Advertisement

PSCA Study Finds Roth Usage Doubled in Past Decade

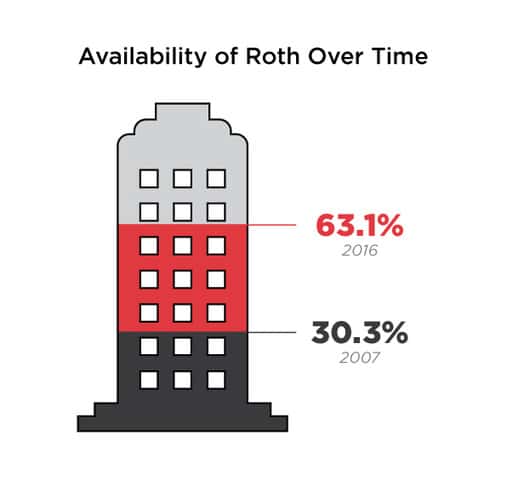

Roth availability doubled in the last decade according to the Plan Sponsor Council of America’s (PSCA) 60th Annual Survey of Profit Sharing and 401(k) Plans. PSCA, part of the American Retirement Association, found Roth was offered in 63.1 percent of plans in 2016 compared to 30.3 percent in 2007.

The Survey found that 7.2 percent of plans added Roth as an option in 2016, with the largest increase at 11.2 percent for plans with more than 5,000 participants.

Of the eligible employees that made contributions to a plan in 2016, 18.1 percent made Roth contributions. Interestingly, the highest percentage of Roth contributors comes from the smallest plan group - plans with 1-49 participants have an average of 29.2 percent of eligible employees making Roth contributions.

Roth deferrals are among the top six behaviors that companies monitor. According to the survey, 21 percent of all plans monitor investments of Roth deferrals.

"In the 12 years since Roth became available as an option where you already offer a 401(k) or 403(b) with pre-tax contributions, Roth features have demonstrated their value," said PSCA Executive Director Jack Towarnicky.

According to Towarnicky, there are some situations in which Roth contributions might be preferable to pre-tax contributions. Some workers:

are just starting their careers and may currently be subject to a lower marginal income tax rate,

- seek tax diversification as a hedge against potentially higher future income tax rates in years to come,

- are employed in a state that doesn’t currently have an income tax,

- want to build a legacy accumulation of assets that will not be subject to minimum required distributions,

- are limited by the 2018 Internal Revenue Code Section 402(g) contribution maximum of $18,500 and/or the 2018 414(v) catch-up contribution maximum of $6,000, and they know that an equal amount of contributions on a Roth basis represents a significantly greater savings rate,

- want to manage their taxable payouts in retirement with an eye on avoiding Medicare Part B and Part D income surcharges,

- are highly paid and are not eligible to contribute to an IRA on a Roth basis, and/or

- want to convert taxable monies to a Roth basis today, but they are not currently eligible for a distribution that can be rolled over and converted into a Roth IRA where plans with Roth features can permit in-plan conversions at any time.

PSCA’s 60th Annual Survey reflects the 2016 plan-year experience of 590 DC plan sponsors. The full survey is available to order as a hard-copy bound book or a PDF. It contains 182 tables of data covering topics such as automatic enrollment, employee eligibility, and investment advice.