Advertisement

Mandating Plan Eligibility at Age 18

Sponsored by MFS Investment Management.

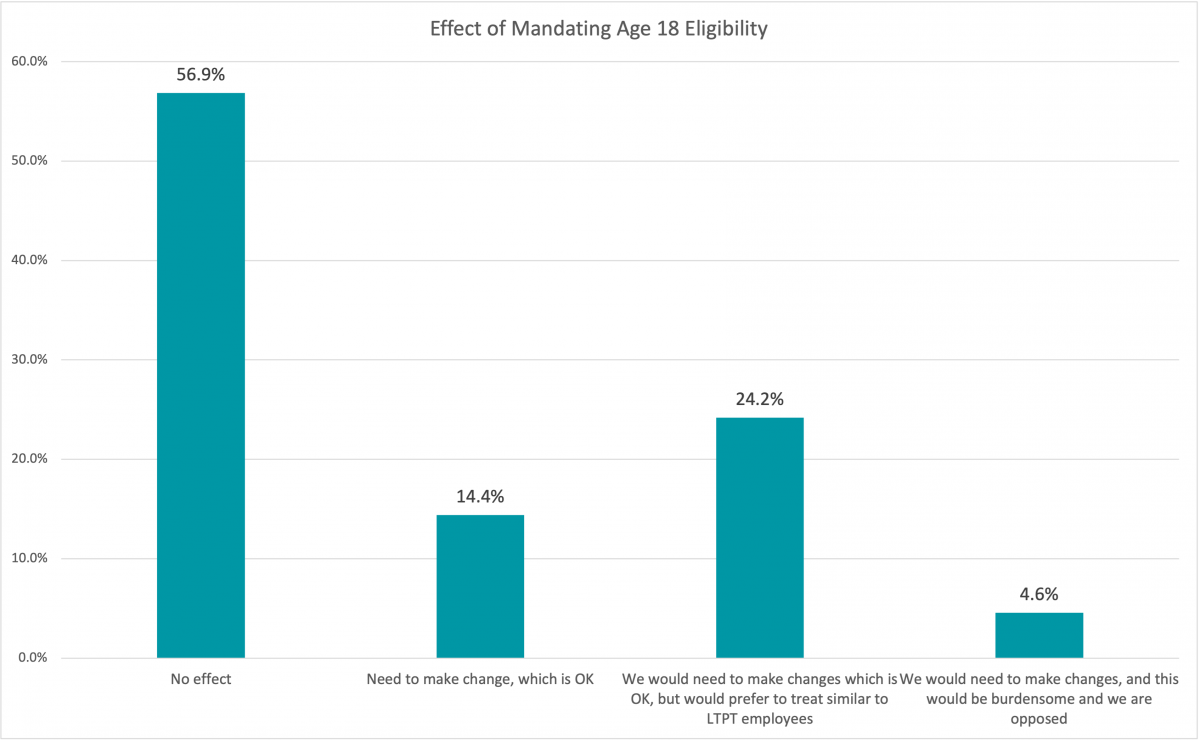

There is a proposal in Congress to change the minimum age requirement from 21 to 18 years old. PSCA annual survey data shows that 40 percent of plans currently have a minimum age requirement of 21, where the rest have either no minimum age requirement or already have an age 18 minimum. We wanted to know what impact this change would have on plans if organizations were mandated to allow all employees aged 18 or older to participate. We also wanted to know if employers that would have to make changes would prefer to have an exemption from testing and employer contributions for this group, similar to the LTPT employee exemption in SECURE 1.0.

More than half of respondents stated that this change would have no impact on their plan, they already allow those employees to participate. Fifteen percent of respondents stated that they would need to make changes/update the plan document but that is OK, it would not be burdensome and they would provide employer contributions as they do other employees (many in this group indicated they have very few, if any, employees under the age of 21). While 4.6 percent of respondents stated they are opposed to this change as it would be burdensome, a quarter of respondents stated they would be OK with making this change, but they would prefer the exemption to testing and contributions.

We then asked respondents if they thought this regulatory change would be good, bad, or if they were indifferent to it, and what other thoughts they have about this potential change. A large number are respondents are in favor of getting employees to save as early as possible ("the earlier the better!") and see this as a positive change. And while a few are concerned about the impact on testing as they feel this group is unlikely to participate and it will lower their participation and deferral rates, others are concerned that there tends to be high turnover in this age group (or they are seasonal, interns, etc.) it would be administratively burdensome and could result in a lot of additional small balances, especially if the plan has automatic enrollment.

See the full comments below.

- Bad - would create even more people to have to locate for the plan.

- Bad, at that age people move jobs a lot which could cause an adverse affect for the small accounts and administrative fees to upkeeping

- Bad...younger employees are less likely to contribute and this would unfavorably skew our ADP/ACP testing

- Could help with retention of employees

- Don't believe mandating is the answer even though it really wouldn't affect us.

- Good

- Good

- Good

- Good

- Good

- Good

- Good

- Good - the earlier they start the better

- Good idea

- Good thing! Saving early is never bad.

- Good to get them started as young as possible!

- Good, increase the benefit to more employees

- Good, start saving earlier

- Good!

- Good! I say if that's the legal age when people become adults, that's when they should be eligible to participate in a retirement plan. The younger people start saving for retirement, the better off they will be in the long run.

- Good. Get kids started early on saving for retirement. Bad. Can be administratively burdensome to some employers with younger workforce.

- Good. The younger you can get them going on it the better off they will be. Plus they won't miss it if it starts from the beginning.

- Good. The earlier the better

- Good. The sooner they start saving the better. I wish someone would have told me to start saving for retirement right when I entered the workforce.

- Good. We're always preaching to start saving early.

- Good...start them young and get them used to saving

- Great

- Great idea - Statistics support those who save sooner have more later. Good habit to start.

- Great! Why keep young adults from starting to save as soon as possible?

- High turnover on this age group would concern me, but not that much different than 21 year olds

- I don't have any objection to making eligibility mandatory at 18; in my experience of my company's plan, we rarely have employees under 25 opting to join the plan anyway. Based on that, I think lowering the eligibility age would have little to no impact on our participant uptake. Having said that, allowing someone to join a plan and prepare for their retirement earlier is never a bad thing.

- I don't think is a bad thing. It gets burdensome if you have high turnover and need to administer the plan.

- I think earlier is better. Let's get the compounding started as soon as possible. Some retail/fast food places may find this to be an administrative nightmare as their workforce can be transient. But all in all - starting saving is always a good thing.

- I think enrolling individuals early is never a bad thing. Already considering this without a mandate.

- I think it would be a good way to help the younger generation know the importance of saving.

- I think it would be ideal - it will give younger employees an additional 3 years to contribute towards their retirement. The harder thing will be to educate these employees so they will take advantage of it.

- I think it's a good idea so the employee can start saving earlier.

- I think it's a good idea; youth need to understand the benefits of saving at an early age.

- I think it's a good thing. The earlier you can save, the better.

- I think it's unnecessary. I don't think 18 year olds value a retirement plan.

- I think its not a bad idea so people can start saving even earlier

- I think this is great, it adds on a few more years for some to start saving and get that compounding. I think it also would show the importance on getting in early and not waiting.

- I think this would be a positive move.

- I used to think this would be bad, but we have one employee under 21 that deserves to participate in 401(k).

- I would welcome to change it will give younger workers an opportunity to Start contributing to a retirement plan, preparing them for long term benefits.

- If an 18 YO is able and smart enough to save for retirement, why would we prohibit that?

- If we were required to make these changes, we'd prefer to treat similar as LTPT employees (no employer contributions/excluded from testing)

- indifferent

- indifferent

- Indifferent

- indifferent

- Indifferent

- indifferent

- Indifferent

- indifferent

- Indifferent

- indifferent

- Indifferent

- Indifferent

- Indifferent

- indifferent

- indifferent - although I don't see 18 as a long tenured employee, so there may be more forfeiture of non-vested dollars.

- Indifferent - not burdensome

- Indifferent - We rarely have employees under the age of 21.

- indifferent, probably not much of an impact

- Indifferent, would have to change plan, but only effects 1 current employee.

- indifferent; however, it would be good to ensure that all employees have the ability to start their retirement planning early.

- Indifferent.

- Indifferent.

- Indifferent... 18 year olds will want their money and not be concerned with starting to save 50 years out...doesn't mean they shouldn't but they will want their money in their pocket

- Indifferent...we rarely hire people under the age of 21

- It is a good idea to start savings at this age of 18.

- It is never to early to get people saving for retirement.

- It should be mandated that ALL fulltime employees, regardless of age, should be eligible for the plan.

- it's a good idea to help employees to start saving early and we should help to educate them.

- Lots of turnover in this age range. Great to provide plan to allow contributions at early age.

- Manufacturing would have higher admin costs due to turnover and RMD's

- Most likely it would make non-discrimination testing more difficult as this population would no longer be excludable.

- Mostly indifferent

- No issues with it. People should be able to save money for retirement as early as possible.

- Our 18 year employees are seasonal employees or interns, etc. They are not permanent employees. We have not collectively addressed the issue so I can’t speak to what we would or not do.

- Our age requirement for employees is 18. All employees, regardless of age, should qualify for employee benefits at time of employment.

- The biggest impact may be on the testing as including the youngest would decrease our average participation rate.

- The priority for 18-20 year olds should be with paying for college or trade school. Retirement savings begins once they have started their career or trade.

- The sooner folks start saving the better!

- The sooner they get in the plan the better, they are setting themself up for success at retirement.

- There would be an added cost for us as well. We offer a match to all participants including LTPT.

- Think would be a good thing as the early start will show the young how can build wealth for the future.

- This could incur significant cost for our plan, as we have a few thousand associates in this age group. We would need to review the analytics to project how many would participate and at what percentage, but would definitely be more than our current participation.

- Three more working years to save!

- We changed our plan's minimum participation age from 21 to 18 a few years back. The sooner employees are able to start putting money aside for retirement the better.

- We changed to 18 from 21 long ago. The ability for folks to start saving from an early age is important for retirement readiness.

- We don't have many younger employees, but i can see where this could be burdensome to administer.

- We generally don't hire anyone under 21 so it wouldn't have much effect on us. We have short term internships so potentially up to 3 additional people per year might be eligible for a couple months. I'm not sure any 18 year-olds would want to participate so the only issue I could see is them being auto-enrolled when they don't want to be (since our plan has auto-enrollment).

- We lowered our minimum contribution age to 18 in order to attract talent. Those extra 3 years of savings could make a world of difference in retirement!

- We permit participation under age 21, but match eligibility isn't until age 21. I would be in favor of the reduced eligibility age. Even though the company expense would increase, it would encourage employees to start saving earlier, which as we know, the longer period of time the monies are invested, the more likely they are to have more monies saved for retirement.

- We usually do not hire younger employees.

- We would change to match, no issues.