Advertisement

The "Lost" Decade 2000-2009

Headlines in early 2010 claimed that December 2009 marked the culmination of a lost decade for investors. The alarming headlines could have easily triggered despair for 401(k) plan participants and caused them to sell their so called “losing” investments at the worst possible time — when the market was down.

Although not clearly stated in many of the headlines and associated articles, the claims of a “lost” decade were based upon a benchmark of the S&P 500 and ignored rates of return in other core categories of investments that are typically available to 401(k) plan participants. Other core categories had either positive rates of return or lower losses. See Exhibit 1.

So, was the decade really lost for 401(k) investors? Let's look at several examples:

The Hypothetical 401(k) Participant

Let’s take a look at Pat Smith, a 401(k) participant who began contributing to a 401(k) plan at the beginning of 2000 85 the height of a bull market that crashed later in 2000 and continued as a bear market through 2003.

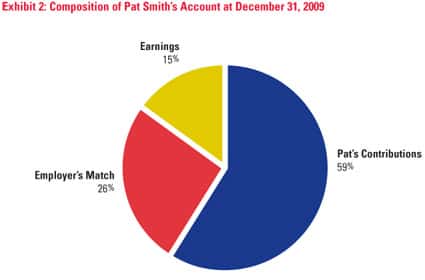

Pat’s salary was $35,000, and it increased 3% every year through 2009. Pat contributed 7% of his salary and his employer contributed 3% of his salary. Pat chose to invest 70% in an S&P 500 index mutual fund and 30% in an index fund based on the U.S. bond market.(6) Pat’s account grew to a little more than $47,000 by the end of 2009, with $28,000 coming from his contributions; $12,000 from employer contributions and $6,960 from investment earnings.(1) See Exhibit 2.

Despite Pat Smith’s entry into a 401(k) at the height of the bull market, his decade was not lost. Rather, he found that with a mix of equity and fixed income investments and regular, monthly contributions (dollar-cost averaging) he earned a positive rate of return — even though 70% of his account was invested in the S&P 500 index which lost 24% for the decade.

Pat Smith versus the Real World

Pat Smith’s experience is corroborated by a Fidelity Investments study of 401(k) account performance for 766,000 participants in Fidelity-administered 401(k) Plans who continued to fund their accounts and remained invested throughout the decade. The account balances of the participants increased an average of 150% from $65,800 to $163,900, with 25% of the increase attributable to investment performance.(2)

How did Pat Smith fare compared to the universe of Defined Contribution Plans?

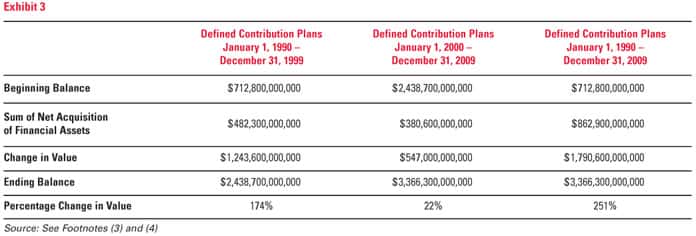

According to data from the Federal Reserve, defined contribution plans started the decade with $2.4 trillion in assets and ended with $3.36 trillion (January 1, 2000 – December 31, 2009). During the period January 1, 2000 to December 31, 2009, three-hundred eighty ($380) billion was attributable to Net Acquisition of Financial Assets and $547 billion came from investment earnings. Defined Contribution Plans reported in the Federal Reserve data earned a cumulative rate of return of 22% over the 10-year period, or a simple average of 2% per year.(3) See Exhibit 3.

Although the cumulative and average rates of return for the decade from January 1, 2000 to December 31, 2009 may not seem impressive, consider that they were earned after a decade (January 1, 1990 — December 31, 1999) when investment returns were lifted by a strong bull market and Defined Contribution Plans earned a cumulative rate of return of 174% (a 17.4% simple average).(3)

How do these numbers compare against Indexes?

Recognizing that defined contribution plans have different mixes of equities and fixed income, we looked at a representative average mix for defined contribution plans (as reported by the Profit Sharing Council/401k of America)(5), which was a mix of 70% equities and 30% fixed income. This mix would have resulted in a cumulative return of 17.75% (a simple annual average of 1.17%)(4) for the decade.

Conclusion

Over the last two decades, defined contribution plans have produced some impressive results as their assets increased from $712 billion to $3.3 trillion. Investment gains for the two decades are estimated to be $1.7 trillion, or 251% cumulatively (a 12.55% simple annual average).(3) and (4)

Despite the occurrence of four bear markets since 1980, participants remain supportive of defined contribution plans as revealed in the 2009 Investment Company Institute (ICI) Report, “Enduring Confidence in the 401(k) System, Investor Attitudes and Actions.” The ICI surveyed three thousand defined contribution plan participants and found that 9 out of 10 have a very favorable, or somewhat favorable, impression of 401(k) plans, and the number one reason supporting their favorable impression is “the ability of retirement plan accounts to accumulate significant savings.”(7)

Continuous innovation in the 401(k) industry has resulted in products and services that allow participants to diversify their investments whether through target date or risk-based funds, balanced funds, managed accounts, and fiduciary investment advice. Plan sponsors can play a critical role in helping participants stay focused on the benefits of diversification and avoid being distracted by the headlines.

For little, or no expense, plan sponsors can easily increase participants’ awareness of the benefits of diversification across equity and fixed income investments; re-balancing; and consistent dollar-cost averaging through payroll deduction. 401(k) plan service providers or record keepers may be able to assist with communication campaigns. Additionally, the Profit Sharing/401k Council of America sponsors “401(k) Day” each year and offers free post cards, posters, and articles targeted to different demographic and life-stage age groups. Plan sponsors can access these materials at http://www.401kday.org/401k-communications.

Questions or comments about this article can be directed to Mr. Prince at (317) 571-4560 or 600 E. 96th Street, Suite 575, Indianapolis, Indiana 46240.

Footnotes:

(1)Assumes: Contributions (both employee and employer) were deposited at the beginning of the month and invested 70% in the S&P 500 index and 30% in the Barclays Aggregate Bond Index; rates of return on the indexes were credited monthly; and the 70% / 30% mix was rebalanced annually. Past performance is not a guarantee of future results.

(2)Information about this study can be found at: http://www.fidelity.com/inside-fidelity/employer-services/fidelity-repor....

(3)Data obtained from the Federal Reserve Statistical Releases for Flow of Fund Accounts of the United States using the reports with release dates of June 10, 2010, March 4, 2004, and, September 16, 2002 which were obtained at www.federalreserve.gov/releases/z1/.

Data in these reports were obtained from the following charts and pages:

- September 16, 2002 Report — Pages 113 and 114 (Charts F.119.b, F119.c, L.119.b and L.119.c)

- March 4, 2004 Report — Pages 112 and 113 (Charts F.119.b, F119.c, L.119.b and L.119.c)

- June 10, 2010 Report — Pages 114 and 115 (Charts F.118.b, F.118.c, L.118.b and L.118.c)

(4)The cumulative rate of return is represented by the Percentage Change in Value for the 10-year period and is calculated by using the [(Ending period value minus Beginning period value – Net Acquisition of Financial Assets} divided by [(Beginning period value)].

(5)1999 Profit Sharing Council of America Survey of Defined Contribution Plan — the respondents’ approximate average allocation, rebalanced annually.

(6)Vanguard 500 Index Fund and Vanguard Total Bond Market Index Fund were used as proxies for the S&P 500 and the U.S. Bond Market. Calendar year returns for were obtained at: https://personal.vanguard.com/us/fundsindexonly

(7)The ICI Report can be found at http://www.ici.org/pdf/ppr_10_ret_saving.pdf

Disclosures:

- Past investment performance provides no guarantee of future results.

- The investment allocations in this article are for informational purposes only and are not to be construed as investment advice.

- Dollar cost averaging does not assure a profit or protect against a loss in declining markets. Investors should consider their ability to continue investing during periods of falling prices.

- Diversification and asset allocation does not ensure a profit or protect against loss.

- Target date funds are mutual funds that periodically rebalance or modify the asset mix (stocks, bonds, and cash equivalents) of the fund’s portfolio and change the underlying fund investments with an increased emphasis on income and conservation of capital as they approach the target date. Different funds will have varying degrees of exposure to equities as they approach and pass the target date. As such, the fund’s objectives and investment strategies may change over time. The target date is the approximate date when investors plan to start withdrawing their money, such as retirement. The principal value of the funds is not guaranteed at any time, including at the target date. More complete information can be found in the prospectus for the fund.

- Rebalancing may have tax consequences, which you should discuss with your tax professional.

- When investing in bonds, it is important to note that as interest rates rise, bond prices will fall.

- The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.

- The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) that serves as a benchmark of the performance in major international equity markets as represented by 21 major MSCI indexes from Europe, Australia, and Southeast Asia.

- The Russell 1000 index measures the performance of the 1,000 largest companies of the Russell 3000 index.

- The Russell 2000 index measures the performance of the 2,000 smallest companies in the broader Russell 3000 Index.

- The Russell Mid-Cap Index is a market capitalization weighted index representing the smallest 800 companies in the Russell 1000 Index.

- The Barclays U.S. Aggregate Bond index is designed to measure the performance of the bond market as a whole, including Government, Corporate, and Mortgage-backed securities.

- The Barclays U.S. Government/Credit Bond Index is designed to measure the performance of U.S. Treasuries that have remaining maturities of more than one year, government-related issues (i.e., agency, sovereign, supranational, and local authority debt), and corporate bonds.

- Investors should consider a mutual fund’s investment objective, risks, charges, and expenses carefully before investing. The prospectus, which contains this and other important information, is available from your Financial Advisor and should be read carefully before investing. The investment return and principal value of an investment will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost.