Advertisement

QOTW: Gen Z Savers

Last week a new report from BlackRock showed that Gen Z savers are saving at higher rates than other generations – at an average of 14% of pay (though the report doesn’t specify if that is deferrals only or includes employer contributions).

This seems high, but the notion that younger workers are saving at higher rates than other generations is interesting. Saving in a workplace retirement plan is commonplace and it is likely that many Gen Zers have grown up with parents saving in plans – the 401(k) is not new and pensions are likely not on their radar. So, are plan sponsors seeing higher savings rates by Gen Z?

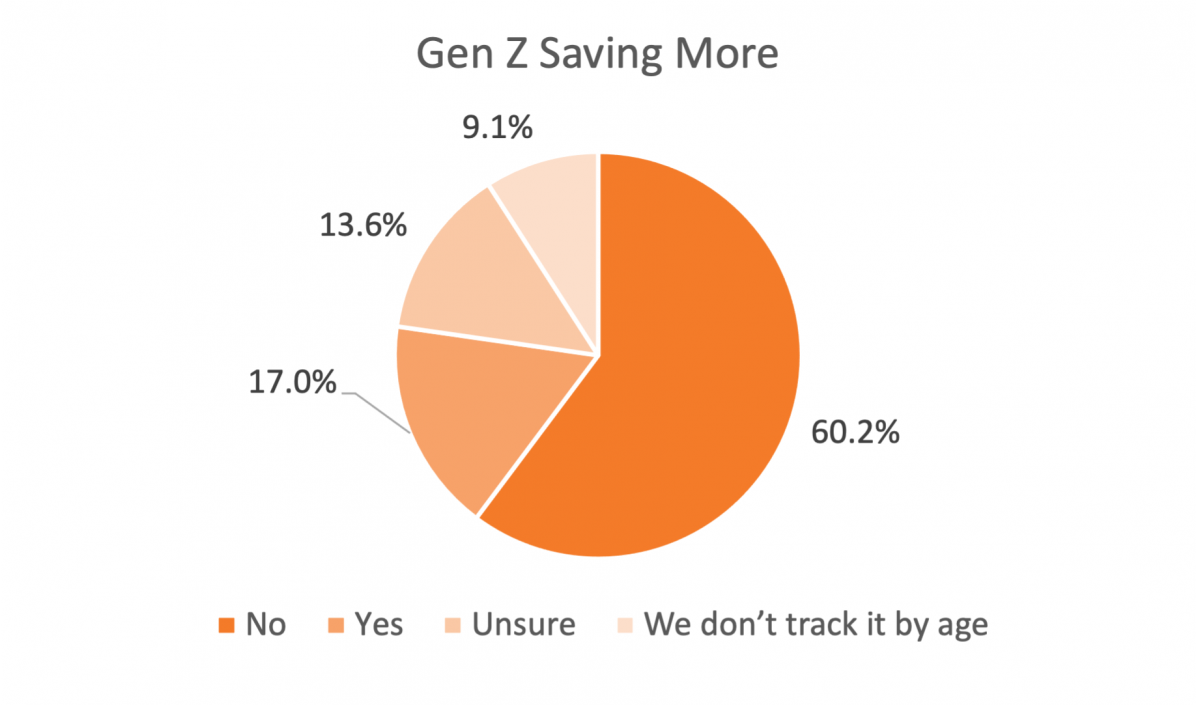

Sixty percent of respondents to our QOTW said no, they are not seeing higher savings rates among Gen Z, with only 17 percent saying they are and the rest unsure or not tracking savings rates by age.

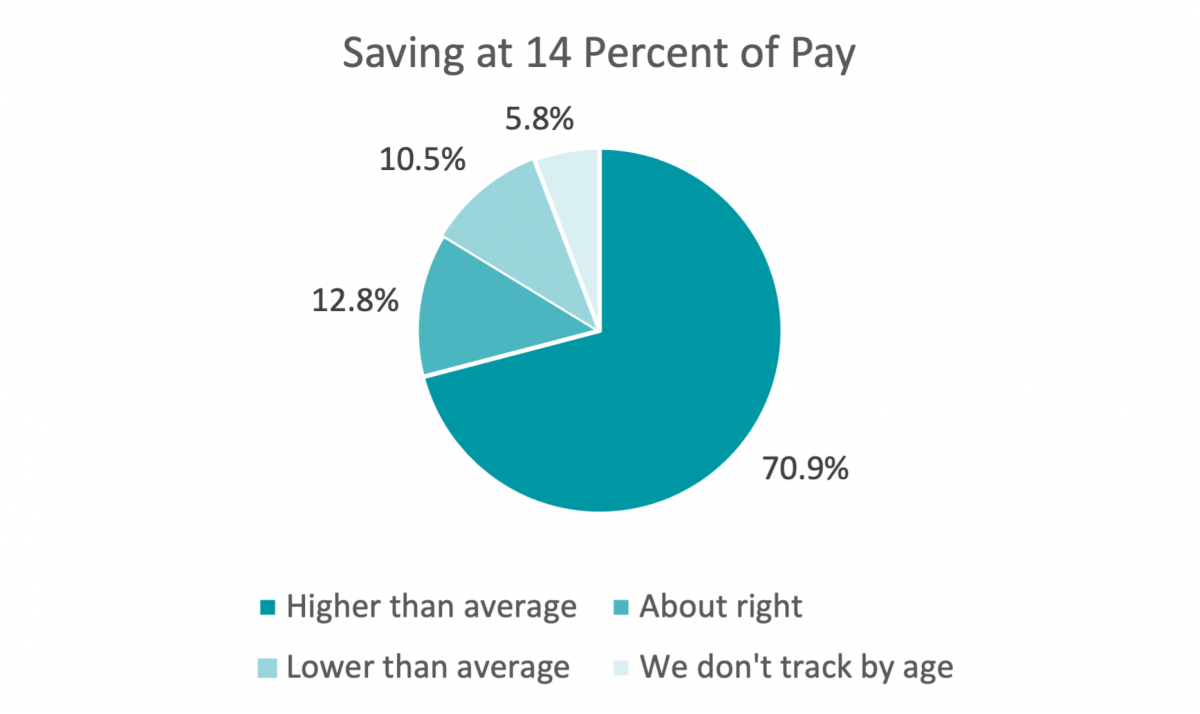

And what about a 14% savings rate – does that sound about right or too high? Seventy percent said that’s higher than average for their employees, though 13 percent said that’s about right and 10 percent said a 14% savings rates is a bit low.

We didn’t capture the industry of respondent companies to this poll, but as a respondent to a similar poll of advisors on NAPA.net said, “It depends on the industry. If in professional groups or traditional "white collar" organizations, the answer is many save a higher percentage but … in manufacturing or other "blue collar" organizations and not for profits, the answer is no even if looking only at those who are participating.”

Some plan sponsors noted that younger employees, when they participate, tend to max out the match. So those plans with a “stretch” match or a higher match rate are seeing higher savings rates among younger workers (when they save). They also comment that when Gen Z participate, they often select auto increases so over time those savings rates are bolstered. It is worth noting that the BlackRock survey did not state that the participation rate among Gen Z is higher than other generations, but that *when* they participate, they are savings at higher rates. And that could likely be due to the plan design features used to boost savings rates such as matching formulas and auto escalation features.

Other plan sponsor comments follow.

- Average approx. 6-8 percent

- As many younger workers are still living with their parents, we have seen their deferral amounts increase.

- For our population, average deferral rates increase as an employee get older.

- Gen Z only makes up about 10% of our workforce and are averaging 8.0% savings rate. Millennials are at about 8.3%, Gen X is about 10.9% and Boomers are 17.4%

- Great to see!! Wish other generations would also up their savings.

- I find that younger workers are more inclined to sign up for deferrals, but the average deferral is around 5%.

- I would be interested to see whether younger workers are less likely to have other sources of retirement income. For example, some employers have closed their pension plans to new entrants, which would naturally mean that over time their younger employees would be more likely to be saving more in a 401k.

- In our company it is the Boomers that are saving the highest amount.

- It appears the older generations are saving at a higher rate. We recently started auto enrollment and auto escalations, which has helped participation tremendously!

- It has been difficult to get our Gen Z to understand the importance of saving. They don't have faith in the marketplace and prefer to place into their HSA account. However we have low participation in both by Gen Zers

- It's more of a buildup. They start low, but elect a step-up plan that takes them up year by year.

- Many do not exceed our max match at 7%.

- Many of our workers (construction) seem to live paycheck to paycheck even w/ recent across the board pay adjustments. They're not able to save.

- Must be 20 years of age to participate in our retirement.

- No, we find that those over the age of 55 save most. Of the 88% of Gen Z who actually contribute to the plan, they are saving on average 6% of their pay toward retirement.

- On average, our older workers (35+) have a higher savings rate ~11% vs. younger workers at ~6%.

- Our company matches $.30 for every dollar an employee contributes up to 15% of their pay. As a whole our employees average contributions over 10%. Our Gen Z employees are consistently +10% in their savings rates.

- Our match maxes if employees do 12% so many tie it to the match.

- Our organization's plan between employer contribution, match and employee deferral equates to 14%. 98% of our participants are at that rate or above.

- Our plan shows those age 29 and younger are contributing 6.5% average. Those 30-39 are also contributing 6.5% average. We are retail, so this may be a reason why Gen Z isn't contributing as high as a percentage in our organization.

- Our young workers are saving 7% on average

- Our younger employees definitely do not save at a higher rate than our older employees, and it is like pulling teeth to get them to participate in the 401k plan at all.

- Our youngest workers are at 6%, with maxes out our match.

- Overall, our organization has seen an increase in deferrals for all age groups over the past few years.

- Some of the younger workers who still live at home with parents elect a higher savings rate than those that don't. However, the highest savings rates currently are with those 60+ who are nearing retirement.

- Student loans are a larger part of younger population's budgeting balance with retirement.

- They are saving more.

- We have a small number of employees below age 25. Of those aged 18-25, the average deferral rate is 9%

- We haven't specifically looked at the age group but I'm going to check it out!

- We see our employees deferring a higher percentage the older they get.

- We see the younger folks saving at least up to the match and participating in the auto increase. In the past, younger employees tended to not save at all.

- Younger workers are saving less than 8% on average.