Advertisement

Rothification Redux?

Failure to Reform Federal Spending = An Endless Loop Which Puts Benefits Tax Preferences At Risk

Think we are done with attempts to curtail benefits tax preferences? Think again. Last week, President Trump released his $4.4 Trillion proposed budget for the 2019 federal fiscal year (October 1, 2019 – September 30, 2020). That spending level is projected to add $984 Billion to the federal deficit and national debt in one year. Projections are for a $7+ Trillion addition to our national debt over the next ten years! Those deficits occur despite:

- Projected annual economic growth of 3.1% over the next three years, and

- $1.8 Trillion of cuts to scheduled spending on federal entitlements.

For comparison, President Bush II presided over an increase in our federal debt of $4.9 Trillion, from $5.7 Trillion to $10.6 Trillion (January 20, 2001 – January 19, 2009). Despite voting for those budgets, then-Senator Obama claimed the Bush II deficits and debt additions reflected “irresponsible” and “unpatriotic” behavior. Later, President Obama himself presided over nearly twice as much of an increase in federal debt – a $9.3 Trillion increase, from $10.6 Trillion to $19.9 Trillion (January 20, 2009 – January 19, 2017).

So, given these profligate spending levels, it is only a matter of time before the budget “loop” completes a full cycle – and Congress will again seek new tax revenues (link: ) And, because the Tax Cuts & Jobs Act of 2017 reduced a number of tax preferences, our benefits tax preferences are now a much more prominent and likely target!

Those who want to eliminate or curtail pre-tax contributions (Rothification) may repeat prior arguments, such as:

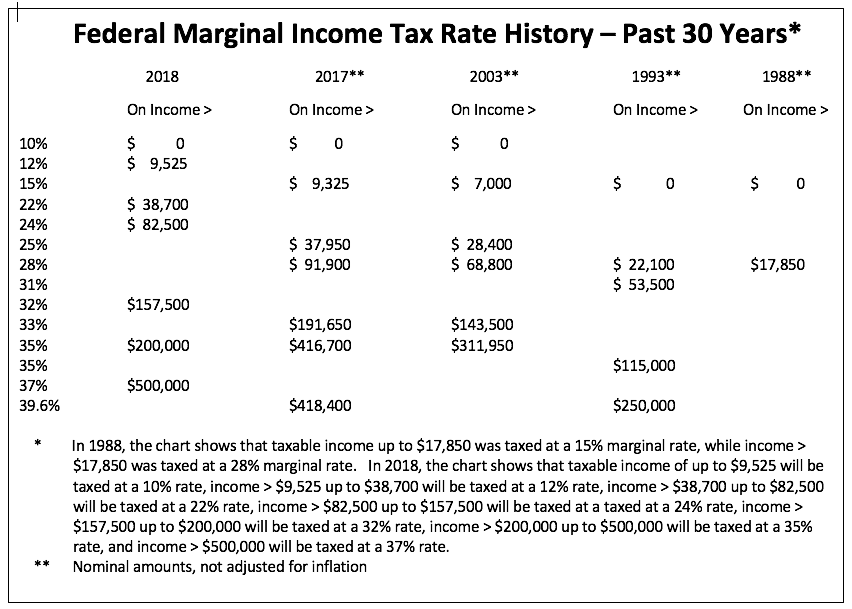

- First, Roth is better because taxes are lower. After the Tax Cuts & Jobs Act of 2017, our rates are as low as any of the past 30 years. Given projected debt burdens, these may be the lowest we’ll see in the near future.

- Second, Roth is better for retirement preparation. Workers who choose Roth often save the same percentage of pay - effectively saving more for retirement.

There are too many variables to assert Roth is better than pre-tax, or vice versa. Consider:

- Pre-tax savings avoid taxes at the top marginal rate; but payouts are often taxed at the effective (average) rate,

- Taxes may differ between the state where employed compared to the state where benefit payouts are received,

- While the cited study showed workers who choose Roth over pre-tax do not reduce their overall savings rate, the average Roth contribution was a range of only .1% to 1.6% of pay,

- The cited study used a survey to try to reveal workers’ intuition about optimal choices. But, the study itself confirms that “… individuals, on average, do not respond rationally to the relative economic incentives…” That’s no surprise to plan sponsors who increasingly deploy automatic features, Qualified Default Investment Alternatives, etc.

Our 61st annual survey shows 63 percent of plans offer Roth. If you don’t offer Roth, perhaps it is time to reconsider. Roth isn’t for everyone. But, in the 12 years since Roth became available, it has demonstrated its value for many workers:

- Just starting their careers (likely with earnings at their lowest marginal rate),

- Employed in a state without an income tax,

- Looking for tax diversification, flexibility, and as a hedge against higher tax rates,

- Who are building a legacy and want to avoid minimum required distributions,

- Whose contributions are limited by the 402(g) and/or 414(v) maximums,

- Who are highly paid and eligible to contribute to a deferred compensation plan, and those

- Who would like to consider a Roth conversion but are ineligible to take a distribution at this time.

Finally, offering Roth may make it easier to explain why Rothification is ill-advised. Once a plan offers Roth, we know just how many workers will reject Roth in favor of pre-tax contributions or choose a combination of Roth and pre-tax. And, of course, the increased revenue from Rothification will be less and, importantly, will only come from workers who previously rejected Roth!