Advertisement

Retirement Super Villain – Retiree Medical – A Growing Threat

A revelation! Retiree medical rides alongside pestilence, war, famine and death.1

This is the second of three posts on retiree medical - this post is focused on future retiree medical costs.

In part 1 of this three-part series, I highlighted and estimated the costs for a Medicare-eligible retiree:

“Most of your retirees qualify for non-contributory Medicare Part A hospital coverage (by paying Medicare HI taxes (FICA-Med)) and most won’t be subject to the income-based contributions for Medicare Part B and Medicare Part D. So, a retiree’s cost may be $494.69/month, $5,936.28/year; $989.38/month, $11,872.56/year for a couple, both age 65.”

While health reform did little to curb medical inflation, Congress took action long ago to limit cost increases for Medicare beneficiaries. During the more than 35 years since 1983, the average annual inflation rate was about 4 percent per year. For example, since 1983, Part B premium has seen average increases of just less than 7 percent per year (from $12.20 to $135.50). The Part B deductible has increased almost 2.5 percent per year (from $75 to $185). The Part A deductible has increased 4.25 percent per year (from $304 to $1,364).2

However, even continuation of those modest rates of inflation creates a significant challenge for workers who are preparing for retirement in the future.

For a worker age 50 today who will reach age 65 in 15 years, in 2034:

- The premium costs shown in the prior blog post will increase:

- Assuming 4%/year inflation: $891/month, $10,691/year, for a couple, $1,782/year, $21,382/year,

- Assuming 7%/year inflation: $1,365/month, $16,378/year, $2,730/month, $32,757/year (couple). - The current point of purchase cost sharing for a Medicare beneficiary will increase:

- Assuming 2.5%/year inflation:

• Part A Deductible – from $1,364 to $1,975

• Part B Deductible – from $185 to $268

- Assuming 4.25%/year inflation:

• Part A Deductible – from $1,364 to $2,546

• Part B Deductible – from $185 to $345

For a worker age 22 today, who will reach age 65 in 43 years in 2062:

- The premium costs shown in the prior blog post will increase:

- Assuming 4%/year inflation: $2,672/month, $32,059/year, for a couple, $5,343/year, $64,118/year,

- Assuming 7%/year inflation: $9,075/month, $108,897/year, $18,150/month, $217,795/year (couple) - The current point-of-purchase cost sharing for a Medicare beneficiary will increase:

• Assuming 2.5%/year inflation:

- Part A Deductible – from $1,364 to $3,944

- Part B Deductible – from $185 to $535 - Assuming 4.25%/year inflation:

- Part A Deductible – from $1,364 to $8,167

- Part B Deductible – from $185 to $1,108

All these projections look like great candidates for something called Stein’s Law3: "If something cannot go on forever, it will stop." Others have paraphrased Stein’s Law as: “Trends that can't continue, won't."

Long ago, in my last plan sponsor position, I did a similar projection for medical spending out to 2080 – noting that current health care spending as a percent of GDP was 16%, and that at double digit inflation rates, health care spending would crowd out all other goods and services – becoming 100% of GDP! I invoked Stein’s Law, joking that it must be true, because otherwise: “All Americans won’t be flipping each other’s hamburgers or greeting each other at Walmart, but administering each other’s meds.”

Most of Medicare is funded by current workers: wealth transfers from the current workforce to current retirees. That is how Medicare has been financed in the past. So, we can just ask current workers to pay more, right? Or perhaps we can tap all those millionaires and billionaires, right?

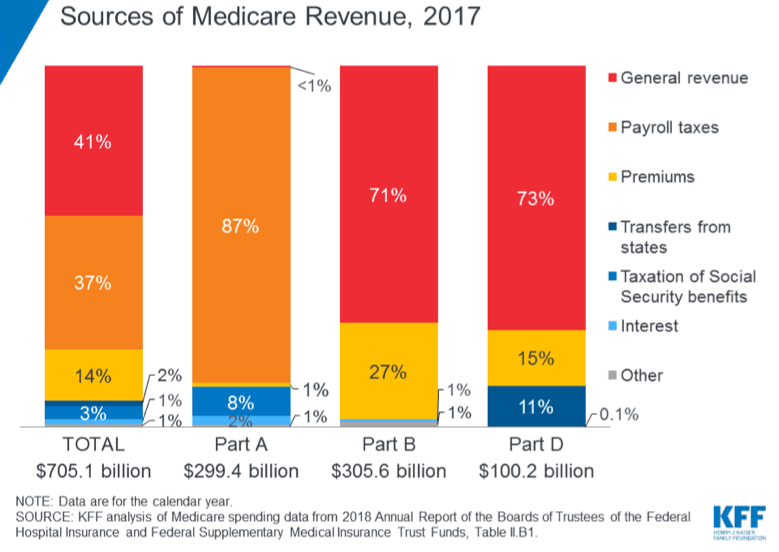

Not likely. Even maintaining the status quo means an ever-increasing, ultimately overwhelming burden on current workers. Don’t forget that working Americans already shoulder most of the cost of Medicare benefits:

- Part A, hospital insurance, funded mostly as a 2.9% tax on wages4, $293 billion in outlays5,

- Part B, physician and outpatient services, $309 billion in outlays where approximately three-fourths are funded by general revenues (income taxes), and

- Part D, prescription drugs, $100 billion in outlays where three-fourths are funded by general revenues.

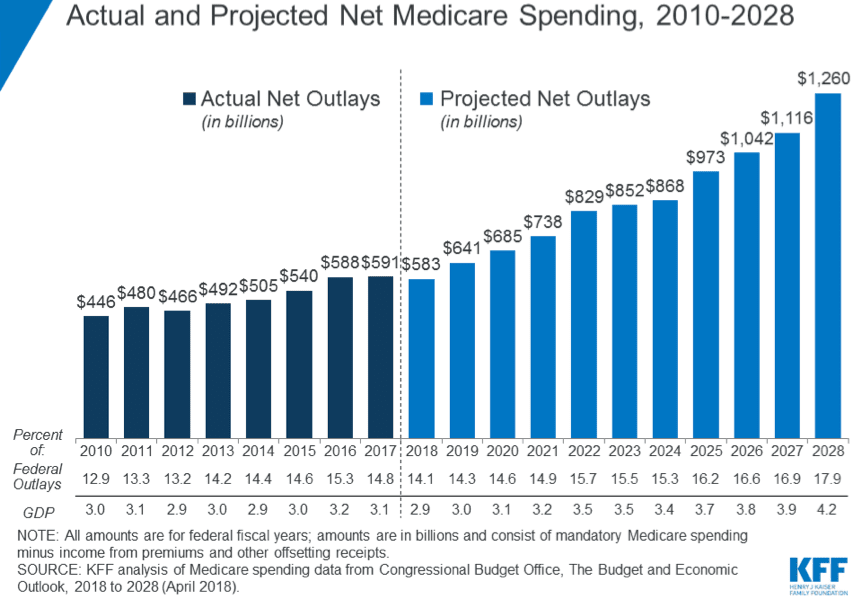

And, with the retirement of the baby boomer generation, Medicare spending is projected to more than double in the next 10 years6:

Finally, as recently confirmed by the Social Security/Medicare Trustees, the Medicare Trust Fund will be exhausted by 2026 – less than seven years from now!7 So, the current funding scheme is inadequate!

Time for a second bet. My bet is that, more and more, your workers know of these looming challenges. At the PSCA 2019 National Conference, one breakout session focused on retirement decision-making challenges.8 Survey results presented at the conference confirmed that 54% of workers expect to retire after age 65 or do not plan to retire, and 55% of surveyed workers plan to work after they retire.9

When asked why they were planning on continuing employment, the reasons given included:

- 53% - need the income,

- 35% - can’t afford to retire,

- 35% - concerned about Social Security,

- 29% - need health benefits, and

- 17% - concerned about employer retirement benefits.

Simply, it is increasingly clear that a worker’s inability to prepare for retirement may negatively impact both the worker and the organization. Are you as concerned about your workers’ preparation for retirement as they are?

PSCA will conduct a webinar on July 25 to review the results of our Health Savings Account (HSA) survey. The HSA is the most valuable benefits tax preference offered in the Internal Revenue Code – a worker’s most tax-efficient opportunity to accumulate assets for funding medical costs in retirement!

Save the Date: 2020 PSCA National Conference! May 13–15, 2020 at the

Hilton Riverside in New Orleans, LA

1V. Vasnetsov, Four Horsemen of the Apocalypse, 1887. Depicted from left to right are Death, Famine, War, and Conquest.

2Social Security, Accessed 7/4/19 at: https://www.ssa.gov/policy/docs/statcomps/supplement/2015/2b-2c.html#tab...

3Wikipedia, Herbert Stein. Stein propounded Stein's Law, which he expressed in 1976 after analyzing economic trends (such as rising U.S. Federal debt in proportion to GDP, or increasing international balance of payments deficits, in his analysis). If such a process is limited by external factors, there is no urgency for government intervention to stop it, much less to make it stop immediately; it will stop of its own accord. Accessed 7/4/19 at: https://en.wikipedia.org/wiki/Herbert_Stein

4Most workers pay 2.9% of wages throughout their entire lifetime (half assessed against workers, the other half assessed against their employers), minimum 40 quarters. During the period 1966 through 1985, the Medicare Hospital Insurance (HI) tax rate increased gradually from .35% to 1.35%. In 1986 and subsequently, the HI tax rate has been 1.45% for employees and employers. The wage base maximum was the same as for Social Security during the period 1966 – 1990. The taxable wage base was $51,300 (1990, maximum tax of $1,487.70). Separate HI taxable wage base maximums applied in 1991 – 1993:

• 1991: Social Security - $53,400, Medicare - $125,000 (maximum tax of $3,625, a 153% increase)

• 1992: Social Security - $55,500, Medicare - $130,000 ($3,770)

• 1993: Social Security - $57,600, Medicare - $135,000 ($3,915)

After 1993, there has been no limitation on HI-taxable earnings. The Patient Protection and Affordable Care Act of 2010 (Health Reform) added a .9% Medicare surcharge for wages in excess of $200,000 in a calendar year, without regard to tax filing status.

5J. Cubanski, T. Neuman, The Facts on Medicare Spending and Financing, Kaiser Family Foundation, 6/22/18, Accessed 7/4/19 at: https://www.kff.org/medicare/issue-brief/the-facts-on-medicare-spending-...

6Note v, supra

7Board of Trustees, 2019 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds, 4/22/19, Accessed 7/4/19 at: https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Tren...

8P. Rowey of the Transamerica Institute® and Transamerica Center for Retirement Studies® and M. Howell, Prudential Financial, May 2019

9Transamerica, A Precarious Existence: How Today’s Retirees Are Financially Faring in Retirement contains findings from Transamerica Center for Retirement Studies’ (TCRS) 2018 Survey of Retirees. Transamerica, What Is “Retirement”? Three Generations Prepare for Older Age contains findings from the 19th Annual Transamerica Retirement Survey of Workers.