Advertisement

Retiree Medical Super Hero – The Health Savings Account

“An investment in knowledge pays the best interest.”1

This is the third of three posts – this post is focused on funding future medical expenses.

In part 1 of this three-part series, I highlighted and estimated the costs for a Medicare-eligible retiree:

- “Most of your retirees qualify for non-contributory Medicare Part A hospital coverage (by paying Medicare HI taxes (FICA-Med)) and most won’t be subject to the income-based contributions for Medicare Part B and Medicare Part D. So, a retiree’s cost may be $494.69/month, $5,936.28/year; $989.38/month, $11,872.56/year for a couple, both age 65.”

In part 2 of this three-part series, I suggested that the current cost-sharing and premium structure is unlikely to be sustainable and that we can’t count on current workers and future generations to shoulder the ever-increasing burden: expecting our economy will ultimately apply all these projections look like great candidates for something called Stein’s Law2: "If something cannot go on forever, it will stop."

- “For a worker age 50 today who will reach age 65 in 15 years in 2034 … The premium costs shown (above) will increase assuming 4%/year inflation: $891/month, $10,691/year, for a couple, $1,782/year, $21,382/year, assuming 7%/year inflation: $1,365/month, $16,378/year, $2,730/month, $32,757/year (couple). Point-of-purchase cost sharing for a Medicare beneficiary will increase assuming 4.25%/year inflation: Part A Deductible – from $1,364 to $2,546, Part B Deductible – from $185 to $345.”

Clearly, increased taxes are in our future – if not next year, then by 2026!3

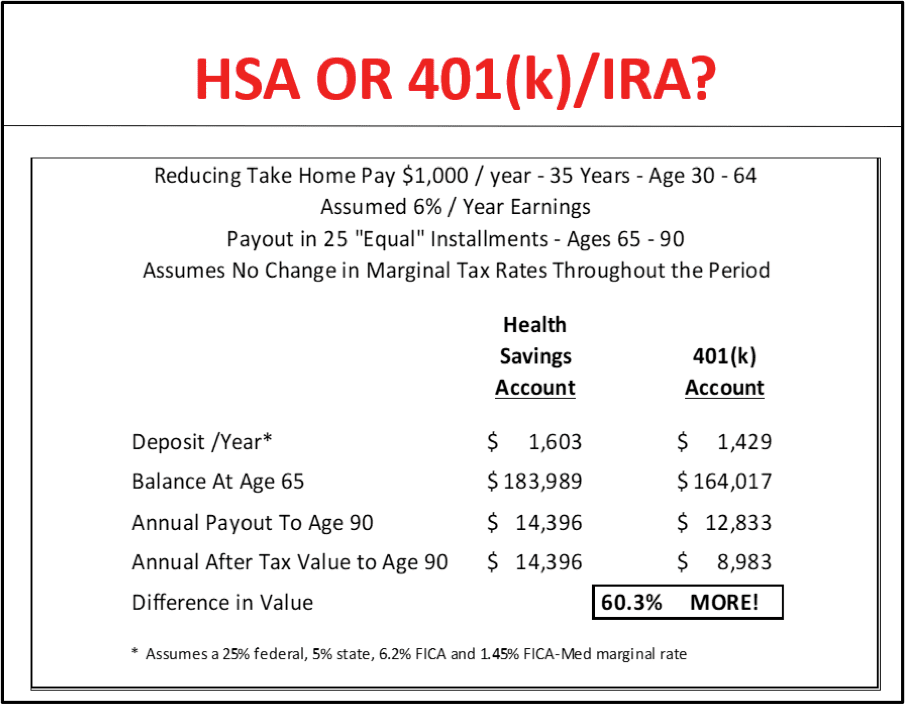

Health Savings Account super hero to the rescue!4 Most retirement professionals agree that medical costs, premiums and out of pocket expenses are the largest expense workers face in retirement. So, why did you and more than 85% of other employers deny your employees access to the most tax-efficient option for funding retiree medical expenses in each of the past 15 years?! Why don’t you offer HSA-capable health options – given their superiority for funding retiree medical costs (author’s calculations)?

Firms that offer access to HSA-capable health options are helping workers avoid over-insurance, accumulate savings5, while concurrently gaining a competitive advantage on you!

There are many reasons why you and/or your senior leadership team may have resisted HSA-capable health coverage in the past – perhaps you believe that a “high” deductible will impede workers who need care. But, the fact is that even a deductible of $500 may be too much for a sizeable minority of Americans – as only 61% believe they have $400 on hand to meet an unexpected expense.6 So, if you continue to offer coverage with a lower deductible while charging workers higher contributions, many will likely continue the higher cost option because they have no savings and are living paycheck to paycheck.7 Do you really want to continue that status quo? Remember, it won’t be enough to just offer HSA-capable health options, you must also prompt contributions to the HSA. If you do, studies show workers who have accumulated HSA assets do use health care services.8

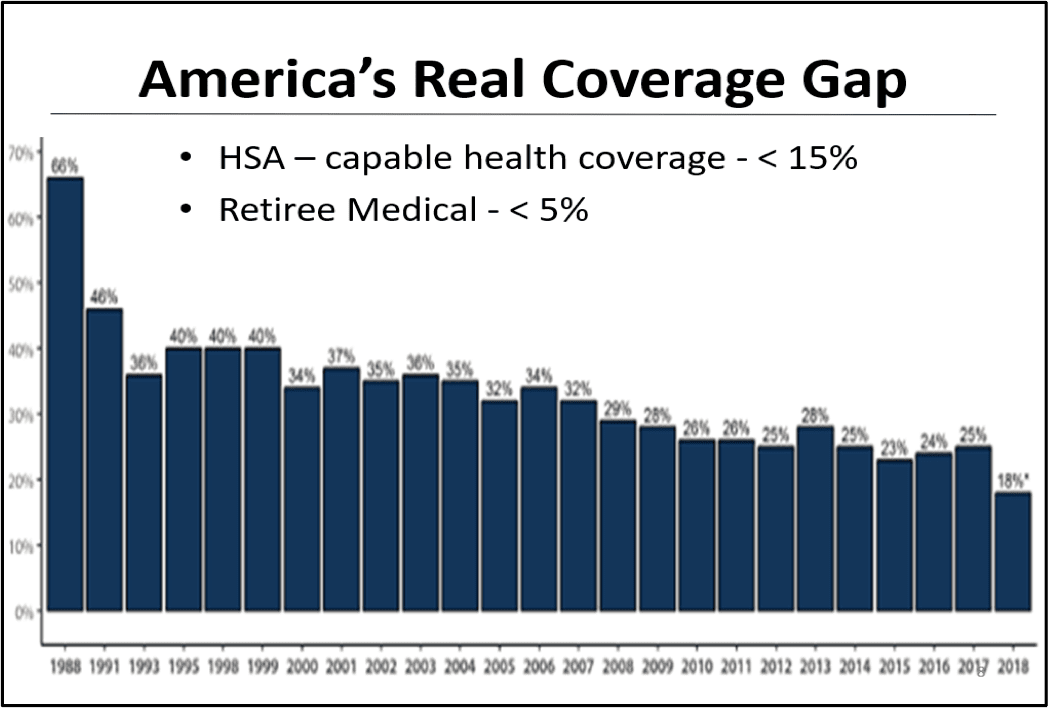

Finally, just like Batman and Robin, the Health Savings Account (and HSA-capable health option) has a sidekick – the Medicare private exchange (including employer-sponsored, retiree-pay-all, fully-insured Medicare Supplement and/or Medicare Advantage options).9 As you know, most employers never offered retiree medical coverage and most never will. Further, most employers who once offered retiree medical coverage have curtailed that coverage or eliminated it:

While 18% of large employers responding to the survey confirmed that they offer health coverage to retirees, that likely includes legacy provisions – grandfathers, red circles or transition coverage. Estimates are that less than 5% of employers offer retiree medical coverage to new hires. So, if you do (even fully-insured, retiree-pay-all coverage limited to Medicare beneficiaries), you’ll gain a competitive advantage in at least two ways:

- Offering younger workers a target for their HSA savings, and

- Creating a transition opportunity for older workers by offering access to tax-favored medical coverage.

My final bet: If you offer HSA-capable health options and employer-sponsored, retiree-pay-all, fully-insured, Medicare Advantage and/or Medicare Supplement coverage10, you won’t regret it. And nor will your employees!

PSCA will conduct a webinar on July 25th to review the results of our Health Savings Account (HSA) survey. The HSA is the most valuable benefits tax preference offered in the Internal Revenue Code – a worker’s most tax-efficient opportunity to accumulate assets for funding medical costs in retirement!

Save the Date — 2020 PSCA National Conference! May 13–15, 2020 at Hilton Riverside in New Orleans, LA

We are providing this information to you solely in our capacity as individuals with knowledge and experience in the retirement industry and not as legal advice. The issues presented here may have legal implications. We recommend discussing these matters with your legal counsel before choosing a course of action. This memorandum (email, publication, etc.) was prepared to support the informational needs of the Plan Sponsor Council of America on the issues discussed. If this memorandum is shared, recipients should understand that (1) the memo focuses on the needs of our association and the issues of interest to association members, and (2) it is not (and you/others should not use it as a substitute for) legal, accounting, actuarial, or other professional advice.

IRS CIRCULAR 230 NOTICE: Any advice contained in this document was not intended or written to be used and cannot be used by the recipient or any other person, for the purpose of avoiding any Internal Revenue Code penalties that may be imposed on such person [or to promote, market or recommend any transaction or subject addressed herein]. Recipients of this document should seek advice based on their particular circumstances from an independent tax advisor.

1Ben Franklin

2Wikipedia, Herbert Stein. Stein propounded Stein's Law, which he expressed in 1976 after analyzing economic trends (such as rising U.S. Federal debt in proportion to GDP, or increasing international balance of payments deficits, in his analysis). If such a process is limited by external factors, there is no urgency for government intervention to stop it, much less to make it stop immediately; it will stop of its own accord. Accessed 7/4/19 at: https://en.wikipedia.org/wiki/Herbert_Stein

3Board of Trustees, 2019 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds, 4/22/19, Accessed 7/4/19 at: https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Tren...

4K. Forsythe, Empower, G. Kvadus, Optum, M. Ikard, Atrium Health, Health Savings Accounts: Retirement Superhero in Disguise, 2019 PSCA National Conference, May 2019; See also: J. Towarnicky, Marvel-ous! The HSA: A Retirement Superhero in Disguise, 4/23/19, Accessed 7/4/19 at: https://www.psca.org/blog_jack_2019_25

5J. Towarnicky, Impediments to Saving for Retirement – The Barriers, Part 1, 11/5/18, Accessed 7/4/19 at: https://www.psca.org/blog_jack_2018_50

6Federal Reserve Board, Report on the Economic Well-Being of U.S. Households, 5/23/19, Accessed 7/4/19 at: https://www.federalreserve.gov/newsevents/pressreleases/other20190523b.htm

7American Payroll Association, Getting Paid in America, September 2018. See Question 6 where 71% of responding workers confirmed that they would have some or significant difficulty meeting their current financial obligations if their next paycheck was delayed one week! Accessed 7/4/19 at: https://www.nationalpayrollweek.com/wp-content/uploads/2018/10/2018Getti...

8P. Fronstin, M. C. Roebuck, Do Accumulating HSA Balances Affect Use of Health Care Services and Spending? 5/23/19, Accessed 7/4/19 at: https://www.ebri.org/publications/research-publications/issue-briefs/con...

9J. Towarnicky, But I Repeat Myself – You Should Offer a Fully-Insured, Retiree-Pay-All, Employer-Sponsored, Medicare Advantage Option to Retirees, 2/7/19, Accessed 7/4/19 at: https://www.psca.org/blog_jack_2019_8

10Carefully, including a reservation of rights clause that would allow you to terminate the coverage at any time.