Advertisement

QOTW: Catch-ups as Roth

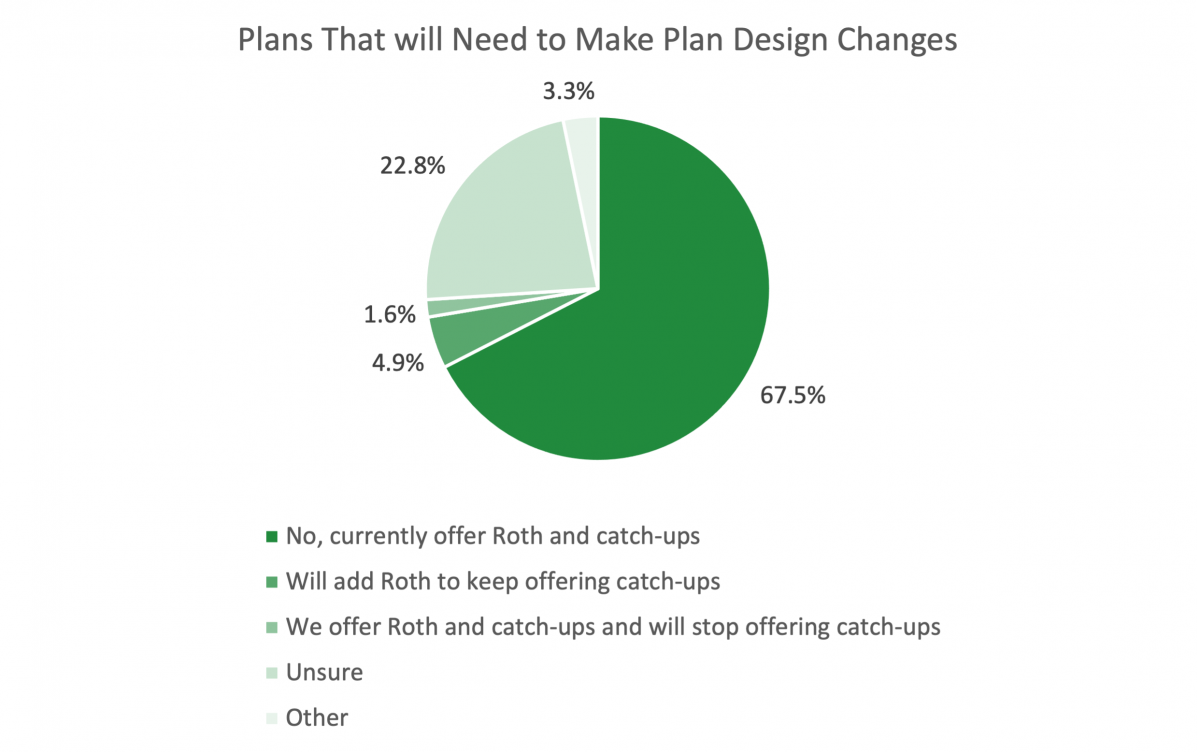

One of the revenue raising provisions of SECURE 2.0 is to require catch-up contributions to be Roth contributions for employees making $145k per year or more (the HCE definition). Though most plans allow catchup contributions, not all plans allow Roth (especially 403(b) plans). In this week’s QOTW we asked plan sponsors if they will need to make plan design changes to comply with this provision that goes into effect Jan 1, 2024.

More than two-thirds of respondents will not need to make plan design changes as they already offer Roth and catch-ups, though many are concerned about the income level threshold and the administrative complexity involved. They are waiting to hear from recordkeepers how this will work. Some are looking into whether the plan can designate all catchups as Roth to avoid the income level requirement and administrative complexity involved.

Comments from those that offer Roth and Catch-ups and will not need to make changes:

- Assume it will require a plan amendment to require.

- But concerned as to how this is going to be monitored (via recordkeeper, employer or self monitoring by employee)

- I dislike that catch up is Roth. More confusing will be the limit - as you may not know someone hits that limit until year end. That could be an issue (I have not read through the entire provision to see if once you reach $145,000 then in the next year you can not contribute)

- I'm concerned about the salary limit and making sure that is tracked correctly.

- Iven though we offer Roth and catch-ups, we still have to figure out how to administratively handle this new requirement.

- No plan design changes are needed. Unfortunately, it just adds additional administrative work over the holidays to ensure compliance.

- Not too much impact regarding secure 2.0

- System changes will be needed which take time and effort, but we are not opposed to doing that.

- The catch-up Roth change is a money grab by the government by being able to tax the 401K contributions

- This is a very messy provision and guidance is needed. Wish that all catch ups were Roth so we had a clearer road. We do NOT want to have to add separate elections but this is getting difficult.

- This may cause administrative burdens within our HRIS to monitor salary and make sure appropriate contributions are Roth only.

- Though to keep it simple wish NO income provision, much easier to do ALL catch-ups one method.

- We already offer both Roth and catchups, and already have a provision to make catchup contributions as Roth, so not likely to make any plan design changes for this.

- We are assuming our payroll provider will come up with a way to manage this within their system, and if so, as we already offer Roth and catch-ups there will be no change to plan design. If our payroll provider cannot manage this, then we'd look at plan design.

- We do not offer Roth option.

- We offer pre-tax and Roth catch-ups. Can we eliminate the pre-tax option in order to avoid possible administration issues? I would like to hear comments on this possibility.

- We pay bonuses in January, so this will be a little challenging to set up correctly so 401(k) catch-up can come out of that payment.

- We will just have to figure out how to handle Roth matches in our payroll system.

- We won't need to make plan design changes, but are still trying to figure out how to actually administer this.

- Will have to see if our payroll system can handle this complexity.

- Will need to change catch-up administration to point to Roth source and may need to add a separate Catch-up election %

Comments from those who are unsure:

- We currently offer Roth and catchups, but are concerned that the complexity of tracking and ensuring the provision is properly facilitated will bring additional administration and oversight with our TPA.

- Not well timed nor logical

- It's fine to require the ROTH but adding in the earnings threshold makes this too complex

- Ours is a multi-employer governmental 401(k) plan. It's voluntary and supplements a mandatory DB plan. The plan doesn't offer a Roth. State statute requires money in the plan be pre-tax. Adding a Roth component would be a considerable expense, as the pension administration system would need to be changed. In addition, the employers' payroll systems would also need to be amended to be able to transmit post-tax DC money to us. It's complicated.

- We already offer Roth and catch-ups but may make plan design changes depending on final administrative guidance.

- We haven't discussed anything yet. We're still digesting.

- We offer Roth and Catch-up already; so provisions are not a problem. Administration may be a hurdle for us but we are waiting for guidance from our counsel/ recordkeeper.

- We offer Roth but determining how the system can require to only take Roth contribution once reaching the catch-up amount.

Comments from those who will add Roth:

- Only if compensation levels dictate it. Hopefully provisions will be clearer.

- We are an MEP and this is going to be a giant pain in the butt; our 250+ employers will hate it.

- We are interested in the feedback from the seminar on making all catchup roth and if that is legally allowed.

- We were already looking at adding a Roth option to our plan.

- We will need to add a Roth provision to the 457 Plan offered to Public School employees.