Advertisement

Impediments to Saving for Retirement - The Barriers, Part 1

Today’s typical histrionic, hyperbolic headline: “Retirement Crisis: Workers Can’t Afford to Save For Retirement Due to Crippling Out of Pocket Medical Expenses and Crushing Student Debt!”1 The accurate rewrite: “Saving For Retirement is Doable – Almost All Workers Have Low, Budget-able Out-of-Pocket Medical Expenses, and Student Debts.”2

My discussions with other plan sponsors are often focused on increasing retirement savings plan participation and contributions. A frequent topic is the perception that many workers are financially incapable of saving for retirement.

Certainly, studies show most Americans live paycheck to paycheck. However, payday-to-payday living is not a barrier to saving.3 Others cite out-of-pocket medical costs or student debt. Recent studies show those aren’t a barrier, either. Consider:

- The median annual out-of-pocket medical expense was $2644, a very small portion of medical spending5, and

- A minority of households have student debt. More importantly, the median monthly student loan payment was $203.6

Total National Health Expenditures – 1970 vs. 2016

Out of pocket spending has declined from 34% of all medical expenditures to only 10%

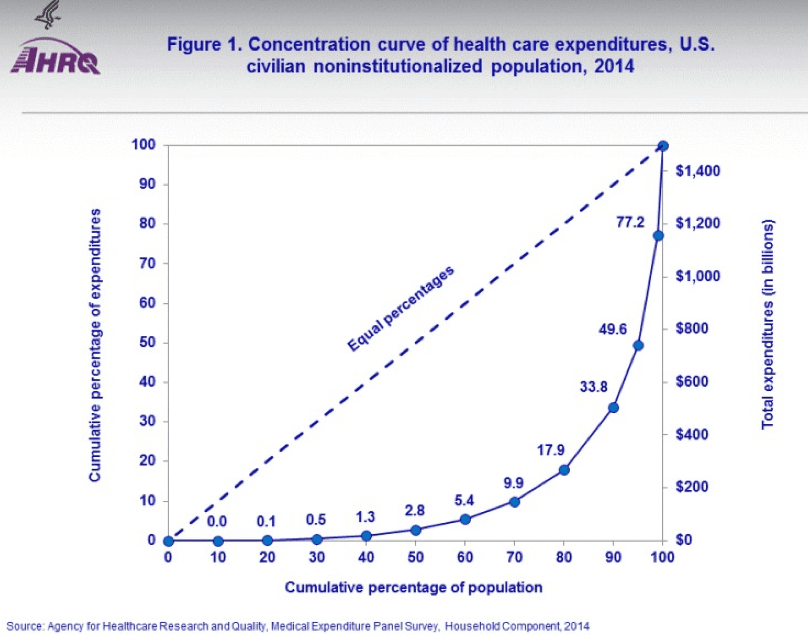

So, most workers have minimal out-of-pocket medical costs. Fifty percent of Americans account for less than 5 percent of all medical spending. In other words, medical spending is concentrated among approximately 5 percent of Americans who account for more than half of all medical spending. Most are retired or disabled.7 And, more than 95 percent of all workers have either no student debt or student debt that is manageable and budget-able.

The bottom line is that those financial challenges are not a barrier. And, plan sponsors don’t have to wait for new legislation or more regulation (examples being sidecar accounts for emergencies8, more guidance on “matching” employer contributions for student loan debt payments or a retirement savings mandate).

Part 2 of this series will reconfirm an effective solution- regardless of the nature or size of workers’ financial challenges.

1T. Ghilarducci, T. James, There is a retirement crisis. And workers can’t fix it alone, Marketwatch, 1/26/18, Accessed 10/22/18 at: https://www.marketwatch.com/story/there-is-a-retirement-crisis-and-worke... ; See also: Politico, How to solve the retirement crisis, A POLITICO Working Group Report. 06/07/18, Accessed 10/22/18 at: https://www.politico.com/agenda/story/2018/06/07/future-of-prosperity-re... ; See also: C. Farrell, Calling For A Blue-Ribbon Panel On The Retirement Crisis, Forbes, 5/20/18, Accessed 10/22/18: https://www.forbes.com/sites/nextavenue/2018/05/20/calling-for-a-blue-ri... See also: S. Harris, America's Retirement Savings Crisis, 1/10/18, Accessed 10/22/18 at: https://www.jackson.com/financialfreedomstudio/articles/2018/01/americas... A. Tergesen, Bankruptcy Filings Surge Among Older Americans; Authors of recent study cite reductions to social safety net, shift from pensions to 401(k)s, 8/7/18, Accessed 10/22/18 at: https://www.wsj.com/articles/bankruptcy-filings-surge-among-older-americ... See also: D. Thorne, P. Foohey, R. Lawless, K. Porter, Graying of U.S. Bankruptcy: Fallout from Life in a Risk Society, 8/18/18, Accessed 10/22/18 at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3226574 See also: P. Fronstin, L. Greenwald, Workers Rank Health Care as the Most Critical Issue in the United States, Employee Benefits Research Institute and Greenwald & Associates, 9/24/18. “… Of the one-half of workers reporting cost increases, 24% state they have decreased their contributions to retirement plans … 30% delayed retirement, … 17% have taken a loan or withdrawal from a retirement plan …” Accessed 10/20/18 at: https://www.ebri.org/pdf/EBRI_IB_459_WBS.24Sept181.pdf See also: R. Moore, Health Care Costs Affecting Retirement Savings and Financial Wellness, 10/15/18, Accessed 10/22/18 at: https://www.plansponsor.com/health-care-costs-affecting-retirement-savin... See also: Annie Nova, More people are unprepared for retirement because of student loans, 5/23/18, Accessed 10/20/18 at: https://www.cnbc.com/2018/05/23/how-your-student-loans-can-hurt-you-late... \

2Andrew Biggs, The Media's Coverage of Retirement Saving Really is Terrible, Forbes 7/2/18, Accessed 10/22/18 https://www.forbes.com/sites/andrewbiggs/2018/07/02/the-medias-coverage-..., J. Towarnicky, Retirement in America - A Life of Poverty? 6/29/18, Accessed 10/22/18 at: https://www.psca.org/blog_jack_2018_32 See also: J. Towarnicky, Retirement in America - Individual Account Retirement Savings Plans ARE Good Enough! 7/5/18, Accessed 10/22/18 at: https://www.psca.org/blog_jack_2018_33 ; J. Towarnicky, The Sky is Not Falling On Older Americans, 8/27/18, Accessed 10/22/18 at: https://www.psca.org/blog_jack_2018_40

3American Payroll Association, Employees in America Living Paycheck to Paycheck Even After Tax Reform, Getting Paid in America, September 2018. More than 70% of workers live paycheck-to-paycheck (they would have some or significant difficulty if a paycheck was delayed one week). However, among those same workers, nearly 90% of those who are eligible for an employer-sponsored savings plan also contribute to retirement savings. Accessed 9/28/18 at: https://www.prnewswire.com/news-releases/employees-in-america-living-pay...

4E. Mitchell, Concentration of Health Expenditures in the U.S. Civilian Noninstitutionalized Population, 2014, November 2016, Accessed 10/20/18 at: https://www.ncbi.nlm.nih.gov/books/NBK425792/

5Kaiser Family Foundation, Out of Pocket Spending Represents a Smaller Portion of Total Expenditures (in 2016) Than It Did in 1970, Accessed 10/21/18 at: https://www.healthsystemtracker.org/chart-collection/u-s-spending-health...

6Cleveland Federal Reserve Bank, Is There A Student Loan Crisis, Not in Payments, 5/16/16, Accessed 10/20/18 at: https://www.clevelandfed.org/newsroom-and-events/publications/forefront/...

7B. Alemayehu, K. Warner, The Lifetime Distribution of Health Care Costs, 2000. “… Nearly one-third of lifetime expenditures is incurred during middle age, and nearly half during the senior years. … The distribution of health care costs is strongly age dependent … After the first year of life, health care costs are lowest for children, rise slowly throughout adult life, and increase exponentially after age 50 … annual costs for the elderly are approximately four to five times those of people in their early teens. Accessed 10/21/18 at: https://www.ncbi.nlm.nih.gov/pmc/articles/PMC1361028/ See also: J. Jones, M. DeNardi, E. French, R. McGee, J, Kirschner, The Lifetime Medical Spending of Retirees, May 2018. “… households who turned 70 in 1992 will on average incur $122,000 in medical spending, including Medicaid payments, over their remaining lives. …” Accessed 10/21/18 at: https://www.nber.org/papers/w24599 See also: CMS, National Health Expenditures 2016 Highlights. “Out-of-Pocket expenses were 11% of total health spending.” Accessed 10/21/18 at: https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Tren... See also: P. G. Peterson Foundation, Spending on Elderly and Disabled Medicaid Beneficiaries is High. Of the $402B in Medicaid spending, 42% was spent on ~11MM Medicaid beneficiaries, ~$15,000 a year. Accessed 10/22/18 at: https://www.pgpf.org/chart-archive/0094_spending_medicaid_beneficiaries See also: J. Cubanski, T, Neuman, A. Damico, Medicare's Role for People Under Age 65 with Disabilities, Kaiser Family Foundation, 8/12/16, “… Medicare covers 9.1 million people with disabilities who are under age 65… (average annual spending was) ~$13,000. Accessed 10/22/18 at: https://www.kff.org/medicare/issue-brief/medicares-role-for-people-under...

8J. Towarnicky, Sidecar = Suboptimal, 7/28/18, Accessed 10/22/18 at: https://www.psca.org/blog_jack_2018_36