Advertisement

Were You Generous or Are Company Contributions Part of Your Total Rewards Strategy?

From PSCA’s 61st Annual Survey: Company contributions are at a new high following the Great Recession – 5.1 percent.

PSCA 61st Annual Survey results show that company contributions as a percentage of payroll have more than fully recovered after declines experienced during and following the Great Recession.

Many employers adjusted or suspended their employer contribution during the Great Recession.1 The 61st Annual Survey shows those curtailments have been more than fully reversed. Next year’s survey, reflecting 2018 data, should show further improvements due to changes prompted by tax reform late in 2017.2

That said, the role for employer financial support in profit sharing plans (including the 401(k)) is not always clear. Prior to the Tax Reform Act of 1986, employer contributions to profit sharing plans were only permitted out of corporate profits.3 Today, the employer contributions reflect a variety of objectives, including:

- Sharing of profits,

- Funding retirement,

- A component of a holistic personal and financial wellness strategy, and/or

- Part of total rewards.

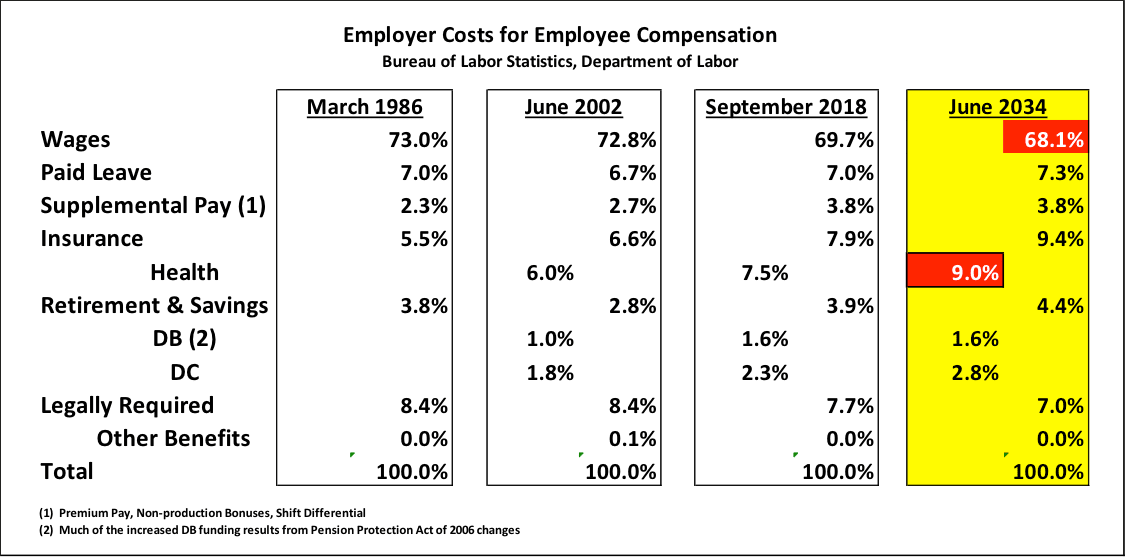

Allocation of rewards spend continues to evolve - reflecting an ever-increasing shift toward greater spending on active worker health coverage.4

Many human resources professionals expect that trend to continue, with even greater allocations to health coverage in the future.

For comparison, some surveys and whitepapers highlight the “retirement savings crisis” – suggesting employers will voluntarily or be compelled to adopt retirement readiness outcome philosophies, reflecting ever-increasing employer financial support for retirement benefits.5

To me, that sounds like wishful thinking among retirement industry service providers, academics and policymakers, because median tenure among workers ages 25 – 64 has been and continues to be about 5 years of service. Instead, a more likely trend will see plan sponsors/employers adding new options and greater worker control over the allocation of financial support among available rewards choices. One study suggests: “Adopting a defined contribution approach to healthcare benefits allows employers to dedicate more dollars to retirement benefits, keep the workforce fit and the business competitive.”6

However, when it comes to health trends, the only certainty seems to be something Herb Stein, Nobel Prize winning economist once said: “If something cannot go on forever, it will stop.”7

1A. Munnell, L. Quinby, Why Did Some Employers Suspend Their 401(k) Match, February 2010, Accessed 1/1/19 at: http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.466.6638&rep=re... See also: Pension Rights Center, Companies that have changed or temporarily suspended their 401(k) matching contributions. A list of 404 plans that took action mostly in 2008 – 2010 where 73 have reinstated/restarted the match. Accessed 1/1/19 at: http://www.pensionrights.org/publications/fact-sheet/companies-have-chan...

2The Tax Cuts and Jobs Act of 2017, Pub. L. 115-97, 12/22/17. See also: Americans For Tax Reform, List of Tax Reform Good News, Updated 10/31/18. “… 750 examples of pay raises, bonuses, 401(k) match increases, expansions, benefit increases, and utility rate reductions (after passage of the Tax Cuts and Jobs Act of 2017) …” Accessed 1/1/19 at: https://www.atr.org/list

3IRC§401(a)(27), Added by The Tax Reform Act of 1986, Pub. L. 99-514.

4Bureau of Labor Statistics, Department of Labor, Employer Costs for Employee Compensation, September 2018, Accessed 1/1/19 at: https://www.bls.gov/news.release/pdf/ecec.pdf

5Transamerica, Prescience, 2017, Accessed 1/1/19 at: https://www.ta-retirement.com/resources/Prescience2017_Summary_FINAL_329...

6Transamerica, Prescience 2019, Expert Opinions on the Future of Retirement Plans, Accessed 1/1/19 at: https://www.transamerica.com/images/19231-ps_b_prescience2019_lorezviewo...

7H. Stein, A Symposium on the 40th Anniversary of the Joint Economic Committee, Hearings Before the Joint Economic Committee, Congress of the United States, Ninety-Ninth Congress, First Session, January 16 and 17, 1986, Panel Discussion: The Macroeconomics of Growth, Full Employment, and Price Stability, Accessed 1/1/19 at: https://babel.hathitrust.org/cgi/pt?id=umn.319510030778307;view=1up;seq=...