Advertisement

QOTW: Student Loan Matching

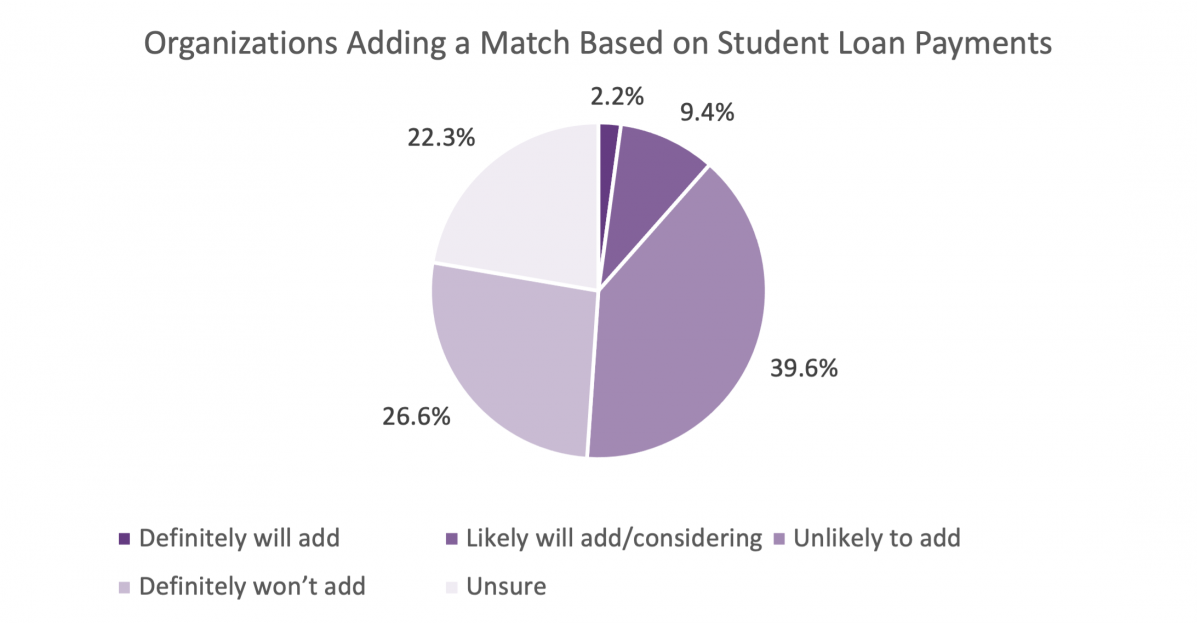

Starting January 1, 2024, employers will be able to make contributions to the 401(k) plan based on a participant’s student loan payments. This provision is optional so this week we asked companies if it is something they are likely to adopt. As we’ve seen before when this was just a possibility, some companies are very excited about being able to offer this as a motivator for recruitment while others are not likely to adopt it as it is not applicable to most of their workforce.

While more than 20 percent of organizations are unsure at this point, two-thirds are” definitely not” or “unlikely” to add this provision while 11.5 percent are definitely or likely to add it.

Definitely will or likely to add:

- We think this is a cool thing

- If we implement this provision, we will likely add it as an annual true-up calculation at the end of the year and do one annual matching contribution for student loans if they have not already met their match through deductions.

- It is critical the recordkeepers can support and it is minimal effort on plan sponsors/employers

Definitely won’t or unlikely to add:

- Adds complexity to manage.

- This would not benefit many of our employees. It would be costly to implement & track.

- We don't currently offer a match so the question doesn't really apply. If we do start offering a match, I think we'd initially only do it for 401(k) and not student loan payments.

- If our competitors add the feature, we'll be more likely to consider but at this point, we don't anticipate adding it.

- Offer a student loan repayment plan. Best of both worlds, pay off their student loan faster and if they contribute to 401k, get company match still.

- Our company is too small (50 pp) to add any additional match.

- Sounds administratively challenging tracking down proof of loan payments, how do you know when the loan is being deferred for any number of reasons? Or do you have the EE bring in the proof each month? Also, we have an older, manufacturing population that doesn't historically have a lot of loan debt (unless they have it for their children).

- Sounds difficult to confirm/verify/track and implement timely. Also some privacy concerns.

- We believe this would add an extra level of administration to monitor that would not be outweighed by the potential employees that would benefit.

- We do not have student loan payments setup in our plan, and are not likely to add that feature no change up the matching contributions to those student loan payments.

- We don't have an employee match yet, but would consider matching student loan payments if a match was implemented

- We have a non-elective safe harbor; participants don't need to contribute to receive ER contribution

- We have a plan where the company makes student loan contributions.

- We have low participation and interest in our plan. PLUS, most of our work force do not or have not attended a higher learning institution.

Unsure at this time:

- I hope my employer will strongly consider this option. I believe it will be a great benefit to our employee population.

- I like the idea, but not sure how we would implement it. We already do Safe Harbor matching. I don't know how we would send a payroll match on something we don't process through payroll.

- Want to see what others are doing

- We are concerned it will decrease current high savings rates and ultimately have a negative impact on retirement outcomes

- We have reviewed in the past and have elected not to pursue. Unsure if the changes will prompt a change in philosophy.

- We will evaluate this provision, but I am unsure whether we will add this provision to our plan.

- We would have to see what products are offered to track and monitor this.

- We're surveying our staff now to determine need.

- While it may be attractive for attracting talent, it seems like it would be administratively burdensome to manage.