Advertisement

Brokerage Window Availability

Sponsored by MFS Investment Management.

While the uptake of ESG funds and other alternatives remains low, we have heard anecdotally from plan sponsors that they offer a brokerage window for participants who want access to those fund types without having to add a specific ESG fund to the lineup. I wondered if the availability of brokerage windows has increased over time – at one point 15 or so years ago they were more common and started to decline in popularity.

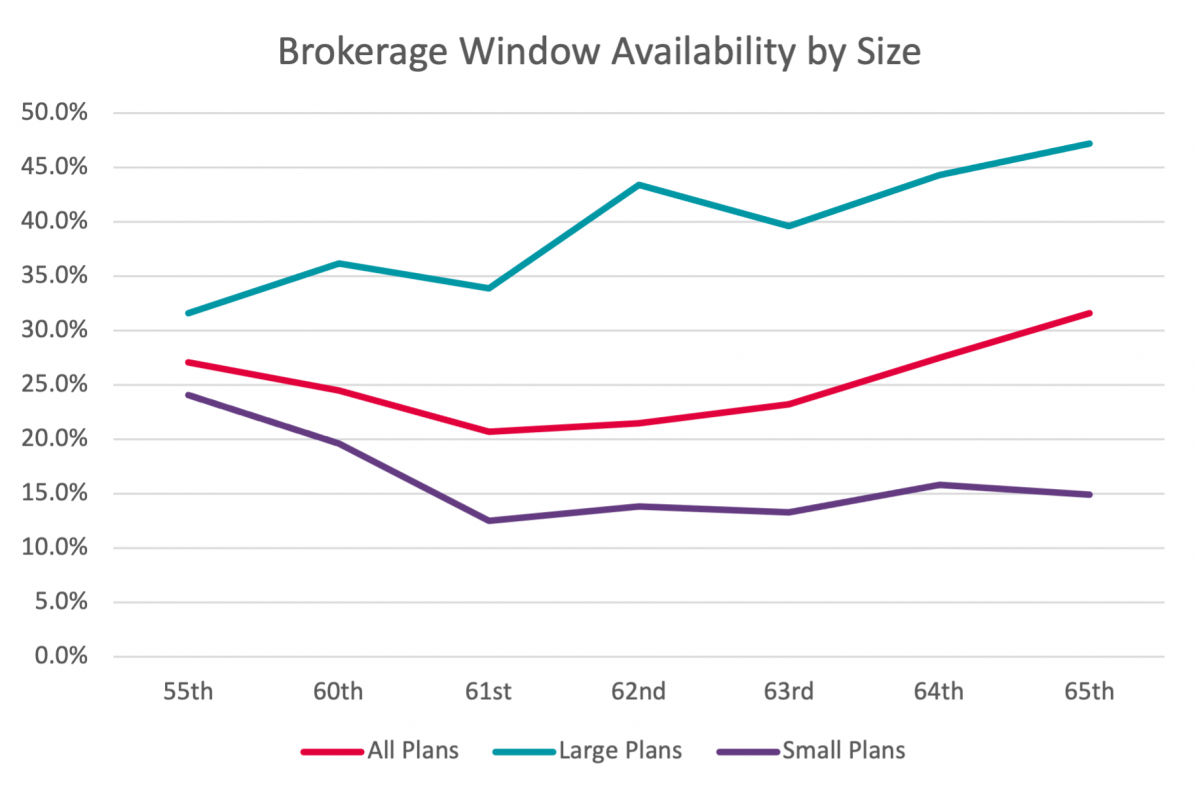

Looking at PSCA’s Annual Survey data over time, we see that there has been an increase in brokerage window availability the last few years with 31.6 percent of plans offering one according to the 65th Annual Survey (reflecting 2021 plan data). However, there is a size correlation with large plans much more likely to offer one. Nearly half of plans with 5,000 or more participants offer one, versus 15 percent of plans with fewer than 50 participants.

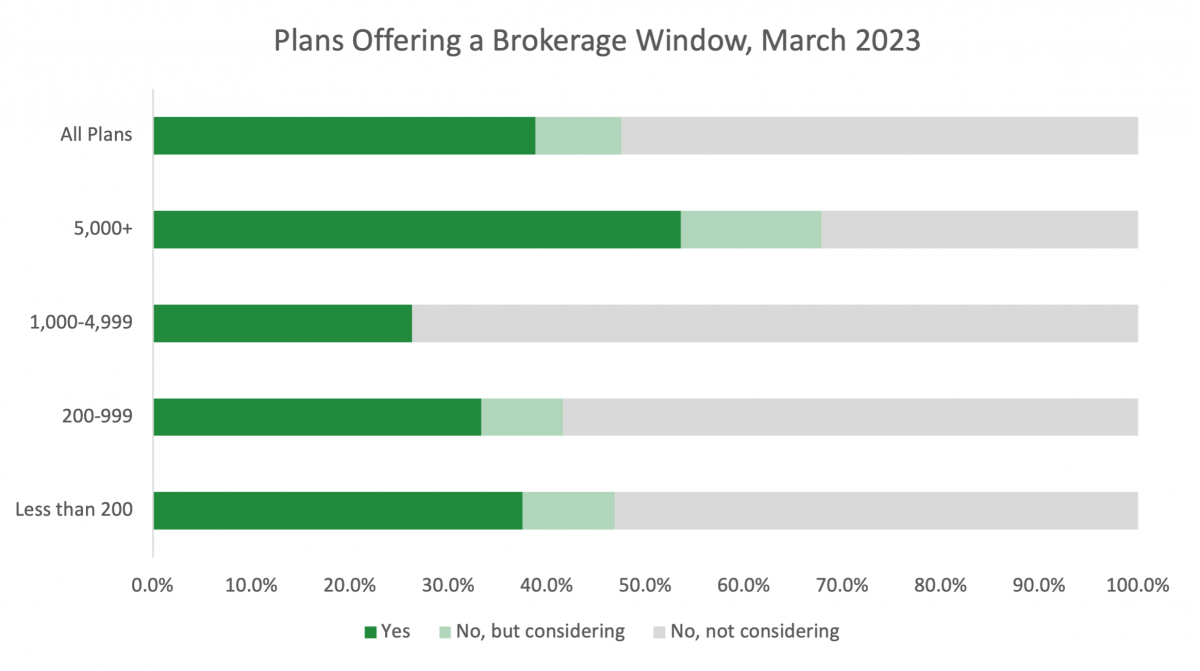

To see if this increase in availability is correlated to plan sponsors adding choice for options such as an ESG without adding a designated ESG fund, we asked plan sponsors in this week’s Question of the Week if they offer one, and why. Nearly 40 percent of respondents (38.8%) offer a brokerage window with nine percent considering one. This includes 53.6 percent of large plans that offer one and 14.3 percent considering it.

I do think this is a trend to watch as plan sponsors balance offering choice to participants who want it with fiduciary concerns regarding adding additional specific funds to the lineup. Many that do offer a brokerage window limit it in some way to address some of the fiduciary concerns of offering a window. Some respondents indicated they have a more investment-savvy workforce with participants asking for the window, whereas other companies feel their workforce is not as investment savvy and offering a window would not be appropriate for their employee base. Comments from respondents by availability of brokerage windows follows.

Offer brokerage window:

- Ease of one company to offer staff other investment options.

- Expands investment options for those that are looking for a specific stock, fund etc.

- Flexibility for the few participants who want it.

- It allows savvy participants to purchase stocks, bonds, ETFs and ESG funds of their preference.

- Maximum exposure is limited to 50% of retirement plan assets and only mutual funds.

- Offer brokerage limited to mutual funds. Helpful as transition from one line-up to another. Provides outlet for choice for plan participants.

- Our brokers utilize the window to determine participants' retirement and financial wellness in order to provide more in depth guidance and recommendations.

- Participants wanted the freedom to invest in stocks and funds of their individual desires that were outside the plan fund offering.

- The majority of our participants benefit from our strong line-up of target-date and index funds but some of our people consider themselves sophisticated investors and wanted more options.

- There are savvy investors who benefit from this option - especially the pre-tax contribution factor.

- To give employees additional investment opportunities

- To give participants an option to reach out for investment advice.

- We believe it provides a good option for those more sophisticated investors in our plan. That said, there is very low participation in this option.

- We chose to offer a brokerage window to permit participants to select religiously compliant, ESG or other funds. Also helped with recent acquisition.

- We employ several physicians as a healthcare organization and this option was driven by providing these employees the additional investment choices.

- We have about 20% of our plan participants use the brokerage window as we are a financial firm with more investment savvy participants. We offer only mutual funds and ETF's in our window and not individual stocks.

- We have offered a brokerage window for about 1 year. We only have about 4 participants currently using this feature. We feel it give someone who is a savvier investor more investment options. We knew from the beginning there would be limited use and we are ok with that.

- We offer a brokerage window to provide additional choice and control by the participants of their investments.

- We offer a limited window. It offers all Vanguard and TIAA funds only. Not a true brokerage window because we wanted to limit the fund availability.

- We offer this option as there was enough of an interest from our professionals.

- Wish we did not offer this. There are only about 8 participants using this feature and it is an extra burden to administer.

- Works for right participant base

Considering:

- It is under consideration.

- to offer more stable rates

- We closed our brokerage account a few years back as there was pending legislation putting the Fiduciary committee at risk. That legislation did not pass so we may reconsider.

- We do not have one now, but we are considering adding one to allow participants more flexibility and choices when making investing decisions.

Not offered and not considering:

- Concerns with investment committee fiduciary obligations

- Cost and low interest in option. Adds sophistication level.

- Educating employees would be difficult, most of our participants default to TDF's and are uninterested in selecting other investments offered in the plan.

- Employee population would NOT know how to use/ manage

- Fiduciary concerns

- Fiduciary concerns and administrative complexity for an option likely to be utilized by a very small group of participants.

- Fiduciary perspective...prudent person rule.

- I feel we are too small in both company size and assets to offer.

- It has not been requested by participants. I do have a concern that with a brokerage option some might take on more risk than they realize and/or trade excessively. I would not consider the great majority of our plan's participants as being sophisticated investors.

- It is an unnecessary complication to the plan and would only apply to a very small group of employees.

- Just no desire to go that route. We just want to stay with investments.

- No one has asked for it and we already have over 20 fund options. However, we are switching recordkeepers so now might be time to consider.

- No participant demand for and expected usage is low for the cost and complication of adding one.

- Not appropriate for majority of our participants.

- Not requested by participants

- Opens up too many potential issues/liability.

- Our investment lineup is fairly thorough, so we don't feel a need for a brokerage window.

- Our plans do not offer a brokerage window because of administrative complexity, the Plans offer a comprehensive platform of investments and we have little participant demand.

- Survey results suggest self-managed investments do poorly compared to professionally managed. We don't see compelling reasons to encourage self-management. Few participants would take advantage of it anyway.

- Too many changes going on in our plans already with Secure. Not the right population for brokerage window.

- We did in our old 401(k) plan and it was a disaster.

- We like to keep our plans simple and feel brokerage investing is best done outside the plan.

- We offer a basic plan, haven't looked into the cost to offer more investment options

- We offer a brokerage window in our 457(b) plan with very little participation so there is no interest in mirroring this offering in our 403(b)/401(a) benefit program.

- Would increase complexity and create confusion