Advertisement

QOTW: Sidecar Accounts

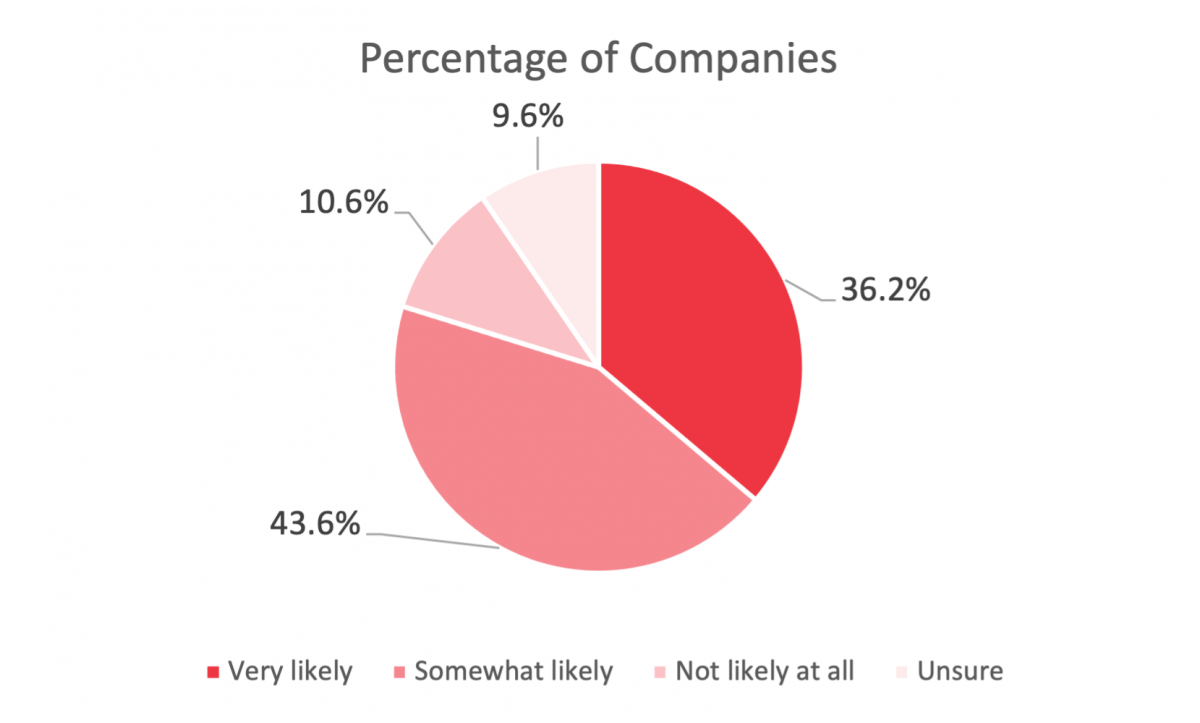

Legislation is currently being discussed in Congress that would establish emergency savings accounts that would be held alongside existing 401(k) accounts (a “side-car account’). Amounts contributed to the emergency savings side-car account could be withdrawn by the participant at any time with no penalties or restrictions. Under this legislation, employers choosing to offer these emergency savings side-car accounts would be required to match the emergency savings contributions following the same matching contribution formula that applies to traditional 401(k) contributions. This week we asked members it they think participants will be likely to switch some or all of their current traditional 401(k) plan contributions to emergency savings contributions since they can get the same matching contribution without any withdrawal restrictions on their contributions. More than a third said their participants were very likely to make the switch and 43.6% said participants are somewhat likely.

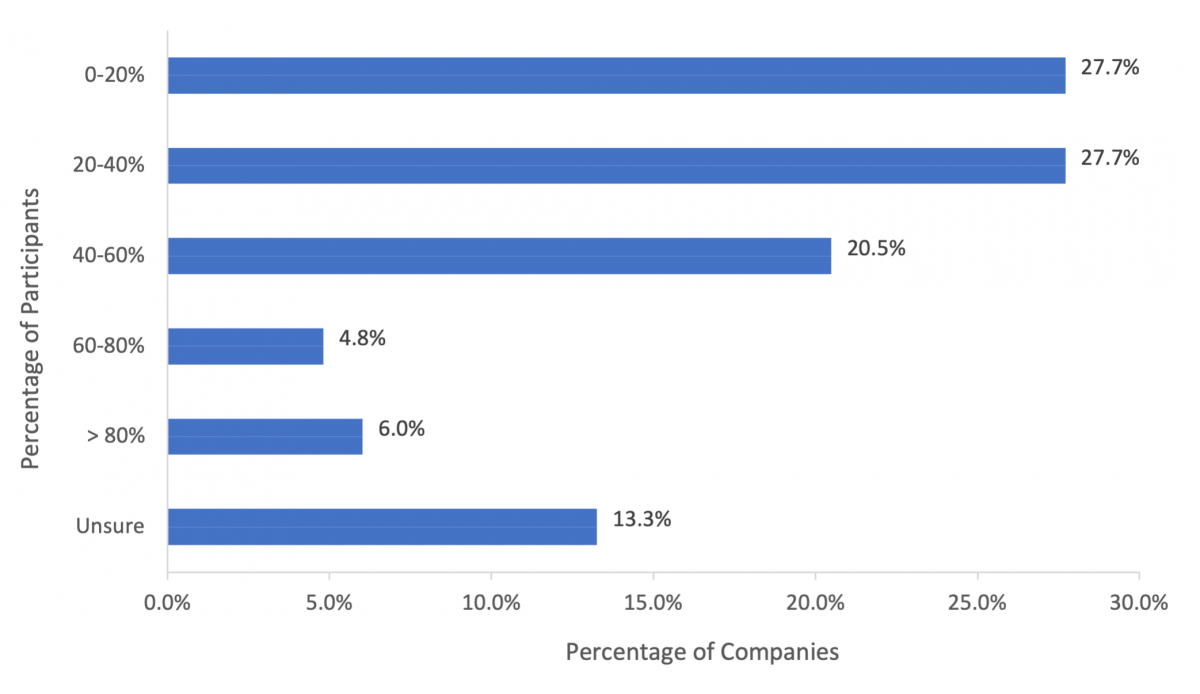

We also asked members what percentage of their participants they thought would make the switch if given the opportunity. Nearly 30 percent of respondents said they thought less than 20 percent of their participants would switch, and the same number think between 20 and 40 percent might switch. Very few respondents think that most or all participants would switch their retirement savings to emergency savings.

Other comments:

- A 401(k) account is a retirement account not a savings account. It’s doubtful my company would offer to participants as we already have participants treating their 401(k) like a savings account by taking out a new loan as soon as they are able. To reward them with an employer match (which would likely be higher than earnings on a traditional savings account) would discourage retirement savings even further.

- A lot of unknowns - Vesting? Maximum coordinated with 401(k)? Tax status of the sidecar plan contributions, etc.

- At some point employees have to start taking responsibilities for their own well being. A side-car account will likely result in more red-tape for the Plan Sponsor and be a stick rather than a carrot.

- Certain industries with a large population of low paid employees (retail, hospitality, health care, etc.) have many employees living paycheck to paycheck who frequently initiate plan loans, etc. This arrangement would be another vehicle for these employees to access their funds, and not save $$ for their retirement.

- Company will discuss this, but is highly unlikely to offer option.

- Don't understand the why behind this proposed legislation. Would the match have the same vesting scheduled? It might make employers stop the safe harbor contribution that has a shorter vesting schedule.

- Few would use this feature

- I agree with the concept but I dont know that I like it attached to the 401(k). Its hard now to convince people to save for their future needs when their immediate needs are barely being met. If this is an option I can see many employees not deferring to their 401(k) and putting into the side car funds because they will have the security of accessing these funds without penalty to meet their immediate needs. Immediate needs will always to take priority to future needs, and it gives the employees the temptation to access those funds even if they really would be ok to not access them. A cap on that emergency savings should be considered, or a cap on the match. If dollars are capped employees will still put into the 401(k). We already have a retirement crisis and this could make that situation worse.

- I believe the actions of participants will be different and the largest determinate will be compensation. Highly comps will do nothing. Lower compensated employee will initially do nothing based on inertia. But actions may spread like wild fire based on conversations with peers.

- I believe this will be very high since there is no penalty to withdraw and they can take so easily.

- I don't like the requirement to match. We would just end up reducing our match to the 401(k) to offset this added expense.

- I don't like this idea. If they want to 'save' money, they should just set up a separate 'savings' accounts. We, as an employer, offer 401K to help employees save for their retirement. We don't want to 'match' employees 'saving' for regular use. We want to 'match' for the future benefit of the employees.

- I think it is a good thing but I don't see that many employers will want to have to match the employee's contributions unless there is a tax savings for them. It may also limit how much the employer contributes.

- I think this is a provision that could see high adoption. It may undermine the long-term goals of saving for retirement, but perhaps if we continue to create savers in general, we end up with a better result. Hopefully the side-car account is limited as to what types of investments could be held in that account.

- I think this is the right thing to do, but am concerned about testing implications and we do not match after-tax traditional contributions - only pre-tax and Roth. If 'traditional 401(k) plan contributions' mean after-tax contributions that is a concern. I also do not want the match to go into the emergency savings vehicle - only into the retirement account.

- I would like to hear more about this. I work at a law firm and we have different benefits for different groups.

- I would prefer legislation lean toward an out of plan emergency savings option, rather than showing ESA balances along side 401(k) assets intended for long term savings. In plan options interrupt the set it and forget it purpose of automatic 401(k) enrollment. It would be great if legislation allowed employers to also auto-enroll participants in an out of plan ESA account and take a credit for add'l matching contributions to employee ESA deferrals.

- If participants receive a match on the side-car accounts, there's no reason not to use this savings vehicle instead of a regular savings account. This will encourage this type of savings, but participants will save less for retirement.

- If the savings accounts are post-tax this would probably impact the number of Roth participants. Also, would the investment choices align with the 401(k) or a rate based earning.

- Is it side-car or side-card? Also, I think younger workers (or workers for whom retirement age is far away) would take advantage of this offering more than older workers (workers nearing retirement) would.

- It depends on other factors as well, like can they take loans from these accounts, or just withdrawals? I think generally people DO want to be savers, but the restriction from removing funds from the account while employed saves people from themselves more often than not and forces them to find other avenues to fund short-term financial fallbacks.

- It would be a great tool if properly used.

- Many of our more recent hires, and some of our longer term participants, are already using a side-card approach by choosing after-tax contributions with auto-Roth conversion. Our match formula takes into account participants' before-tax, Roth, and after-tax contributions, so the match is already neutral regarding the type of participant contribution. And we have no ACP concerns that might otherwise cap the after-tax availability.

- Not sure that employer should pay match for a savings account.

- Our plan also includes an after-tax source, where employees could use as an emergency savings fund. this account has no withdrawal restrictions. It might be a better option for employees, especially if the company decides to offer a match to support additional savings.

- Our plan currently does not allow for in-service withdrawals and an emergency savings account would be a palatable compromise. My concern with how I read the proposed legislation is that we do a once a year profit sharing contribution. If the company contribution is taxable (since an employee can pull it out I'm assuming it would be similar to Roth contributions), how do taxes get paid on the company contributions that land in participant accounts if they have terminated?

- Overall, I think it's a good idea. However, the amount should be capped that go into the account.

- Should have option to have a vesting schedule for employer contributions.

- The likelihood of participants switching would depend on the tax treatment of withdrawals and the impact of any fees that might be associated with side-car accounts.

- They should restrict being able to move their retirement funds to this account - just make it a true, separate account - not interchangeable.

- Think it should have a cap like 25% of total amount or something so people can have that emergency fund but not make it so easy to totally deplete their retirement account without any penalty.

- This is pure speculation on my part. I'd like to hear from those plan sponsors who do currently offer a side emergency savings type plan. I think surveying those plan sponsors specifically would be more beneficial. The rest of us are just speculating and many times the data does not come out the way we expect.

- This is the first I've heard of this, but it seems like the employee would see no downside to transitioning to the side-car plan. As an employer, I'd be very concerned about their lack of commitment to keeping the money for retirement and therefore falling short of retirement goals.

- This would alleviate the need for 401K loans which would be huge.

- We allow them to "cash out" accrued PTO, up to 40 hours, once each year to use as Emergency Funds.

- We're a retirement system, not an employer. The system has 825 or so employers reporting into it.

- We're manufacturing and see many participants take hardship withdrawals. I feel a significant portion of the workforce would switch.

- Would ee contributions be pre-tax, there should be some limitations to mitigate "replacement" of the traditional 401k process

- Would the ER contribution be pre or post tax? I think that would make a difference. I don't our think EEs would compromise their Traditional or Roth 401k earnings for a taxable scenario.