Advertisement

QOTW: Retaining Participants

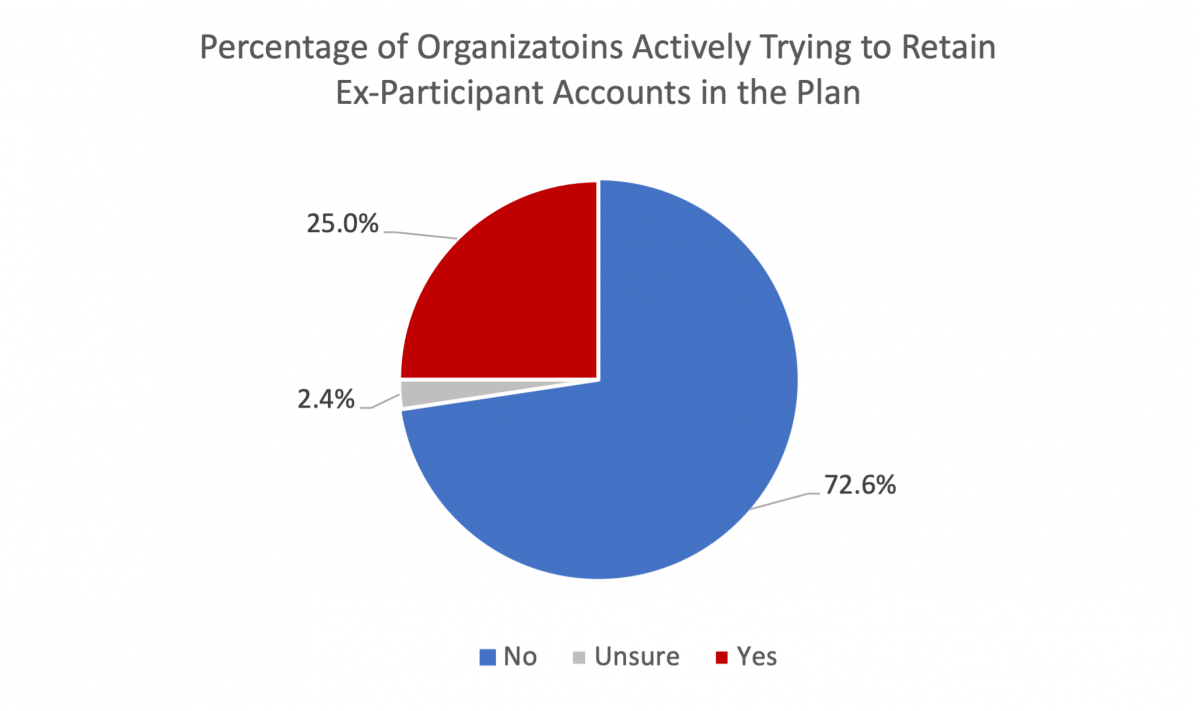

This week we asked plan sponsors if their organization actively makes an effort to keep ex-participant accounts in the plan. Three-fourths of respondents do not – though most say they allow it and provide education on the options, they do not actively try to retain assets in the plan. Many of these plans cited the increased administrative burden and the growing issue of missing participants and uncashed checks as a reason not to, though the majority seem to not take a stance either way. Most plans do have a minimum balance for remaining in the plan (77.8 percent according to PSCA’s 63rd Annual Survey), for some that is $1,000 (20.6 percent), for others that is $5,000 (57.2 percent).

week we asked plan sponsors if their organization actively makes an effort to keep ex-participant accounts in the plan. Three-fourths of respondents do not – though most say they allow it and provide education on the options, they do not actively try to retain assets in the plan. Many of these plans cited the increased administrative burden and the growing issue of missing participants and uncashed checks as a reason not to, though the majority seem to not take a stance either way. Most plans do have a minimum balance for remaining in the plan (77.8 percent according to PSCA’s 63rd Annual Survey), for some that is $1,000 (20.6 percent), for others that is $5,000 (57.2 percent).

For the quarter of plans that do actively try to retain participant accounts, nearly all target both retirees and terminated employees. Most also citied keeping assets in the plan helps them provide better options and lower costs to all participants, and that their options and costs are better for retirees in the long run, so they see it as an additional way of supporting retired employees.

Comments from both sides follow.

Plans that do not actively encourage ex-participants to stay in the plan:

- I don't think terminated/retired employees are communicated to enough about this, and I don't think they understand their options fully.

- If under a threshold we auto-distribute.

- Increases administration and incurs plan admin fees for account maintenance.

- It's not that we make effort to keep them in the plan but we let them know we will not force them out generally and that if they like the fund array, they are free to keep their funds in the plan until such time that they wish to rollover.

- Most of our terminated participants are young.

- Our Executive team would prefer we get them out of the Plans.

- Our terminated/retired employees have not been high maintenance so there is no incentive to move them out. Their accounts represent greater than 10% of total plan assets. As we have more employees retire with large balances we expect the aforementioned percentage to grow as younger employees have lower average balances.

- Standard =<$5000 distribution. Higher balances may remain.

- There is a concern if too many long term participants with high account balances leave at the same time (retire) and how that would impact the total plan balance.

- They have that choice but there is not a targeted effort to retain the ex-participant.

- We allow it, but do not make any efforts to keep them.

- We allow that to be their personal choice.

- We allow them to keep it in the plan up to a certain age but do not encourage them to do so.

- We are neutral on the matter. There are no actions to encourage or deter the former participant's decision to keep assets in the plan.

- We currently only force out balances under $1,000 but we also only offer lump sums to ex-employees with no periodic payment options.

- We discourage it because of the difficulty keeping track of addresses and sending out notices.

- We do not actively make an effort, but most former employees keep balances with the plan.

- We do not have concerted efforts to keep terminated employees accounts in the plan, but we also do not encourage terminated employees to move their accounts, but we do remind them of the minimum amount and that their account may be forced out of our plan if their balance falls below that amount.

- We don't conscientiously make an effort, but we don't require terms/retirees to move their funds.

- We don't encourage or discourage terminated participants to keep their money in the plan from a communications standpoint. From a plan provisions standpoint, we do not charge additional fees to those who have terminated employment, and we also allow them to set up periodic installment withdrawal payments (monthly, quarterly, or annually). About 20% of our plan participants are terminated.

- We don't encourage them to leave the plan, but we also do not do anything proactive to keep them in the plan either.

- We don't make an effort to move the money out.

- We don't solicit ex-employees to keep their money with us. It is based on balance as far as options go.

- We explain the options available and let the individual decide.

- We force out anyone with a balance $5,000 or less. If their balance is greater than $5,000, they can keep their balance in our plan.

- We inform them that they can leave it in the Plan if they choose to.

- We make it easy for participants to stay in the plan. However, we do not make any extra efforts to retain employee account balances beyond that.

- We make no special effort, though we do allow it... I can see the benefits of leaving the funds however it seems to cause more headaches when something doesn't go smoothly - bad addresses, no beneficiary records, etc.

- We neither encourage or discourage terminated/retired employees from participation. We do have small balance limits to automatically force those accounts out after a certain period.

- We used to, but the plan's TPA rate structure does not benefit anymore by this, so there's not a reason to worry about it either way.

- We're becoming more concerned about missing participants than increasing the assets in the plan. We've made a big push over the last year to reach out to plan participants that termed more than 5 years ago to remind them that they still have an active account. That effort resulted in finding 3 that had passed away (one more than 5 years ago). We have also increased the frequency of auto cash outs. This is reducing uncashed checks as people tend to move over time otherwise.

- While keeping ex-participant accounts in the plan isn't a goal, educating participants on their options, and the fact they don't have to take a withdrawal when employment ends, is. That's a common myth.

Plans that do encourage ex-participants to stay in the plan:

- Our plan has the incentive of lower fees due to institutional pricing of funds.

- Retirees tend to have a plan in place that requires them to move the funds out of our plan.

- We are trying to help them to make good retirement decisions.

- We attempt to educate participants about plan pricing, which is favorable because of our negotiating power made possible by the billions of dollars in the plan.

- We believe that our low fees and quality investment options are a good choice for participants, and superior to almost all retail options.

- We don't go all out but we do encourage it without giving advice about it.

- We neither encourage or discourage this practice. We do have the force-out provision. We have a lot of former employees that retain their money in the plan we provide them information at time of separation options they have and also what to review such as fees, consolidation, etc. If someone leaves it is more likely they don't cash out fast (under age 59 1/2).

- We provide participants (former and active employees) with exceptional fees and investments. We allow ALL participants to rollover assets into the plan to make advice and distributions easier. We also permit former employees to take and/or repay loans, believing that repaying themselves or taking out a loan and repaying it allows them to keep their retirement assets (rather than just taking a permanent withdrawal). The more assets we have from ALL participants, the better our investment class share, services and fees.

- We set up our plan design with distribution options and low costs to make it desirable for these people to stay in the plan. Our separation of service notice has cash distribution listed last to get people thinking differently than just taking their money.