Advertisement

QOTW: Financial Stress and Wellness Tools

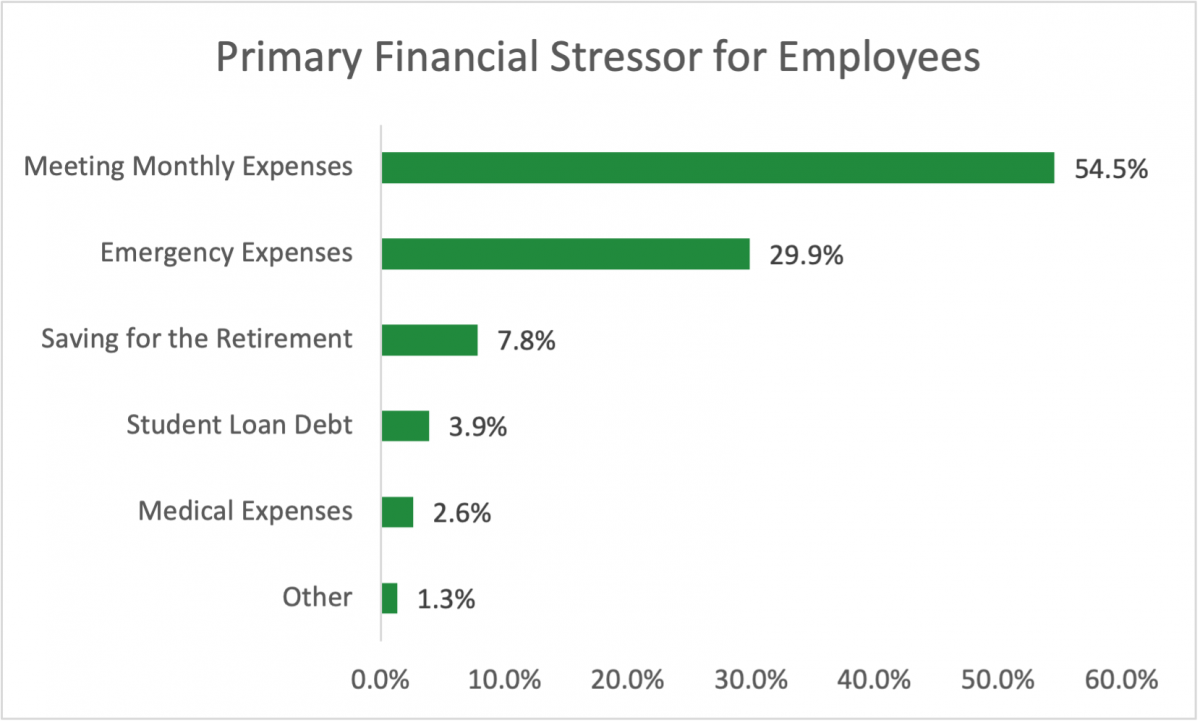

This week we asked plan sponsors what they think the number one financial stressor for their employees is, and what they think it the most beneficial financial wellness tool in addressing the stressors. More than half of plan sponsors said that meeting monthly expenses and budgeting is the primary stressor, and thirty percent said the primary challenge is emergency/unforeseen expenses.

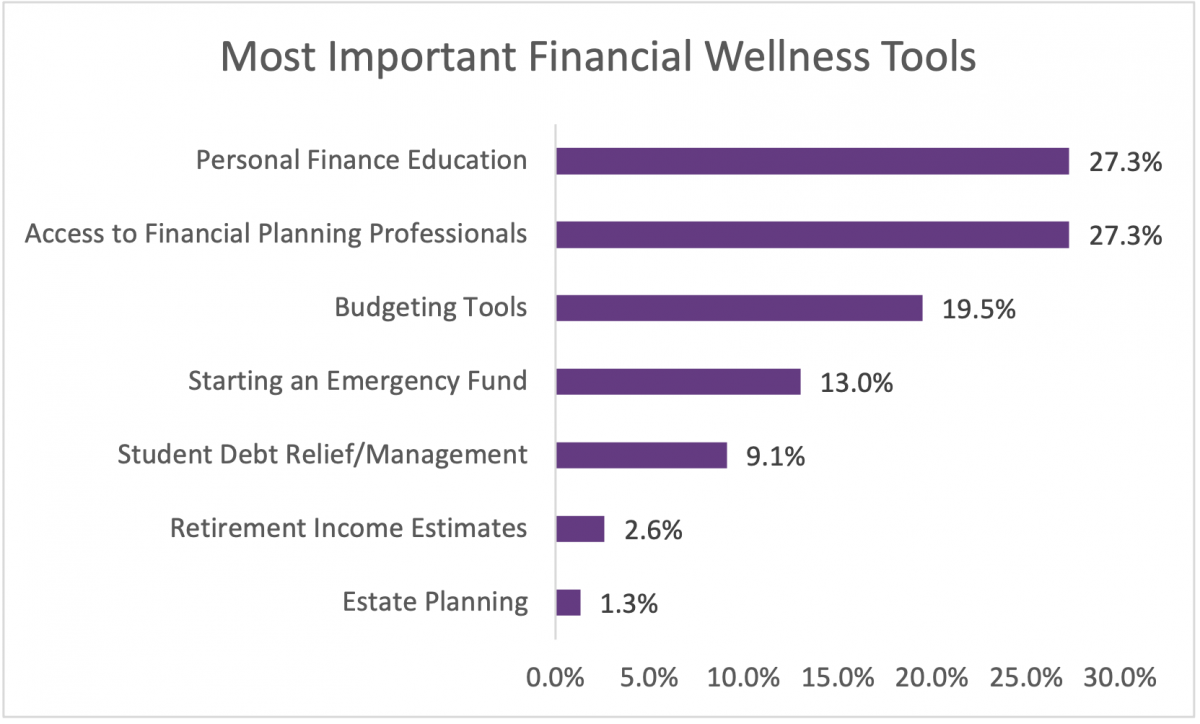

Personal finance education and access to a financial planning professional are tied for the most beneficial part of a financial wellness program. Budgeting tools was also cited by 20 percent of plan sponsors.

Maybe respondents indicated that picking just one item was tough as many of these are intertwined, and depends on the life stage their employees are in. Read the comments below:

- Although all the elements above are important, starting an emergency fund was selected because it is a catalyst/springboard for the other elements.

- EEs no matter the generation really respond to a personal meeting like no other. Tools are still impersonal.

- I think financial literacy is on issue whether in our higher or lower paid employees. Being able to provide this additional guidance is something we are continuing to pursue.

- I think most people live outside their means and if they just budgeted and stuck to a lifestyle they can afford, they'd be able to handle the rest (paying off debt, handling financial emergencies, saving for the future, etc.)

- I think the best financial wellness programs are those that help them manage spending. If they do a better job of living within their means now, they can better save for emergencies and retirement.

- It is hard to just choose one from both questions, I feel that there are several answers that have the same weight when it comes to financial stress and ways to address it.

- It takes a certain level of determination (and includes both spouses) to address overspending. Most people will not take the painful steps necessary to rectify their financial situation. Their short term financial well being is always a priority over their long term financial well being.

- It takes a lot of effort to truly live within your means and save for unforeseen expenses and retirement. Sometimes advisors can be out of touch with rank and file families. We need to step back and think more about how to change behavior without just lecturing.

- It was very hard to pick the #1 stress when you have a wide range of employee demographics. I chose the #1 stress based on a group we are targeting this year in our warehouses. They have the lowest participation rate.

- Make a budgeting class required the same way compliance training is required

- Many ethnicities are not taught about how money works and how to manage money so even when they are making good money they don't know what to do with it to manage current expenses and save for the future.

- The firm has HCE and NHCE and for the NHCE, I don't think they think it is important to allocate money through their budgets to fund for retirement on their own behalf, they think the PS contribution will suffice, which is 10%. We use the 1% get started push just for participants to get started.

- The foundation to do all of the items above is to budget.

- We have such a wide range of employee ages, there are really different needs based on their stage of life.

- While student loan debt is important, it is only one piece of a total personal loan debt stressor that impacts all employees, not just those who have attended college. Debt management programs should address not only student debt, but other credit debt as well.