Advertisement

Opportunity Is Knockin’ on the Door! Let ’Em In!

Maximizing use and value of Health Savings Accounts.

Despite the growth in Health Savings Account (HSA) usage1, most employees still miss out on America’s most valuable, tax-favored benefit. As of 2019, fewer than 11 percent of American adults have an HSA, with an average account value of less than $300. We offer some “best practice” guidance on maximizing the utility and value only possible through an HSA.

No Benefit Without Access

Why do health plan sponsors fail to offer HSA-eligible coverage? (See Sidebar: Our Coverage Challenge.) Lack of access places employers and their employees at a competitive disadvantage — foregoing the HSA’s utility and tax preferences.

The HSA is a unique, flexible tool — the Swiss Army Knife© or Leatherman© of employee benefits. For the plan sponsor, the HSA can be a payroll tax reduction opportunity, an anti-selection sentinel, an executive benefit, and/or a “pay for performance” or “pay for results” value added component within a total rewards strategy. For employees, the HSA can fund out-of-pocket medical, dental, vision, and Long-Term Care (LTC) expenses, today and tomorrow, as well as future insurance premiums — Medicare, COBRA, LTC, and premiums for coverage while receiving unemployment compensation. Employees can also use HSA assets to replace income in retirement, as a survivor benefit, as an income tax averaging scheme, and/or as an emergency account.

Others may not fully appreciate the tax preferences. For example, for employees who set aside the same amount of take-home pay, HSA dollars go 60 percent further than the 401(k) when it comes to funding Medicare premiums.

Where plan sponsors fail to offer an HSA-eligible option, it means your rewards package is sub-optimal — incorporating fewer tax-preferred benefits and savings options. Employees miss out on America’s most tax-favored benefit.

Simply, an HSA may offer the coverage that best meets the diverse needs of your workforce, today and tomorrow.

Solution: Offer a (new) HSA-eligible coverage option effective December 1, 2020 so employees can make a maximum HSA contribution for both 2020 and 2021.

Eligible Employees Won’t Benefit Unless They Enroll

Where an HSA-eligible coverage option is offered, 79 percent offer it as a choice alongside PPO or HMO options, according to PSCA’s 2020 HSA Survey. The survey also showed that only 51 percent of employees whose employer offered HSA-eligible coverage enrolled in that option.8 (See Sidebar: Our Marketing/ Education Challenge)

Consciously or unconsciously, enrollment processes and communications tend to favor existing coverage options. Decades of annual enrollment experience confirms:

- Healthy employees are sensitive to contribution differences (point- of-enrollment cost sharing),

- Employees with health conditions are sensitive to differences in copayments and deductibles (point-of-purchase cost sharing), resulting in

- Positive risk selection when employees are given a choice of plans and disenrollment in HSA-eligible coverage.

Some prominent reasons why HSA enrollment has lagged:

- Myopia: Many annual enrollment processes focus solely on coverage needs for the next 12 months.

- Prioritization: Most Americans live paycheck-to-paycheck; many need a “nudge” to save.

- Inertia and/or status quo bias: Many prefer things remain relatively unchanged.

- Availability bias: People over-insure. They overestimate the likelihood of events with greater “availability” — they are influenced by size, recency, or how the event was emotionally charged.

- Knowledge Inertia: We often don’t learn from others’ or our own mistakes — suffering from stagnant, outdated information and/or experience, a lack of exposure to new thinking, or an unwillingness to invest time/resources in decision-making.

- Continuation bias and present bias: Some fail to recognize how the challenge has evolved or that the initial enrollment decision was incorrect.

- Position bias: Too frequently, the HSA-eligible coverage is positioned as the last option, the low coverage option, or as substandard coverage. Studies show that the presentation order and methods affect decision- making.

Solutions that might level the playing field where HSA-eligible coverage is offered as a choice:

- Avoid focusing on deductibles in comparisons — present a complete picture, including employer HSA contributions.

- Carefully name the HSA-eligible option — avoid “high deductible” or the deductible amounts (e.g., $1,400 option).

- Use the same minimum general deductible structure for all options.

- Implement a full positive re-enroll-ment and set the HSA-eligible option as the default.

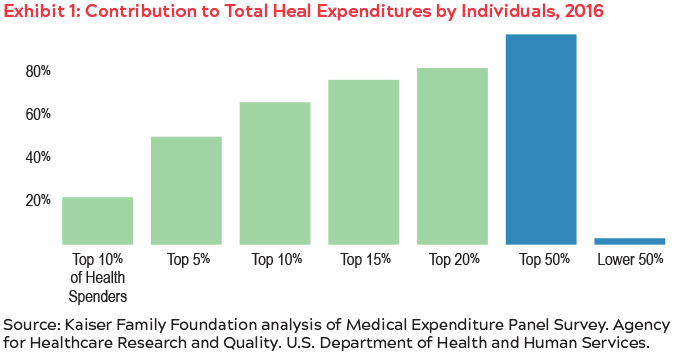

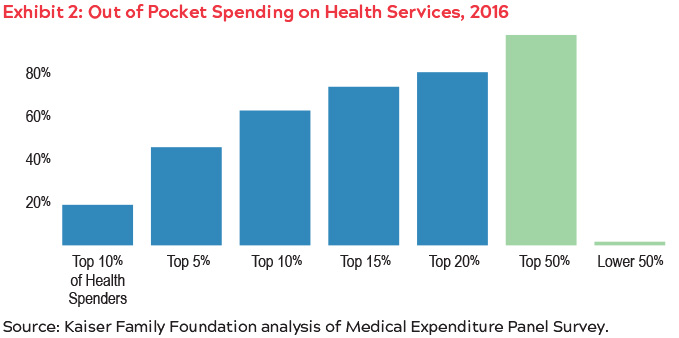

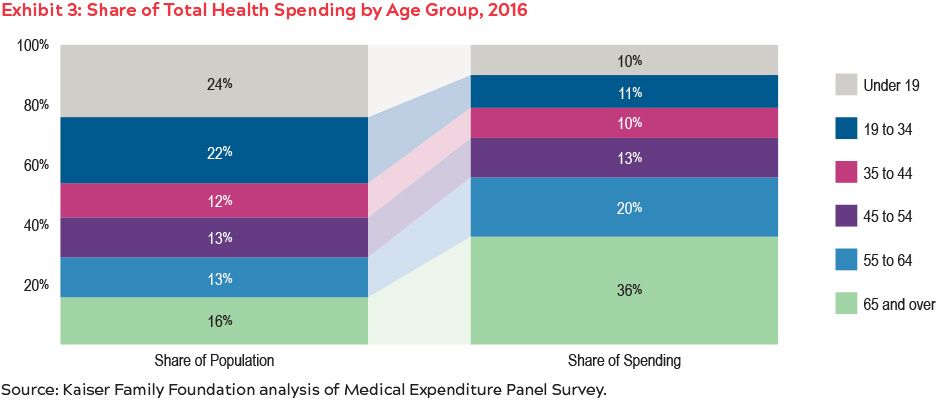

- Reduce over-insurance by creating an “informed annual enrollment process” — highlight the employee’s own medical spend or use data that confirm most Americans won’t meet their deductible most years (See Exhibits 1–3.)

If each coverage choice has the same level of employer financial support, HSA-eligible coverage is often the best choice, but undersubscribed. Employees end up in the wrong option.

Enrollees May Still Miss Out

Many who enroll in HSA-eligible coverage fail to open an HSA. Some haven’t contributed to their HSA. Others haven’t accumulated enough assets to allow for investment.11 (See Sidebar: Our Participation Challenge)

Too many focus the HSA marketing and education as a “Super-FSA.” HSA education remains a roadblock to enrollment in, contributions to, and investment in HSAs according to a white paper from The American Retirement Association.12 Only a handful of HSA owners have consistently optimized America’s most valuable benefits tax preference.13

Solutions include:

- “Start the clock” for eligible expenses — deposit $1 into the HSA upon initial enrollment in HSA-eligible coverage.

- For those who enroll in HSA-eligible coverage, incorporate an automatic contribution default.

- Market the HSA as an emergency account — especially for unexpected medical, dental, vision, hearing, and long term care out of pocket expenses.

- Educate employees about the benefits of the HSA at retirement by highlighting anticipated retiree medical costs.

- For those enrolled in HSA-capable coverage, consider a mid-year “re-enrollment.”

- Open the HSA with a $1 contribution,

- Add a default, automatic contribution, or

- Escalate the HSA contribution amount.

Some plan sponsors have started to adjust their offerings to remove impediments, allow for apples-to-apples comparisons, deploy defaults like automatic enrollment and escalation, and deploy communication strategies that highlight the opportunity that an HSA provides.

Someone’s knocking on the door. Somebody’s ringing the bell. Do them a favor, open the door, let ‘em in… to the HSA.

Jack Towarnicky is Principal Researcher for the American Retirement Association.

Please note that the author will provide endnotes upon request. For a complete list of the endnotes, send Jack an email at [email protected]