Advertisement

The Search for a Safe Way to Save for Retirement

There are three important elements of a safe investment vehicle:

- Principal protection: A safe investment vehicle maximizes the protection of a participant’s original investment.

- Predictable returns: A safe investment vehicle provides a high degree of predictability in the returns that it will provide in the near and medium-term.

- Sufficient returns: A safe investment vehicle must have a high likelihood of providing returns that will slightly outpace inflation in order to avoid a long-term deterioration in the real value of the participant’s principal investment.

Many participants need access to a safe investment vehicle. First, some participants may have a very short-term investment horizon. For example, near-retirees who plan to retire in a few years may need a “safe” investment vehicle to ensure that they will not lose a significant portion of their assets shortly before retirement. Second, some individuals may simply have a lower risk tolerance and are willing to give up potentially higher expected returns in exchange for less risk. For example, retirees may prefer access to a steady return on their retirement assets instead of opportunities for rapid growth. Finally, some participants may want to diversify their investments by investing a portion of their DC assets in a safe vehicle to balance more aggressive investments held within or outside their DC plan.

The recent market turmoil is increasing the focus on providing safe investment vehicles within qualified plans. With over $2 trillion lost in equities in IRAs and 401(k) plans in 2008, many individuals are reassessing their retirement investments and risk tolerance.1 Sponsors can respond to this need by ensuring that they are providing investment options within their DC plans that meet each of the three requirements of a safe investment option. Options with these characteristics will complement the other investment choices within DC plans, such as target-date funds or equity mutual funds.

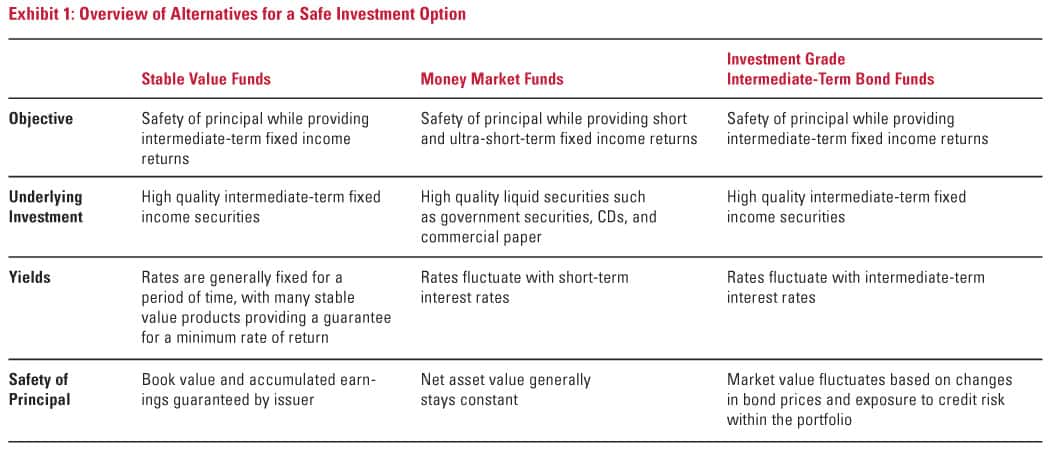

There are three primary alternatives for a safe investment option within qualified plans: stable value products, money market funds, and intermediate-term bond funds. An overview of these products is shown in Exhibit 1.

Stable Value Products

Stable value products combine an investment in intermediate-term fixed income securities with an insurance contract that guarantees the return of the investor’s principal and accumulated earnings. The source of earnings is a crediting rate promised by the stable value product provider. The crediting rate is usually only reset periodically, such as every quarter, and may be guaranteed to be above a “floor” for the duration of the investment.

Stable value products manage risk by investing in high quality securities. The insurance contract provides an additional layer of protection for participants by promising the return of participants’ principal and accumulated earnings whenever they wish to redeem their investment, even if the actual market value of the assets may have declined by this time. As a result, all stable value products protect participants against market value risk, i.e., the risk that a participant may have to redeem his or her investment at a time when the market value of his or her assets has fallen due to short-term fluctuations in bond prices. Stable value products may require staged withdrawals of participants’ assets if large-scale redemptions occur.

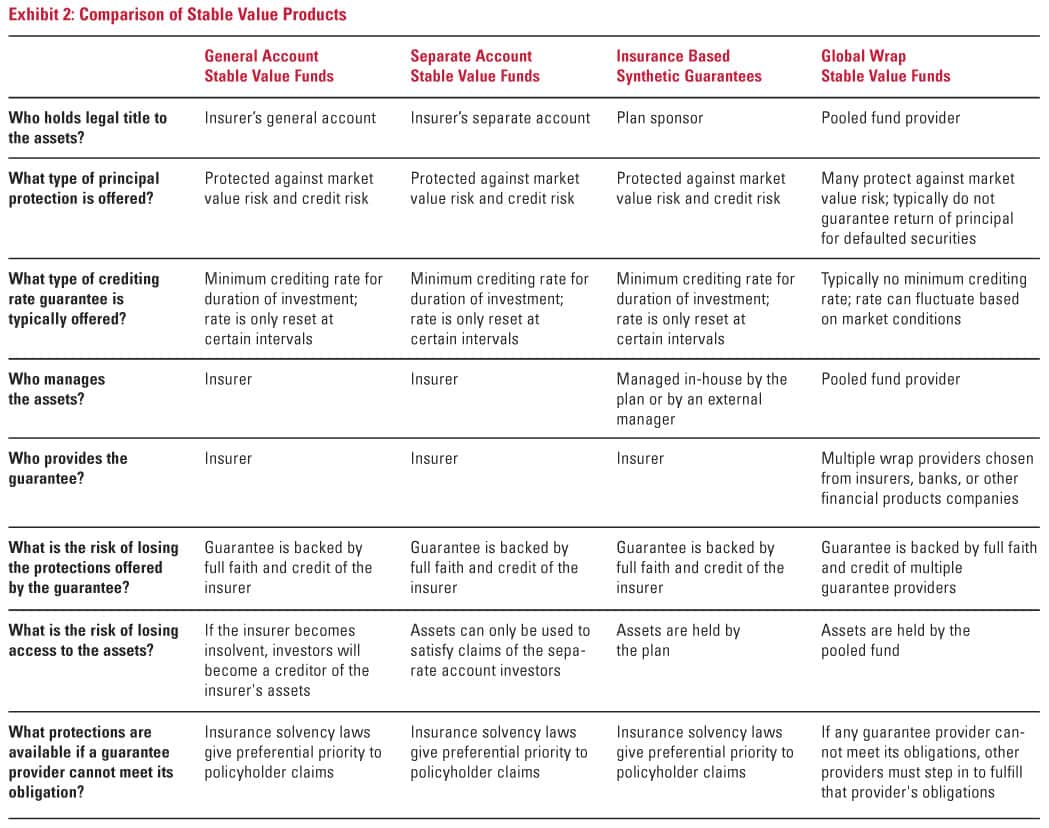

Guaranteed Investment Contracts (GICs), introduced in the 1970s, were the first type of stable value products. A GIC is a group annuity contract issued by a life insurance company that guarantees the return of an investor’s principal and accumulated earnings for a set period of time. In 1988, banks and investment managers began offering their own stable value products, called synthetic stable value products, by purchasing or manufacturing a contract to “wrap” a set of assets that they managed on their own. As a result, several types of stable value products have become available to plan sponsors:

- General account stable value funds. Plan sponsors invest their assets directly with the insurer providing this product. The insurer is both the investment manager and the guarantee provider. The insurer guarantees the plan’s principal against any loss, including the default of any underlying securities, and also promises that the crediting rate will never fall below a minimum. The assets are invested by the insurance company within its general account, which is used to support all of the liabilities that the insurance company is underwriting across multiple lines of business.

- Separate account stable value funds. These products differ from general account products in that the insurer invests the plan’s assets in a separate account rather than the insurer’s general account. As a result, the assets in the separate account can only be used to satisfy claims related to the investments made in the separate account, and are insulated from any claims on the insurer’s general account.

- Insurance based synthetic guarantees. These products enable plan sponsors to retain legal ownership of the underlying fixed income assets. The assets can be passively or actively managed either in-house by the plan, or by a third-party manager. The assets are then “wrapped” by an insurer. The wrap provider guarantees the return of investors’ principal and accumulated earnings, and also provides a minimum crediting rate.

- Global wrap stable value funds. These products differ from insurance based synthetic guarantees in several ways. First, the assets from multiple plans are usually combined into a single pool, managed by a stable value provider. Second, the pool purchases contracts from multiple providers, such as insurers, banks, or other financial products companies, to wrap the assets. The wrap providers guarantee the return of investors’ principal and accumulated earnings. Finally, an important benefit of these funds is that each wrap provider is obligated to proportionally assume the responsibilities, usually for a period of time anywhere from thirty to ninety days, of any wrap provider that is unable to fulfill its obligations. However, these funds generally do not provide a minimum crediting rate, and also do not guarantee the return of principal under certain conditions, such as the default of any underlying securities in the portfolio.

All stable value products have certain rules on the timing and level of plan withdrawals to prevent rapid, large-scale outflows that would strain the ability of the product provider to meet its obligations. Guarantees provided under stable value contracts are based on the claims paying ability of the issuing company

Money Market Funds

A money market fund is structured as a registered mutual fund that is required by law to invest in low risk short-term securities such as government securities, certificates of deposit, and commercial paper. Money market funds are legally required to meet three specific conditions:

- The weighted average maturity of the portfolio cannot exceed 90 days, with no single security having a duration greater than 397 days.

- At least 95% of the portfolio must be invested in securities that have received the highest possible short-term rating from at least two rating agencies.

- No more than 5% of the portfolio can be invested in any single issuer, with the exception of securities issued by the federal government or its agencies.

Money market funds pay dividends that fluctuate based on trends in short-term interest rates. However, these funds are managed to maintain a constant $1.00 net asset value (NAV) per share at all times to protect investors from any principal loss. Investments can be redeemed at the fund’s NAV at any time. Although the fund seeks to preserve the value of the investment at $1.00 per share, it is possible to lose money by investing in money market funds.

Investment Grade Intermediate-Term Bond Fund

Investment grade intermediate-term bond funds are mutual funds that invest in high quality bonds with maturities ranging from one to ten years. Bond funds do not have a maturity date because bonds are constantly bought and sold. Market conditions, such as the interest rate environment, constantly affect the interest paid on the fund and the fund’s market value. The fund’s level of risk depends on the credit risk of the underlying securities and the diversification of the overall portfolio. Shares can be redeemed at any time at market value; investors will experience a capital gain or loss based on changes in the prices of the underlying securities and based on any defaults that may have occurred within the underlying securities.

Stable Value is a Compelling Safe Investment Option

The three primary choices for a safe investment option within DC plans can be evaluated based on the key requirements for such an option:

- Protection of principal

- Predictable returns

- Sufficient returns

Stable value products meet these requirements more effectively and more comprehensively than the alternatives.

Protection of Principal

Stable value products provide explicit guarantees that promise the return of an investor’s principal. The type of guarantee offered does vary across stable value products. For example, general and separate account products provide an unconditional guarantee, backed by an insurance company, of the return of principal and accumulated earnings to the investor. As a result, such products protect investors from both market value risk, caused by short-term fluctuations in the prices of the underlying securities, and credit risk, caused by the possibility of default in an underlying security. By contrast, global wrap stable value products offer a narrower guarantee by protecting against market value risk, but not credit risk.

Not surprisingly, there is concern about whether stable value providers can meet their obligations during the current economic crisis. However, during 2008, every stable value fund produced a positive return for the year.2 There are several reasons why stable value providers are able to meet their commitments. First, stable value providers are regulated by a number of government entities, such as the Securities and Exchange Commission and state insurance regulators, which are focused on ensuring that stable value products are designed appropriately. Second, stable value providers are required to reserve capital to meet their obligations; this feature distinguishes stable value products because traditional investment products do not reserve capital to protect investors from losses. Finally, the guarantees inherent in stable value products align the interests of investors and asset managers because stable value providers have an incentive to invest conservatively.

Money market funds and intermediate-term bond funds, on the other hand, do not provide explicit guarantees that an investor’s principal will be returned. Money market funds typically attempt to maintain a level NAV to prevent capital losses. However, money market funds do not explicitly guarantee a level NAV and are not required to reserve capital to protect a level NAV. Money market fund investors have experienced losses on a few rare occasions when the investment manager was unable to maintain a level NAV. At such times, investors may also face a temporary freeze on redemptions as the fund manager attempts to stem a massive flood of withdrawals that could exacerbate losses. The federal government is providing a temporary guarantee for money market deposits, but this only applies to balances as of September 19, 2008.

Investment grade intermediate-term bond funds do not provide guarantees, either. Investors are exposed to both market value risk and credit risk. For example, if bond prices decline, investors who need to redeem their investment may incur a loss because the market value of the fund is likely to have fallen. Similarly, investors would experience a loss if a security within the fund’s portfolio defaulted.

Predictable Returns

Most stable value products promise a minimum crediting rate throughout an investor’s holding period. In addition, most stable value products also commit to only changing the crediting rate, which usually cannot fall below a minimum, at certain intervals, such as every quarter. As a result, investors in most stable value products can count on both a minimum rate of return, and also on receiving the current rate of return for a known period of time. Some stable value products, such as stable value pools, a specific form of a global wrap fund, provide a rate of return that fluctuates daily, based on market conditions, and as a result, do not promise a minimum crediting rate or a certain crediting rate for a set period of time.

In contrast, money market funds and investment grade intermediate-term bond funds do not provide a guaranteed minimum rate of return or a predictable rate of return. The returns for money market funds and intermediate-term bond funds fluctuate daily, based on changes in the interest rate environment. For example, returns on money market funds have fallen dramatically in the last year, with some funds yielding close to 0%. As a result, money market fund investors have seen a sharp reduction in the income that they were earning on their investment in such funds.

Sufficient Returns

A safe investment option needs to deliver sufficient returns so that investors will experience returns that at least keep pace with, if not exceed, inflation. Otherwise, investors could experience gradual erosion in the purchasing power of their assets. Analyzing long-term returns is one way to evaluate which alternatives help meet this requirement.

Dr. David Babbel and Dr. Miguel A. Herce of the University of Pennsylvania’s Wharton School conducted a study that compared the returns for stable value funds, money market funds, and intermediate-term bond funds from 1989 to 2008.3 During this period, stable value funds had the highest average annual return, 6.3%. Intermediate-term bond funds followed with an average annual return of 5.7%. Money market funds’ returns were 4.1%. These results are not surprising. Stable value funds and intermediate-term bond funds should deliver higher long-term returns than money market funds because the duration of the underlying securities in which these products invest is two to four years, compared to under a year for money market funds.

Each of the options has met the requirement of delivering positive inflation adjusted returns. During the 20 year period that the study was conducted, inflation averaged 3.0%.4 Stable value funds’ returns exceeded inflation by a much wider margin than money market funds’ returns, thereby delivering more significant growth in purchasing power for participants.The wide range of stable value products enables sponsors to select the optimal solution for their needs based on key criteria shown in Exhibit 2.

Sponsors seeking a “turnkey” solution can opt for general account stable value products, which only require the selection of a single provider that both manages the assets and provides the guarantee. Plans that want to insulate their assets from any unrelated claims on an insurer providing stable value products can use a separate account solution, although the guarantee remains backed by the full faith and credit of the insurer. Larger plans seeking full control of the assets they plan to invest in a stable value product can select an insurance based synthetic guarantee. Finally, plans seeking the assurance of multiple wrap providers backing the guarantee can select a global wrap product.

This comparison demonstrates one of the key trade-offs that sponsors must make in selecting a stable value product. Insurance based stable value products, such as general and separate account products or insurance based synthetic guarantees, provide the most comprehensive guarantees. Investors are relying on the insurer’s credit worthiness, but state insolvency laws provide an added layer of protection. Global wrap products provide investors with the benefit of multiple guarantee providers; each is required to fulfill the obligations of the others. However, these products generally do not promise a minimum crediting rate and provide less comprehensive guarantees for the return of principal.

Although the above comparison is generally true, it is important to note that significant differentiation may exist within each category of stable value products. There are several key questions that sponsors should ask when evaluating any stable value product and its associated guarantees:

- What does the guarantee provide in terms of principal protection and a minimum crediting rate?

- Are there any conditions under which the guarantee provider can back out?

- How strong is the guarantee in terms of the level of capital that has been reserved to back the guarantee and the credit ratings of the guarantee provider?

- What is the safety net in place if the guarantee provider cannot meet its obligations?

- How accessible are the assets under a range of scenarios such as the termination of the plan or any distress faced by the guarantee provider?

- Can the guarantee provider offer full transparency into the underlying investments in its general account or other balance sheet assets that support the guarantee?

- What are the fees and asset minimums to access the product?

The strong performance and robust features of stable value products have led to their widespread adoption within DC plans. In fact, about half of all 401(k) plans offer stable value funds as an option to their participants.5 Currently, stable value represents about $520 billion in retirement plan assets.6

During 2008, stable value products earned an average rate of return of 4%.7 This occurred while virtually every other asset class experienced double digit declines.8 The safety of stable value products drove more than $5 billion in transfers into stable value products within DC plans from other investment options.9

Conclusion

Plan sponsors need safe investment options to meet the needs of plan participants. There are many tradeoffs to make in determining which vehicle is most suitable to fulfill this need. Money market funds have relatively low volatility, but offer the lowest returns. Investment grade intermediate-term bond funds provide higher returns, but with significantly higher volatility. Stable value products, with their relatively high returns, low volatility, and protection features such as capital reserves to back guarantees, provide a compelling solution.

1For the one-year period ending October 9, 2008. “Are Retirement Savings Too Exposed to Market Risk?” The Center for Retirement Research at Boston College, October 2008.

2In the case of the Lehman Brothers bankruptcy, despite a negative return of 1.7% for the month of December 2008, Lehman’s Stable Value Fund earned 2% for the year. Source: “Answers to Issues Raised in the January 9, 2009 Wall Street Journal Article,” Stable Value Investment Association, January 9, 2009.

3Bedway, Barbara, “The Safe Haven in Your 401(k),” MoneyWatch.com, 2009.

4Bureau of Labor Statistics, “Consumer Price Index Data from 1913 to 2009,” 2009.

5“What Do You Need to Know About Stable Value Funds in Today’s Challenging Financial Environment?” Stable Value Investment Association, March 23, 2009.

6“What Do You Need to Know About Stable Value Funds in Today’s Challenging Financial Environment?” Stable Value Investment Association, March 23, 2009.

7Lankford, Kimberly, “Are Stable-Value Funds Safe?” Washington Post, January 19, 2009.

8Indexes maintained by S&P, MSCI, Citigroup, Dow Jones, and Credit Suisse.

9Bedway, Barbara, “The Safe Haven in Your 401(k),” MoneyWatch.com, 2009.