Advertisement

QOTW: Employer Contributions as Roth

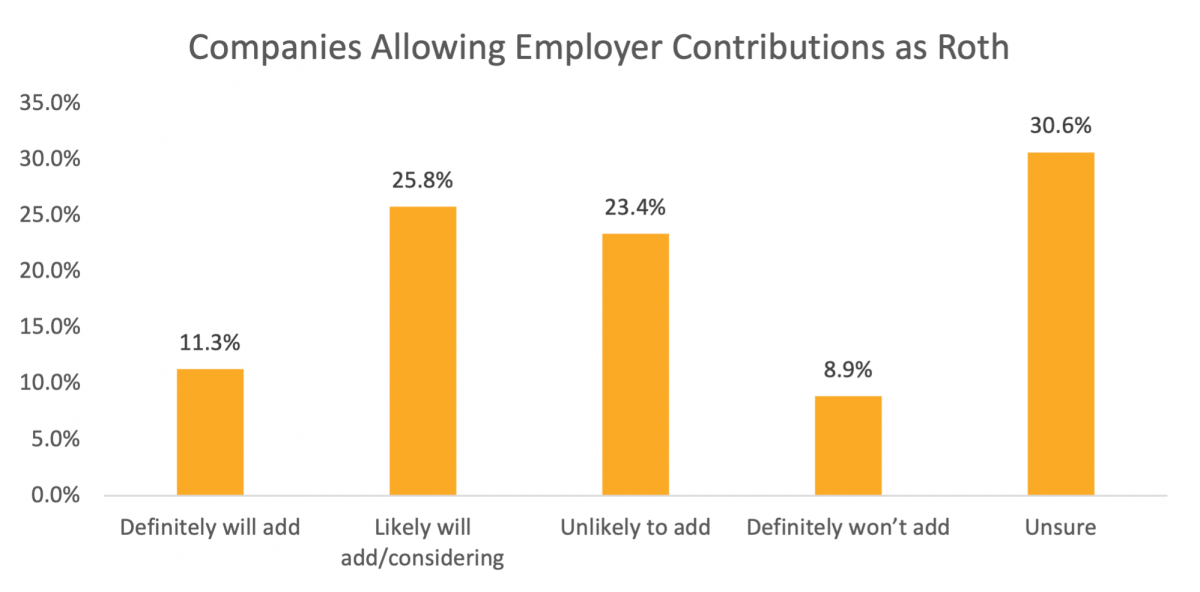

One of the optional provisions of SECURE 2.0 would allow participants to elect employer contributions as Roth after-tax contributions (rather than only employee contributions if the plan currently offers Roth). Some PSCA members are considering this – have had participants request this provision – and wanted to know if other sponsors are likely to adopt this provision. Though 30 percent of respondents indicated they are unsure, the remaining responses are fairly evenly split on adding this provision or not – 37 percent are definitely adding or likely to add this provision, while 32 percent are definitely not or not likely to add it. Many sponsors, on both sides, are concerned about the administrative complexity and waiting to see how it will be handled through payroll and the recordkeeper. See comments, by response type, below.

Definitely will/Likely to add

- Already added for 2023

- Not sure how fast we will implement, trying to coordinate with the other changes while not overwhelming administrators or employees..

- We already currently offer Roth

- We already have this option in our 401K

- We already offer Roth

- We already offer Roth in addition to the 401K

- We already offer Roth in our plan

- Already offer Roth so don't know why we wouldn't let employee's determine if they want match pre or post tax.

- I think it is a really great option for some employees.

- I think it will be a worthwhile addition to our plan. My understanding is that Roth company contributions will be taxable to employee, so will need to see how to handle it in our payroll system.

- I think this is a great idea, but we would have to amend our plan to allow Roth contributions.

- If this is something that can easily be automated by the payroll system then I see no downside.

- Less impactful for our plan as we have in-plan Roth conversion which allows match and profit sharing dollars to be converted to Roth at any time. May add so that it is immediate.

- Seems like this is a win-win proposition for employer and employee. We will review it with our advisor and determine if there is any downside, but if not we will adopt.

- The main factor will be time/expense to update Workday.

- Undecided. But probably will if the recordkeeper can support without raising costs.

- We have had employees asking for this and we will likely add however there are a number of complexities and build to consider.

- We haven't heard anything from the team that supports our payroll system regarding any of the SECURE Act 2.0 provisions. I know that many of their clients are asking for guidance. It seems that it will be hard to implement some of the provisions.

Definitely will not/Unlikely to add

- Don't want the added admin burden of running the match through payroll to tax it.

- No desire to add another layer of complexity at this point.

- Our current payroll system is unable to facilitate employer Roth contributions.

- This option would add another level of complexity to our payroll processing that we will not be interested in taking on.

- adds too much complexity, especially with having to withhold taxes on the contribution amounts.

- As written, will be very difficult to implement - coordination with payroll and 401k recordkeepers will be complicated.

- At least not right away. Need to understand how it will impact the plan, administration, participants, etc.

- Participants can already do this by utilizing the In Plan Roth Rollover feature

- The immediate and future tax consequences for both participant and employee need to be fully evaluated before implementing such a provision.

- This is a significant added cost to companies

- Unlikely to add initially. Impacts on Company finances, recordkeeping ease, recordkeeping complexity and Participant understanding/communications must be evaluated.

- We are just now looking into adding Roth as an option. Unlikely to offer this provision even if we implement Roth.

- We do not currently offer Roth investment option.

- We have a vesting schedule that we wish to maintain. It's too difficult to explain the tax hit. We already allow in plan Roth conversion so people can do this themselves. And, if we did it, it would end up costing us several million dollars each year in lost forfeitures from terminations prior to vesting.

- We likely won't add the option directly given the vesting/tax issues that come into play but indirectly we have a Roth In-Plan conversion feature so participants can move their match source monies to Roth via that mechanism and accomplish the same thing. We currently match once annually so if we moved to a per pay period match, we'd like review further given the by pay period task it would create to do a Roth In-Plan conversion.

- We offer a Roth option to participants & if they want funds to go there, they can direct their funds to the Roth. Company contributions will remain going in their 401k account.

- We will add the ROTH option for employee and catch up contributions, but not for company contributions.

Unsure

- Administrative management concerns

- How do the taxes get paid? Is the employer responsible or the employee?

- Interested but need to know the logistics first. So far there are no guidelines.

- Looking for more information on why we would do this.

- My company would want to consider the pros and cons before making a decision.

- Very few employees have ever asked about this option

- We have to do this for those who are highly-comped. We will consider pros/cons about applying it more broadly.

- We need to fully understand the implications to the Company and our employees before considering adopting this provision.

- We will evaluate this option with Fidelity and then present it to our Pension Committee for discussion and decision. Unknown at this time which direction we'll go.

- Will discuss and see what changes that makes to the employer and corporate taxes, if any