Advertisement

QOTW: Student Loan Matching in 401(k) Plans

This week we asked plan sponsors if they would be interested in providing a matching contribution to their retirement plans for employees who are making student loan payments if there were no concerns about non-discrimination testing. This proposed provision in the SECURE Act 2.0 aims to help employees who are paying student loans and not able to contribute to their workplace retirement plan, and are therefore missing out on employer matching contributions. This provision would allow the employer to make the matching contribution to the retirement plan without the participant making deferrals. There are concerns about the impact this may have on non-discrimination testing and on current safe harbor plans.

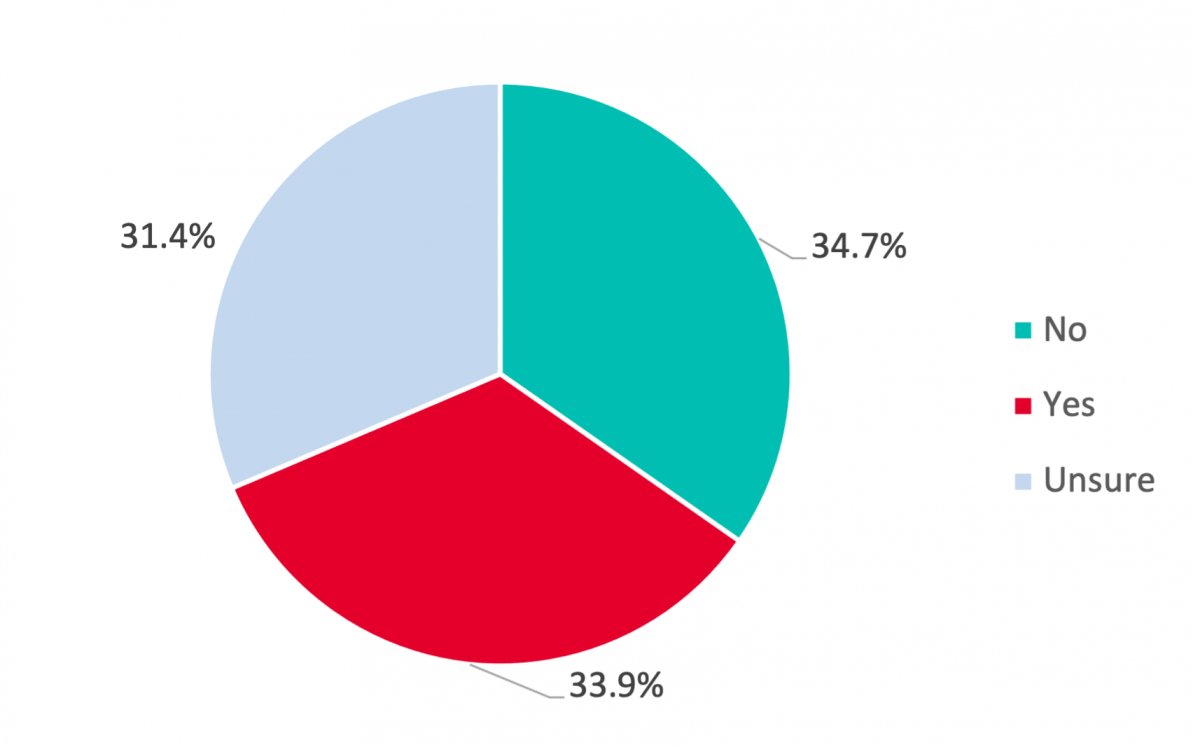

About a third of plan sponsors (34.7 percent) are not interested in this provision. The responses ranged from the position that retirement plans should remain focused on helping participants save for retirement and not used to solve the student loan debt problem, to companies who do not have many employees with student loans, to companies who are providing student loan assistance in other ways.

About a third of plan sponsors (34.7 percent) are not interested in this provision. The responses ranged from the position that retirement plans should remain focused on helping participants save for retirement and not used to solve the student loan debt problem, to companies who do not have many employees with student loans, to companies who are providing student loan assistance in other ways.

Another third (33.9 percent) of plan sponsors are interested in this provision and generally think that this would be a great way to attract employees and help address a growing issue.

About thirty percent (31.4 percent) of plan sponsors are unsure at this time – many stated that they are interested but have concerns about the impact on safe harbor plans, other regulatory concerns, and concerns about the administrative complexities.

Comments from those with no interest in this provision:

- The purpose of the 401(k) plan is for the participant to save for their retirement. If you start matching on money that goes to student loans, what other sources of debt should now be included as well.

- The administration of this is extremely complicated and would require more resources than currently available.

- We have an older workforce as well as mostly laborers that do not have personal student loans.

- At present, we don't have a large enough population requiring this benefit to make it cost/beneficial to administer. If that would change in the future, we would reconsider.

- Our employees are largely Hispanic. Due to cultural and economic variables, most of our work force is blue collared and haven't gone to college to accumulate student loans. Many of their children go to Junior Colleges and then on the state colleges where tuition is not like Ivy League tuitions. Many of their children work incredibly hard to garner either a scholastic or academic scholarship or athletic scholarship. Owing money to the government is not viable alternative.

- We have a tuition reimbursement program in place.

- Our plan is Safe Harbor - We do NO other match.

- Focus should be on finding ways to lower college costs, not continue the student debt growth and issues.

- We should not be placing any moral hazards into 401(k) Plans or DC Plans. The Plan loans are bad enough already.

- Not likely due to our plan being pretty generous to begin with.

- Not on the priority off issues we are dealing with.

- We don't use a match formula in the 401(k); we do a once a year discretionary company contribution. We also have a tuition reimbursement program in place.

- Our executive team is not interested in offering student loan assistance.

- Our plan is a voluntary 401(k) plan that's supplemental to a mandatory defined benefit plan. It's also a multi-employer plan, with more than 800 employers participating. An employee matching arrangement would be at individual employer's discretion. The plan document would also have to be amended to allow for this. So far, no employers have expressed interest in this feature.

Comments from those who are interested:

- We are interested but there has to be a cost benefit to the organization to help with student loan repayments.

- We would be willing to match up to 6% of annual salary toward qualifying student loan repayments.

- Exploring now.

- Would add to the growing issue of student debt and aid in attraction / retention efforts.

- We would like to explore this option. We are concerned about the appearance of only benefiting employees that have remaining debt, vs. those that found a way to pay for it already.

- We would be very interested in offering the match on student loan repayments.

- We already pay $300 per month to help employees pay off student loans. We need to stop simply forgiving them and encourage creative ways to incentivize their repayment without sticking our debt to future generations!

- This could be a significant way to attract talent and reduce a nationwide issue.

- We employ many highly educated employees where the student loan matching program would be a great benefit. As a small employer of less than 50 employees, programs with excessive administration or start up effort aren't feasible.

- Good for recruiting but hard to implement

- We would have to look at this carefully because putting money in a 401k earns tax deferred. While student loan matching would decrease a debt it would be of less value than increasing the match to the 401k. However you are helping the person in the present verses future.

- Definitely make this more interesting and it bridges the concerns of payments vs 401k deferrals.

- much needed

- Safe Harbor plan restrictions need to be addressed.

- We would be interested in redirecting company match to 401k deferral to loan payment, not a new matching contribution for payment made by employee.

Comments from sponsors who are unsure at this time:

- This is one we'd want more detail of administering and probably watch others do it for a while before considering seriously.

- Since we are a government entity, legislation would need to be passed related to making student loan repayments.

- Not considering now. Would need to know more about the recordkeeping implementation of such a program and related regulatory rules.

- Not really sure what this means or what it would look like.

- We are a church denomination that functions like a MEP. Decisions like the one above is handled on church level and not by the denomination. Anecdotally, I know some churches would like to offer matching contributions based on college or seminary loan repayments. If this becomes a possibility for 403(b)s, we will test the waters.....

- Our firm does not offer and is not interested in offering student loan assistance. I think they would see this as a way of offering that assistance and would prefer to keep retirement plan matching separate.

- I am in favor of matching up to the equivalent of a DC contribution max for student loans, however, I am only in charge of investments and this is a HR benefits plan design matter.

- Possibly! We are currently designing a student loan assistance program, and some employees are interested in a match/401k component...

- Our plan is traditional safeharbor so although it sounds great, it would not work for our plan.

- While there is a benefit to saving for retirement, the amount an employer would contribute would be miniscule and not be beneficial to employees. You would have to adjust fee schedules, investment offerings, etc. to make this beneficial to the employee and employer.

- I would be interested. I’m not sure how our committee feels about it.

- This would be an interesting option to encourage employees to pay off this debt but also help them continue to make progress on their retirement savings. I'm not the decision maker, though, so while it's interesting to me, I'm not sure what our executive committee would choose to do.

- I don't know if our employees would value this benefit. I question how many of our employees are still paying back their student loans. Would it count if they were paying their child's student loan that they had co-signed on?

- We are interested but haven't determined if we want to make it an option

- Amount of required documentation, reporting and qualifications would influence interest even if there were no issues with non-discrimination.

- Our match is not guaranteed but determined annually. It would depend on how the student loan repayment is structured.

- We haven't had much discussion about this yet. I would be in favor and would make a recommendation to the Plan Administration Committee if it didn't affect non-discrimination testing.

- We are making use of CARES Act allowing us to exclude up to $5,250 of educational assistance the employer provides to an employee under an educational assistance program from the employee's wages each year. As such, I do not think we would also offer matching contributions to 401K based on qualifying student loan repayments. IE: we are already helping our employees pay student loans.

- Would need more information on the cost, administration, and compliance requirements before we could make a determination.

- This question conflates 401k matches and student loan repayments. Two separate topics. I am not sure what is being asked.

- Interested only if the match is NOT in addition to an employer match that is directed to the retirement plan.

- Our organization has not started conversations regarding this yet but I anticipate it to be forthcoming. Personally, I would prefer to add, if no issues with testing.