Advertisement

QOTW: Multiple Retirement Accounts

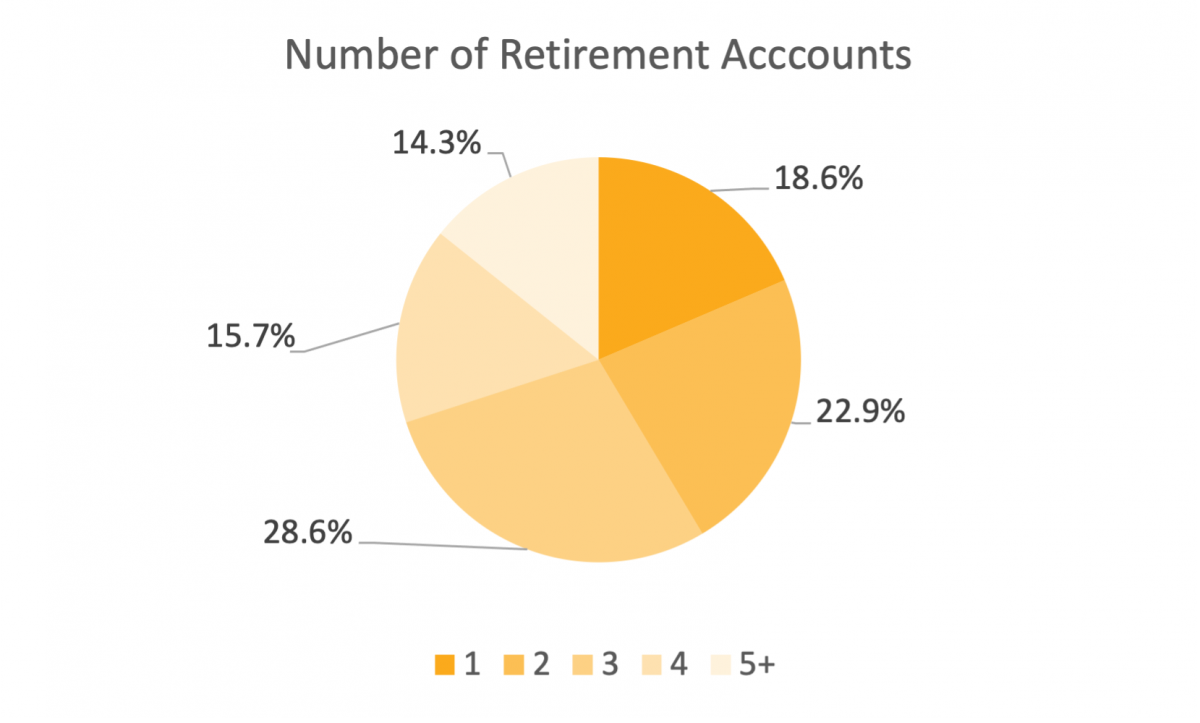

A PSCA member recently reached out with a question on whether retirement readiness projections based on average account balances are accurate as many of their employees state that they have other retirement accounts or pensions as part of their retirement mix (IRAs, 401(k)s from previous employers, military pension, etc.). To get a sense of this and to have a clearer picture of what the actual retirement preparedness landscape looks like, we asked members how many accounts they personally have and if organizations are taking any steps to determine the additional accounts employees may have and show that in retirement income projections. Fewer than 20 percent of respondents only have 1 retirement account with nearly 15 percent having five or more. A quarter of respondents stated that their spouse/partner had one account, and 37 percent stated they have two.

Nearly half of respondents (44 percent) stated that their organizations asks employees about additional accounts through their advice or wellness programs to get a fuller picture of their participants’ retirement preparedness.

Comments on if members think their employees have multiple accounts:

- Both our former recordkeeper and current recordkeeper have included in their toolkit the ability to add in other retirement accounts information for the projection of retirement income. The biggest challenge with this is both only incorporated balance information as opposed to more specific - investment level information which can obviously skew the actual investment performance over the planning horizon.

- Don't know. Our service provider site has an option for employees to enter additional retirement account information to take into account as part of its retirement planning calculator.

- Financial information is very sensitive and private. I like having the option for employees to have preparedness resources, but generally not sure how many save that information in their accounts. The ability to model it is more important than savings the actual data, as again that becomes too personal in some instances.

- I am guessing it is split down the middle...half do and half don't.

- I assume most management employees have multiple accounts, and a smaller percent of our retail employees do.

- I do expect most employees have multiple accounts

- I do think many employees have multiple retirement accounts.

- I think employees consolidate (rollover) into one account when they can, but that is not always feasible. It is common that this is not an option and many have at least a couple of accounts.

- I think many do have multiple, but I do not think most, as 78% of our team partake in single policies and a large percentage of those team members are under 35.

- I think many people have multiple accounts. And while we invite employees to aggregate them within our retirement plan for advice purposes, only a very small percentage do that. I doubt we have a clear picture of retirement readiness because people are providing the whole picture to us.

- Many I suspect.

- Many of the younger individuals have multiple retirement accounts as a result of job mobility. People are not staying with one employer as long as they did in the past. It does not always make sense to roll money from one retirement account into the new employer account.

- Most employees would have other account. 401Ks at former employers.

- No, most of our employees do not have multiple retirement accounts - less than 5% do.

- Not sure. There are many ways the millennials and younger seem to be accessing online stock and investments that do not exist as what I would think of as being a traditional retirement account. Are those included in your analysis?

- Our company uses Fidelity as our record keeper for our 401k plan and they have an on-line tool that allows a participant in the plan to add retirement financial information from all sources, in addition to their 401k, for a more accurate view of retirement preparedness.

- Our employee demographics are broad. Our higher-paid professionals may have but our lower paid would not.

- Our Fidelity relationship includes individual advice, which would include discussion of the employee's and spouse's other assets and accounts. In addition, we provide a financial wellness tool that employees can use to assess their preparedness. This tool is not linked to any of our plans, and employees enter their own retirement and asset data to obtain (confidentially) limited feedback about their retirement readiness.

- Our organization does not ask employees about other accounts and does not have sight on it. Our record keeper has a retirement readiness calculator that allows participants to add other accounts to help evaluate their preparedness.

- Our trustee/record keeper normally conducts one-on-one meetings with our participants to talk about retirement preparedness. Our plan participants are welcome to bring information on other retirement savings (outside of our plan) to the meetings.

- Ours is a multi-employer governmental plan, with 800+ employers reporting into the retirement system. Each employer has its own philosophy on employee education.

- Principal has a Retirement Wellness Planner that can be completed in the system by any employee. I believe its highly likely that many employees do not rollover former 401k balances into one account.

- Probably yes. I would expect that many would have a Roth IRA, traditional IRA, plus the 403(b) through their employer.

- Rank and file people who only have DC accounts will find retirement may be out of reach without additional sources of income (part time work?). DB plans provide lifetime income, but the government made administration so complex and the funding rules so expensive that many companies have closed, frozen, or terminated their DB plan. BTW, our DB and 401k administrators (different companies) both have benefit modelling and retirement projection tools, and both take "other sources of retirement income" into their model.

- Retirement readiness calculators have a lot of room for improvement.

- Service provider has capability to bring in outside accounts

- Some of our employees have multiple accounts. We make a strong effort to have them rolled over into one account with the help from our advisors.

- The projection tools we use allow a participant to add their other account balances either through linking them or by the dollar amount, which they will need to update periodically.

- The recordkeeper who also provides financial advice to our participants asks about participants' entire retirement financial picture, but we as an employer do not.

- The retirement calculator inside my 401K does ask about other balances.

- There is an option to link/add information however we don't ask employees to do so.

- they almost certainly do. but bringing in rollover balances is a double-edged sword - cuts both ways.

- This has always been my issue with these projections. The advice product we offer our employees always asks them for their other resources when doing their modeling. As would any financial adviser on an individual basis. I don't believe it is our job as plan sponsors to gather all this information. Disclaimers remind them that this is based on their 401(k) account only and encourage them to use the advice product.

- We are manufacturing and reasonably guess they only have one or two (401k from a prior employer).

- We do ask for this information if they complete an on-line survey, but honestly most people won't put the data in

- We do not ask employees to provide this, they have the option to do this through our record keeper.

- We have a 3rd party advisor who may ask them that but as a company, we don't ask.

- We often get a total balance estimate of assets held outside the plan. We don't typically get an accurate asset allocation of those assets and have trouble tracking the gain and losses over time.

- When doing orientation it is presented in a way so the participant can account for those other items in their decisions but we don't internally track this information or consider if someone is retirement ready.

- When you include spouses, most employees have multiple retirement accounts. Serious savers will also have multiple retirement accounts (IRAs and 401ks). Companies can add a financial planning benefits whereby employees can meet with a financial advisor (advisor must be a fiduciary to reduce risk to company). For companies not wanting to go this route, there are many planning options such as Personal Capital that one can use to aggregate accounts and do some rudimentary planning.

- Yes - they are financial professionals by trade

- Yes I believe most of our employees have a minimum of two accounts.

- Yes- we even get contacted by former employees to see if they still have an account because they aren't sure.

- Yes, a number of our employees have multiple plans

- Yes, after PSCA conference in May, we will be bringing this to the attention of new hires, perhaps a nudge. :)

- Yes, but few upload the info to our 401k recordkeeper's site

- Yes, employees have more frequent job changes. This would increase the likelihood of multiple accounts.

- Yes; I think many do not roll over when they take new position.