Advertisement

Annuitization Anyone?

Looking For a Few “Good” Plan Sponsors, Part 2

My search continues for plan sponsors willing to innovate and help participants who need more retirement income without burdening other participants and the plan with the compliance burdens of an annuity.1

Is There A Need For More Retirement Income?

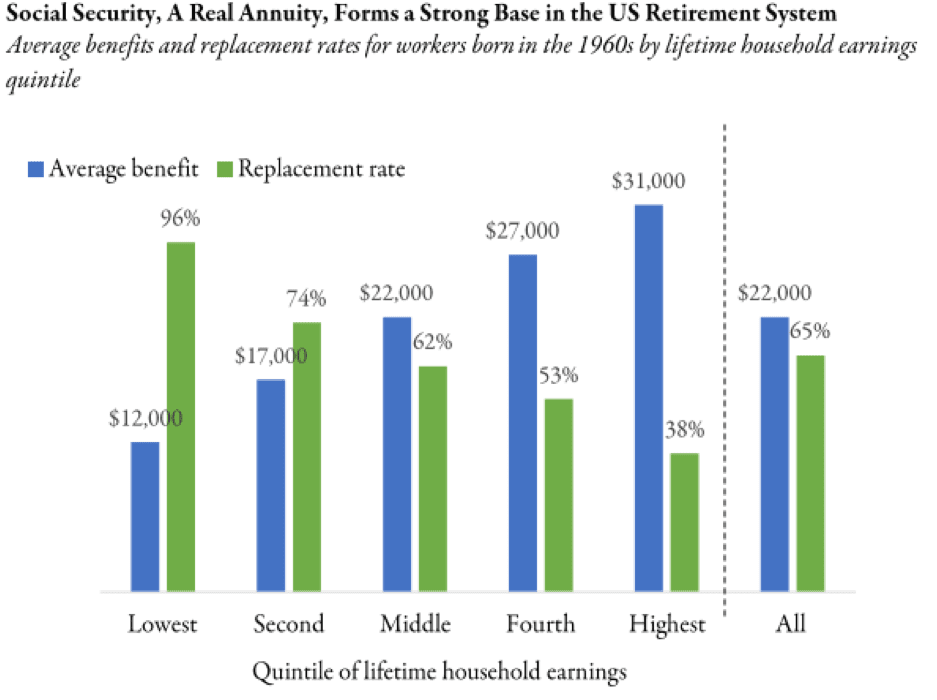

Yes, for some households. However, other households are highly annuitized. Consider Social Security replacement rates:2

Social Security is paid as a monthly lifetime annuity. It is the primary means of support for retirees with low lifetime earnings, including workers who have periods without wages. And, Social Security is a substantial source of income for all retirees. On average (and averages can be deceiving,) for all households comprised of workers born in the 1960s (those expected to retire in the next 10-25 years,) Social Security benefits are scheduled to replace 65 percent of inflation-indexed lifetime earnings.

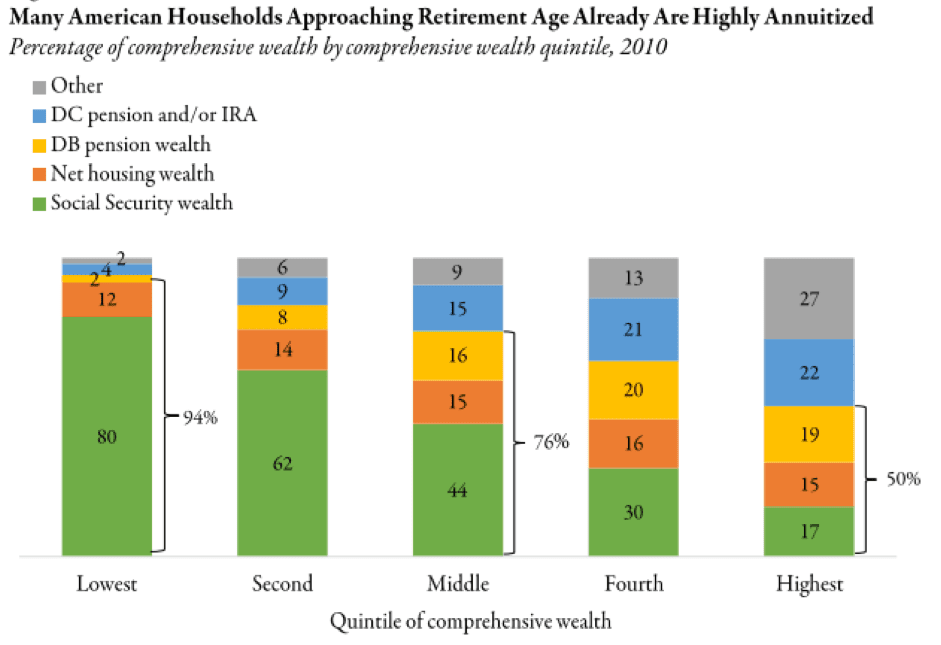

A majority of older Americans already hold most of their wealth in an annuity-equivalent form, including both future Social Security and defined-benefit (DB) plan benefits and owner-occupied housing.3

So, most near-retiree U.S. households already are highly annuitized. So, rationally, most households may not want to annuitize more assets, preferring instead to preserve the liquidity and flexibility of their defined-contribution (DC) plan balances.

Meeting the Diverse Needs of Your Participants

During my 30-plus years in plan sponsor roles throughout five different decades, I encountered very few who expressed an interest in using plan assets to purchase an annuity as they transitioned into retirement. Unsurprisingly, most plan sponsors have not added an in-plan annuity option or selected a vendor for annuity purchases. Other plan sponsors, like me, took action to remove the in-plan annuity option back in the early 1980s so as to reduce compliance burdens on participants and the plan.4 That is, those interested in an annuity purchase are directed to the individual market.

Because demand remains weak, most plan sponsors continue to avoid annuities.5 Only a minority invest in worker education regarding retirement income. As a result, participants who want to use plan assets to purchase added income in retirement may be underserved.

How have plan sponsors dealt with underserved populations in the past? Well, throughout the past 10-plus years, we added automatic features to “nudge” those who had not voluntarily enrolled or those who had never increased their contribution rate. We added qualified default investment alternatives (QDIAs) for those who are uninterested in investment decision making.

Perhaps it is time, or even past time, for plan sponsors to adopt plan provisions that serve as a payout “nudge.” There are payout mandates in defined benefit and defined contribution pension plans – a single life annuity and, where married, a 50 percent joint and survivor annuity. Most times, in a majority of those plans, retirees still control the benefit commencement date.

So, in an individual account retirement savings plan, the default payout “nudge” might be an annual installment designed to “bridge” and ultimately dovetail with deferring commencement of Social Security until age 70. Some plan sponsors have adopted a default payout option in the form of annual installments to comply with minimum distribution requirements, starting at the required beginning date. However, I am not aware of any plan sponsor that has adopted this form of a “nudge” as a means of encouraging participants consider deferring Social Security commencement so as to minimize the cost to purchase added retirement income.

With this type of a default payout “nudge,” participants retain 100 percent control. They still have to elect to commence payment (unless they have already deferred commencement past age 70). And, because the payout strategy does not involve an annuity purchase, workers retain the option to change their minds at any time – before or after annual installment payments commence.

Finally, this strategy may minimize the cost to participants who want to purchase additional retirement income while, at the same time, it will preserve two of the individual account retirement savings plan’s most valuable “assets” - liquidity and flexibility.

I am still looking for a few “good” plan sponsors. Send me a note at [email protected].

1J. Towarnicky, Looking For A Few “Good” Plan Sponsors, 11/28/17, Accessed 12/31/18 at: https://www.psca.org/blog_jack_2017_16 S.

2Holden, S. Salinas, 2018 ERISA Advisory Council, Lifetime Income Solutions as a Qualified Default Investment Alternative (QDIA), 8/20/18. “… Estimates show that, for those in the lowest quintile of workers ranked by lifetime household earnings, first-year Social Security benefits are scheduled to replace 96% of inflation-indexed lifetime earnings, on average, for workers born in the 1960’s who claim benefits at age 67 (Social Security Normal Retirement Age).” Accessed 12/31/18 at: https://www.dol.gov/sites/default/files/ebsa/about-ebsa/about-us/erisa-a...

3Ibid, note ii. Data represent households with at least one member aged 57 to 62 and exclude the highest and lowest 1% of households ranked by comprehensive wealth. Comprehensive wealth includes the present value of future Social Security benefits and the present value of future DB benefits, in addition to financial assets, net housing wealth and other balance sheet items.

4Retirement Equity Act of 1984, Pub. L. 98-397, 8/23/84.

5J. Towarnicky, 2018 ERISA Advisory Council, Lifetime Income Solutions as a qualified Default Investment Alternative (QDIA), Focus on Decumulation and Rollovers, 6/19/18, Accessed 12/31/18 at: https://www.dol.gov/sites/default/files/ebsa/about-ebsa/about-us/erisa-a...