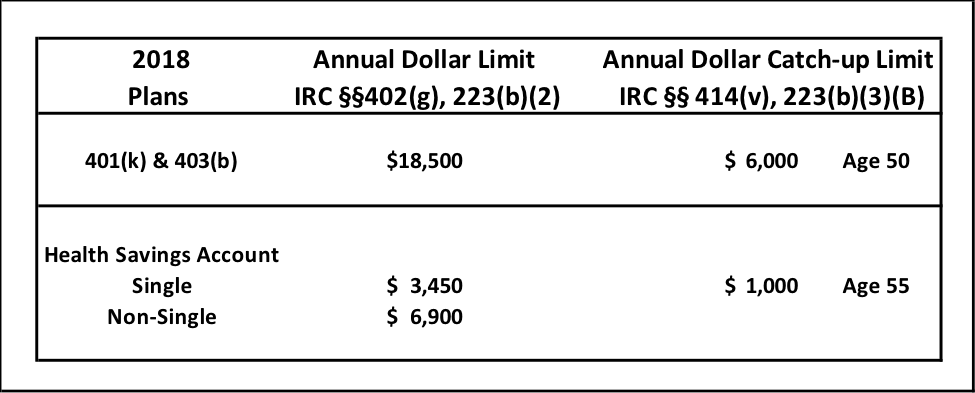

Catch-Up – IRC §§401(k) and 403(b) plans, and HSAs

Catch-up contributions for workers aged 50 and up were added for 401(k) and 403(b) plans as part of the Economic Growth and Tax Relief Reconciliation Act of 2001. Most plans provide catch-up provisions – you should too! Participants become eligible to make catch-up contributions in the calendar year in which she/he reaches age 50. Catch-up contributions are special for three reasons – they are not included or considered when applying:

- The annual addition calculation under IRC §415(c),

- The maximum deferral limit under IRC §402(g), and

- The Average Deferral Percentage (ADP) discrimination testing.

So, catch-up contributions can be used to enable higher total contributions and, as necessary, to re-characterize contributions that would otherwise be returned to participants due to IRS limits.2

Catch-up contributions were part of the initial authorization for HSAs as part of the Medicare Modernization Act of 2003. Because the HSA account is a participant-owned custodial account, all individuals who are eligible to contribute to a HSA become eligible to make catch-up contributions in the calendar year in which she/he reaches age 55. IRC §223(b)(3)(B) provided for an initial catch-up contribution amount of $500 in 2004, and increased that by $100 each year until it reached the current maximum of $1,000 in 2009 - it has not changed since then. Each eligible individual who is age 55 or older can make a catch-up contribution to his or her own HSA.

What’s Up?

Are you adding a HSA-capable health option in 2019? If so, you may want to consider making that option available December 1st 2018, so that you can publicize and market a unique option to contribute a full year’s amount to the HSA this year, under the “last month rule.”3 For some, that could be the most valuable “catch-up” or “true-up” option for 2018!

1Felice Stevens, The Shape of You

2Internal Revenue Service, See: https://www.irs.gov/retirement-plans/401k-plan-catch-up-contribution-eli... See also: Treasury Regulation §1.414(v)-1(d)(2)(iii)

3IRC §223(b)(8) “… for purposes of computing the (contribution limit) … an individual who is an eligible individual during the last month of such taxable year shall be treated — as having been an eligible individual during each of the months in such taxable year, and as having been enrolled, … in the same high deductible health plan in which the individual was enrolled for the last month of such taxable year” (so long as coverage is maintained throughout a testing period of the subsequent taxable year).