Advertisement

But I Repeat Myself - You Should Offer a Health Savings Account-Capable Health Option*

An Employee Benefits Version of Groundhog Day1

A week or so ago, in a presentation titled, Health AND Wealth in Retirement, I once again stood in front of a crowd of plan sponsors extolling the value of HSAs. HSAs offer:

- The most valuable benefits tax preference,

- Immediate and future value,

- An opportunity to accumulate wealthand much more!

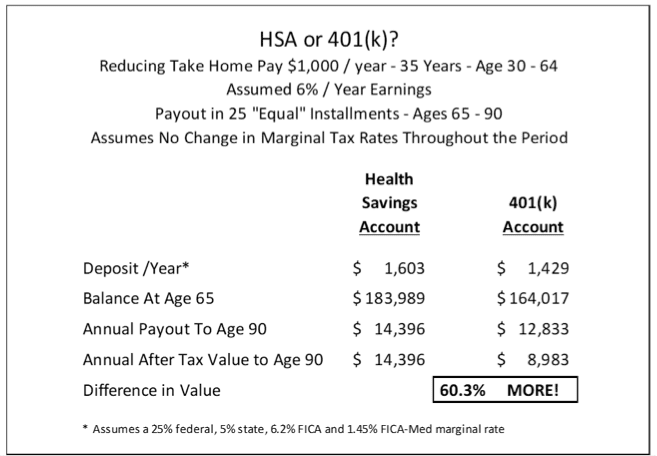

For skeptics, I compared the net, after-tax value of contributions to a 401(k) and an HSA when it comes to preparing for medical costs in retirement. My example reduces take home pay by $1,000 a year for 35 years, working from age 30 through age 64, where the monies would be paid out in 25 equal installments to cover medical and long term care insurance premiums and out of pocket expenses in retirement, ages 65 to 90.

HSA contributions through a cafeteria plan are “triple-tax-free” (pre-tax for federal and state income taxes, pre-tax for FICA and FICA-Med employment taxes, tax deferred on earnings, and tax free upon payout to cover Qualifying Medical Expenses). So, HSA assets have a much higher value to workers in terms of financing retiree medical and long term care insurance premiums and out-of-pocket expense needs.

However, in my second presentation, titled HSA Chicken or 401(k) Nest Egg, Prioritizing Contributions, I confirmed that fully funding the HSA first isn’t always the best strategy for every worker. I offered the following guidance:

- For workers who can, they should max out contributions to both the HSA and the 401(k), including catch-up,2

- For workers who can’t max out, they should be sure to contribute enough to each plan/program (including, as applicable, a working spouse’s employer’s plan/program) so that they obtain the maximum employer financial support, and

- For those who can’t max out, there is a “common sense” order of contributions that will allow each worker to take advantage of two design features:

- First, workers can almost always prospectively change their contributions to the 401(k) and the HSA,3 and

- Second, a well-designed 401(k) offers sufficient liquidity to enable workers who live payday to payday to use plan loans to maximize tax-preferenced contributions to both programs.4

Save early, save often, and for most workers, save as much as you can in both accounts.

*If you disagree, send me a note, [email protected] to explain why you believe it would be a mistake for your organization to adopt a HSA-capable health option. Don’t even think about calling the health coverage a “High” Deductible Health Plan. That would be a misnomer. Reminds me of the name we first used to describe 401(k) plans – “salary reduction savings plans.” Great marketing, eh!? The minimum deductible for a HSA-capable health option in 2018 is $1,350. Kaiser confirms that the average general deductible for single coverage in 2018 was $1,573. Even the 2018 Medicare Part A deductible is $1,340. See Kaiser Family Foundation, 2018 Employer Health Benefits Survey, 10/03/18. https://www.kff.org/health-costs/report/2018-employer-health-benefits-su...

1 See my prior HSA blogs: at www.psca.org/blogs

2If a financially successful retirement is a priority, consistent, significant saving are required. According to Aon, The Real Deal, Retirement Income Adequacy at U.S. Plan Sponsors, 2018, many workers will need at least 11 x pay in order to be financially prepared to retire at age 67 and maintain their pre-retirement standard of living. According to EBRI, Savings Medicare Beneficiaries Need for Health Expenses: Some Couples Could Need as Much as $370,000, 2017, a 65 year old man needs to have accumulated $131,000 ($147,000 if a woman) to have a 90% chance of having enough savings to cover premiums for Medicare Part B, Medicare Part D and a Medicare Supplement, as well as out-of-pocket spending for outpatient prescription drugs. Those numbers do not adjust for taxes nor do they include potential long term care, dental or vision expenses not covered by Medicare. Maximization of contributions is an appropriate strategy for many because: (1) HSA assets will be used to cover both current and future medical expenses, (2) Only a minority of employers currently offer access to a HSA-capable health option, and (3) Over half of American workers are 42 years of age or older.

3A plan sponsor can adopt plan provisions that enable workers to prospectively change 401(k) and/or HSAs contributions at any time. Where the employer financial support is in the form of a matching contribution, the plan sponsor can adopt “true-up” provisions so that the employer financial support is the same regardless of when contributions are made during the year.

4J. Towarnicky, It is Not Borrow to Save, But Save to Borrow! 10/09/18, Accessed 10/10/18 at: https://www.psca.org/blog_jack_2018_45