Advertisement

QOTW: SECURE 2.0 Emergency Savings Provisions

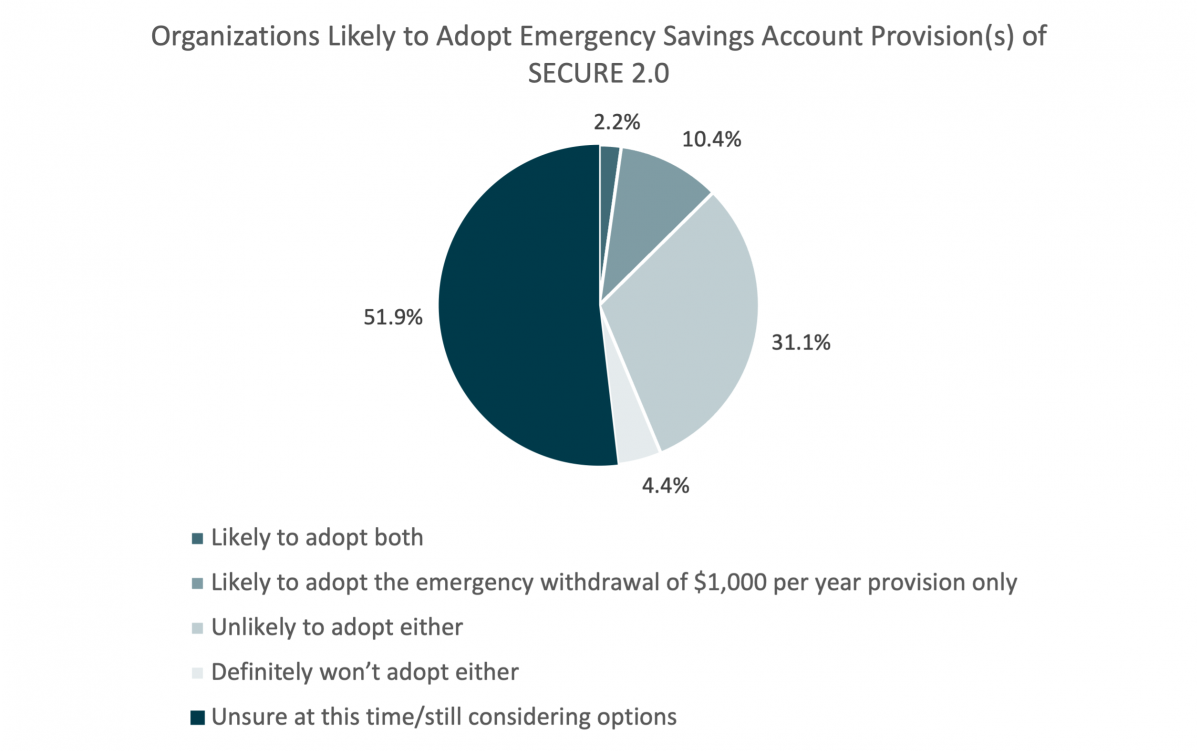

In the recently passed SECURE 2.0, there are two optional provisions geared towards helping participants create an emergency savings account. One option is to provide a side-car account where the employer matches money deferred into an emergency savings account with a matching contribution to the 401(k) account. The other option is a penalty-free distribution of $1,000 per year from the 401(k) account. In this week’s QOTW we asked members how likely they are to adopt one or both provisions. As a few indicated that it is too early to ask this question, more than half of respondents said they are unsure/still considering, while 10 percent are likely to adopt the $1,000 penalty-free emergency withdrawal per year, and only 2.2 percent are likely to adopt both. Nearly a third are unlikely to adopt either provision.

Comments from respondents likely to add the emergency distribution provision only:

- I like the idea. It may inspire people to save more if they can easily access some of the funds in an emergency with paying penalties.

- It is a lot of little details! Again, the HR world is tasked with implementing it.

- We don't currently have a 401(k) match; if we do implement one, I think we'd also adopt the sidecar provision.

Comments from respondents unlikely to add either:

- I don't understand the need to create more administration within the K plan when emergency savings accounts are available outside the plan everywhere. Our payroll will send a deduction anywhere you want.

- The penalty-free distribution appears to be a quick fix that will deplete participant's savings quickly. And we're not built to match any additional accounts.

- Think this just adds another layer of complexity to what employees can already find complex.

- We are a Safe Harbor plan so we would not 'Match' a savings contribution. Not sure about the $1000 distribution option. We will need to discuss that option.

- We encourage staff to borrow against their 403(b).

- We have a 403(b) retirement savings plan.

- While we are all for a paternalistic approach to helping employees, the additional administration associated with adopting these provisions and the limited additional participation value that we may gain do not seem to merit the change.

Comments from respondents unsure/still considering:

- I feel we are more inclined to consider the distribution option, but unlikely to consider the emergency savings account.

- I like the idea of it but am worried it's more options to move money away from retirement savings. Waiting to see the rules before any decision is made.

- Overall, I think the emergency account provisions were created with the right intentions, but I do wonder if employees already live paycheck to paycheck especially with rising cost of living, would they be prepared to sign up.

- Plan to adopt one or the other in 2024

- Something we are seriously looking at but have not made a decision yet.

- To early to decide this.

- We currently offer 2 401k loans, and may consider reducing that to 1 401k loan should we adopt the emergency $1k withdrawal provision. We definitely will not adopt the side-car provision.

- We have concerns with encouraging 401(k) distributions in populations that are already behind in saving for retirement. If we implement something, it would likely be a side-car account, which encourages more retirement savings on top of employees' own emergency fund saving.

- we want to adopt emergency savings account provisions. we have to put before committee.

- We'll likely adopt at least one if not both provisions but want to learn more about how our recordkeeper will accommodate each.

- While the idea has some positive attributes, the penalty-free distribution is just one additional way for a participant to miss out on future retirement funds.

- Will discuss at the next committee meeting. Unlikely to adopt penalty free distributions.

- Will have to determine paperwork requirements to make sure it is not too burdensome. We currently allow regular loans and hardship distributions, so we need to see how emergency savings would fit in.