Advertisement

QOTW: Retirement Tier

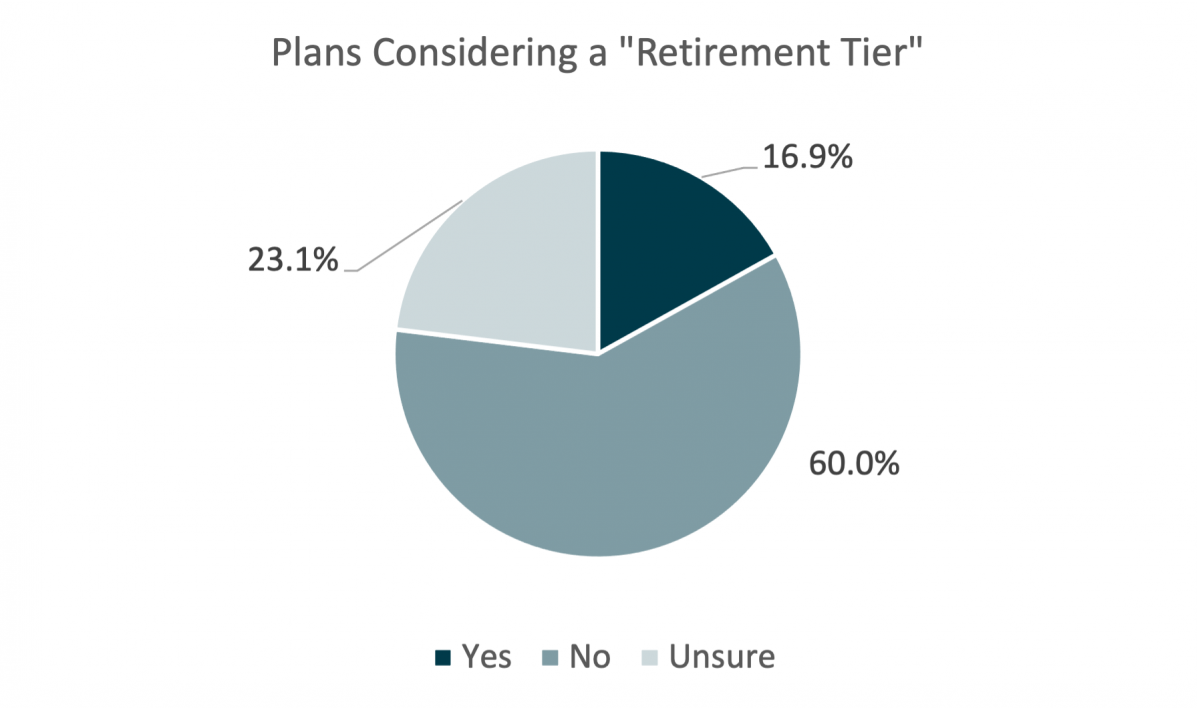

We’ve been hearing talk in the industry about the benefits of companies trying to keep assets in the plan, especially with the significant increase in assets expected to flow out of plans as the baby boomers retire. This might look like adding a “retirement tier” to encourage retirees to leave assets in the plan and draw them down over time. This week we asked sponsors if this is something they are thinking about at this time. Sixty percent of plans are not with another 23.1 percent unsure (many have not heard of this), with 16.9 percent of respondents actively thinking about this. Comments follow.

- Assuming you're talking about a 401k Plan, we don't have a need to keep money in the plan. It's working well as it is.

- Been doing this for 10 years

- Currently not considering, but interested to see results and comments on survey.

- Expanding resources to retirees would add significant administrative and fiduciary burdens to plans like ours (small to midsize).

- Great idea. No plans of doing such a thing.

- Hadn't considered it, but I would be interested to hear success stories from other plans that offer this.

- I would not say we are considering it, but we have had discussions.

- Many people with higher values seem to already have an advisor and a plan.

- Need to evaluate.

- Not at this time. It is something we have on a back burner.

- Our institutional share class pricing assures participants have low investment costs so we encourage participants to keep their money in the plan after termination/retirement. We already allow partial distributions and installments. We are starting to study what we can do better for decumulation.

- Our Plan currently offers a managed account option (which includes an annuity option). Our TDFs offer a "through" glidepath that has a slightly higher allocation to equities than peers or the benchmark. We continue to evaluate the addition of annuity products to the core lineup.

- Our plan currently provides for lump sum distributions, partial distributions and annuities. We may start looking at other options for decumulation through investment options which include this as a feature.

- Retirees are already allowed to remain in the plan after their last day, so long as their balance remains at or above the $5000 DeMinimus amount. The retirees are allowed to manage their accounts and investments in target date funds or a variety of available investments. They are also allowed to select annuity payments or lump sum payments.

- The retirement balances for our participants is small. Consolidation IRA would be more applicable at retirement.

- There are many logistical challenges (employee savings across multiple locations, employee education, lack of easy distribution solutions) - investments is not high on this list, and most plans already offer investments that could be considered part of a "retirement tier"

- This is already an option - many of our retirees keep their funds in our plan at retirement. As a 403b plan sponsor, we already offer two vendors, one of which offers annuities that our retirees can transfer their funds to if they want an annuity.

- Under discussion with financial advisor.

- We already allow participants to keep balances in the Plan after retirement. They also have option to receive installment payments from the Plan.

- We are adding managed accounts but won't require a retiree to keep assets in the plan. At present we do not have managed accounts, but allow those over the age of 59 1/2 to rollover assets to other qualified plans during employment as many of our lawyers and staff have other accounts and they would like to consolidate. We will see what happens when we begin offering the managed accounts in mid-October when we switch record-keepers and see how many participants take advantage of the managed account offering and then determine if our fund offerings will need to be modified.

- We currently do not make a significant effort to promote to retirees to keep their money in the plan.

- We do not encourage terminated/retired employees to remain in the plan. It is too hard to keep track of them as time passes.

- We have always actively tried to keep assets in the plan and have sought opportunities to help with distributions. We are now looking at better decumulation strategies. May be a while before we add, but we're heavily researching.

- We have talked about this type of feature but there are a number of reasons we have felt that it isn't a good fit for our plan and participants. 1)Currently all assets have to be out of our plan if terminated by age 72 so no ability to maintain through retirement. 2)We have a cash balance pension plan and very few (2%) of terminated participants take the annuity 3) a large portion of our employees work with a financial advisor who provides more individualized expertise on drawing down income in retirement 4) there is limited uptake in benchmarking and products at this point and we tend to wait and see before acting.

- We might consider at some point but currently not a part of our plan.

- While generally keeping more assets is good, there is administrative concern that this will increase issues with lost participants and complications from disbursements at death

- Would like to know the benefits of doing so. Our CFO tends to like to push people out of the plan once they terminate but I'm not convinced this is the correct thing to do for the Plan.

- Would think we'd follow our trustees' guide here.

0 Comments

Discussion Policy

Sign In to Comment