Advertisement

QOTW: Recordkeeping Fee Allocation to Participants

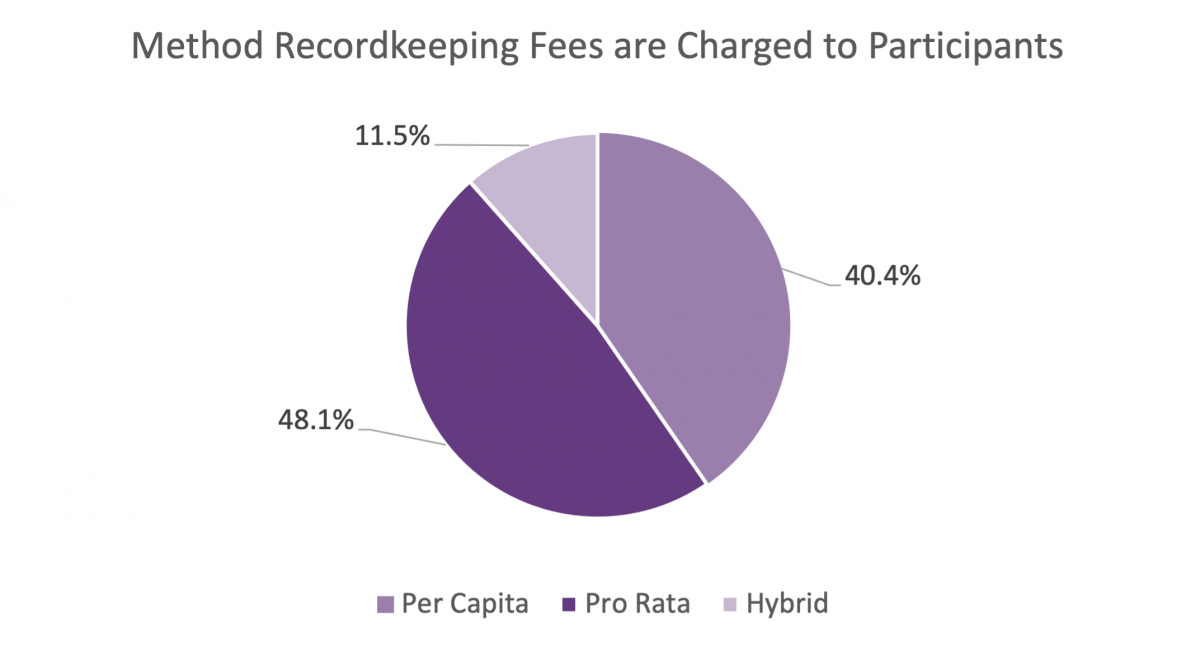

A member is reevaluating how recordkeeping fees are charged to participants and wanted to know what other members do and why. Thirty percent of respondents stated that they do not pass on the recordkeeping fees to participants. Of those that do pass on recordkeeping fees to participants, nearly half use a pro rata approach, allocating fees based on account asset size, while forty percent allocate a fixed fee to each participant, regardless of plan balance.

As is true for the fees charged to plans by recordkeepers, the fee assessment method is size corelated with small plans MUCH more likely (70%) to use a pro rata calculation and large plans more likely to use a per capital (55%) or hybrid (18%) approach.

Interestingly, the most common reason in the comments for why the chosen method was used, for both methods, is that it is the fairest method for their participants. Which begs the question, who decides what’s fair and why? Is fair equitable? Or is fair giving everyone what they need, even if it isn’t the same? (I may or may not have had this conversation with my children at breakfast this morning when discussing the “fairness” of screen time allocation.) The determination of what is “fair” is very much a value judgement and will depend on the decider’s point of view. And what feels fair to the person on the receiving end of those decisions is not necessarily what seems “fair” to the decider (just ask my kids, or any kids for that matter). For this decision, there isn’t a right or wrong answer, and keeping your employee demographics – and corporate culture – in mind will help inform this choice, and ensure it is rational and prudent.

Read the rational for the methods used below.

Does not pass on RK fees:

- Company pays for all RK expenses outside of plan assets.

- Employees pay their own investment fees however we pay the recordkeeping fees.

- Recordkeeping fees are paid by the plan sponsor.

- Recordkeeping fees are paid via revenue sharing

- Trying to keep the costs to EEs as low as possible.

- We are a small plan and pay the asset based fees as a cost of doing business and a benefit to help our employees save for retirement.

- We look at this as an administrative expense of providing an employee benefit, no different than costs associated with administrating other benefits such as medical coverage.

- We use RCA (RCP) funds to cover recordkeeping fees.

- While employed they don't pay record keeping fees, once they terminate, they take on all fees.

Charges Per Capita:

- As a small plan we have extremely low fees to begin with, so we decided it was fair to pass some fees along.

- Fees are withheld from the participant's plan assets on a quarterly basis. The company pays the fee for the first 3 years of service for participants to allow them to build savings.

- Forfeitures used first for active participants. Terminated participants (except retirees) pay their share in full. All participants receive the same services, so all are charged equally.

- I do not have the institutional knowledge required to address this question. Maybe the recordkeeper provided a choice to us or maybe the only option provided was per capita.

- More transparent to participants. Each participant pays an equal amount of the recordkeeping fee.

- Our committee's preference is to maintain an equal share of the cost to participants. In order to not discourage new savers, we exclude anyone who has been saving for less than a year to allow time to accumulate assets.

- The fee is primarily the result of the administrative burden of tracking the account rather than the size of the account which is charged as the investment fee.

- We changed from pro-rata to per capita years ago because the same recordkeeping services are being provided to members regardless of the size of your account balance.

- We feel it is the most equitable.

- We have 25,000 participants and a flat fee is fair.

- We have negotiated more favorable share classes annually, driving down the expense ratios over many years. In the past, some large funds had achieved expense ratios with zero recordkeeping (RK) component. While that was successful from an investment management standpoint, it created a disparity among participants for the payment of RK fees. The only way to both achieve the lowest expense ratios and to achieve an equitable division of RK fees was to adopt a per capita structure. We implemented this at the same time that we moved all funds to share classes with zero RK component.

- We have over 50k participants - covering the RK fees would be cost prohibitive. We've negotiated very low RK fees and pass those on to participants. We do not believe that Pro Rata method is equitable or fair for participants and can severely impact rate of return for larger balances.

- We recently changed this to per capita from pro rata. This allows level, fair fees for all participants and prevents low-balance accounts from becoming missing participants.

- We used to use pro rata and found high balance participants were leaving the plan at retirement due to cost, which hurt out negotiating power. Changed in 2014 and seen a significant growth in assets.

Pro Rata:

- Allocation is based on level of participation.

- It is based on asset size for each participant.

- Just the way that it has always been.

- Our recordkeeper fee is charged as a percent of plan assets, so charging it to participants based on their share of the plan assets is equitable.

- Plan expenses for the general administration and recordkeeping of the plan can be charged to your account and the accounts of all other plan participants. The expenses that can be paid from your account have to meet certain requirements and must be paid from all accounts in a fair manner. Your share of these plan expenses is paid by a portion of the investment management fees and other expenses that apply to each specific investment in your account.

- Pro rata is more equitable to plan participants with small balances.

- Thought this was the fairest way to share the cost.

- We believe it to be the fairest means for allocating.

- We believe this is a fair approach to the fee allocation. It's similar to how success based fees would be assessed on a personal account.

- We currently pass the charge on to participants on a pro rata basis but are strongly considering a change to per capita for transparency and to ensure equality.

- We feel that Pro Rata is the fairest method to apply fees to our participants.

- We feel those with a small balance should not pay a disproportionate amount of the fee.

- We find it is more fair using a pro rata approach.

- We negotiate a per head fee with our RK, but pass along to participants pro rata. We have a significant population of low income employees with small balances.

Other (Hybrid approach):

- Participants will pay a small per capita fee and the rest is allocated on a pro rata basis. we don't want to encourage large accounts to leave the plan, but don't want new participants to pay a large fee as a percentage of their account.

- The rationale is that there is a fixed cost of providing recordkeeping services (flat fee) and then the remainder is tied to % of assets.

- The structure is straight fee per person from revenue sharing and excess revenue is returned back to participants based upon % of assets.

- This is a governmental plan, and it needs to be self-sustaining.

- We eliminated all asset based admin fees a long while back and replaced with a flat fee per participant for active and terminated with a balance of $5,000 or more. We didn't want to allocate to small balances so that a fee isn't a barrier to saving in the plan.

- We have a hybrid of a flat rate plus asset based with a cap; we are currently looking at changing back to flat rate.