Advertisement

Best Practices for NQDC Plan Education

NQDC plans are very different from 401(k) plans — the education needs to be too.

A non-qualified deferred compensation plan (NQDC) is a strategic benefit utilized by employers to recruit, reward, retain, and retire key employees.

Participants value the unique tax preferences and wealth accumulation opportunities an NQDC plan affords them. That is, if they are aware of the benefits. Only slightly more than half of employers provide participant education specific to the NQDC plan according to PSCA’s 2019 NQDC Plan Survey. (See Exhibit 1.)

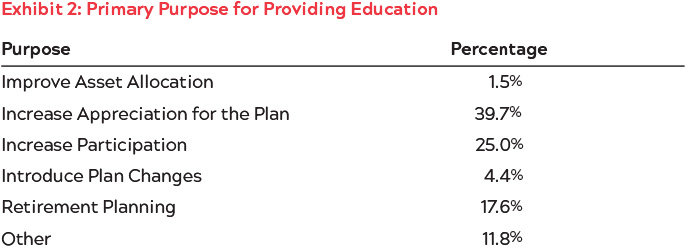

The survey also showed that the top two reasons employers provide specific plan education is to increase executives’ appreciation for the benefit and to raise participation. (See Exhibit 2.)

For their part, executives appear to recognize the importance of an NQDC plan. Despite its perceived value, however, executives often misunderstand the role an NQDC plan serves in helping them defer compensation for the future and to better plan for retirement. As such, plan sponsors have a responsibility to communicate the benefits to eligible participants in a clear and compelling way. Moreover, a properly deployed education plan is a critical component of plan success; it is particularly effective in increasing plan participation. It also significantly enhances the after-tax value of compensation executives actually receive.

For their part, executives appear to recognize the importance of an NQDC plan. Despite its perceived value, however, executives often misunderstand the role an NQDC plan serves in helping them defer compensation for the future and to better plan for retirement. As such, plan sponsors have a responsibility to communicate the benefits to eligible participants in a clear and compelling way. Moreover, a properly deployed education plan is a critical component of plan success; it is particularly effective in increasing plan participation. It also significantly enhances the after-tax value of compensation executives actually receive.

Plan sponsors seeking to improve NQDC plan performance should consider the following best practices for participant education:

1. Enhance the participant experience: Help executives understand the opportunities to take full advantage of the benefit being offered to them. In so doing, plan sponsors should evaluate the existing communication and education strategy.

Consider:

- Does it clearly explain the inherent advantages and risks of participating in the plan?

- Is it evident that the plan is an exclusive benefit, available only to a select group of management or highly-compensated employees?

- Does it provide simple, easy-to-follow enrollment instructions?

- Does it outline deferral parameters, i.e., that eligible employees can defer all or a portion of their salary, bonuses, or other forms of compensation each year?

- Does it explain how the plan is different from a qualified retirement plan (i.e., a 401(k))?

- Does it discuss applicable employer matching contributions and vesting requirements?

If the current education strategy does not adequately answer these questions, it is likely appropriate for employers to consider making relevant revisions.

2. Define applicable plan and regulatory rules: Participant education initiatives should also include information about the plan’s structure, operation, and administration as it pertains to executive compensation. Specifically, it is necessary to inform eligible participants that:

- Deferred compensation is not subject to state or federal income tax for the deferred period.

- Most plans contain a substantial risk of forfeiture dependent on the company’s future solvency or a potential change of control.

- Generally, NQDC plans are unfunded or unsecured by the employer, which poses additional risks.

- For the majority of plans, the Federal Insurance Contributions Act (FICA) and Social Security taxes apply when the services are performed and or become vested, and not later when the deferred compensation is distributed.

- There are no limits under the Internal Revenue Code as to the amounts that may be deferred on an annual basis (although the plan sponsor may impose limits).

- Participant communications should also specify distribution rules and describe applicable tax regulations. Among organizations that provide NQDC plan education, nearly 64 percent deliver education to participants taking a distribution.

3. Detail the risks: It is critical that plan sponsors ensure participants are aware of the relevant risks of deferred compensation plans. As previously mentioned, the plan assets are unsecured and generally unfunded. Moreover, if the employer becomes bankrupt or insolvent, the benefits provided to participants are essentially forfeited. In other words, NQDC plan assets are not protected, as the employer’s assets are used to pay the company’s creditors.

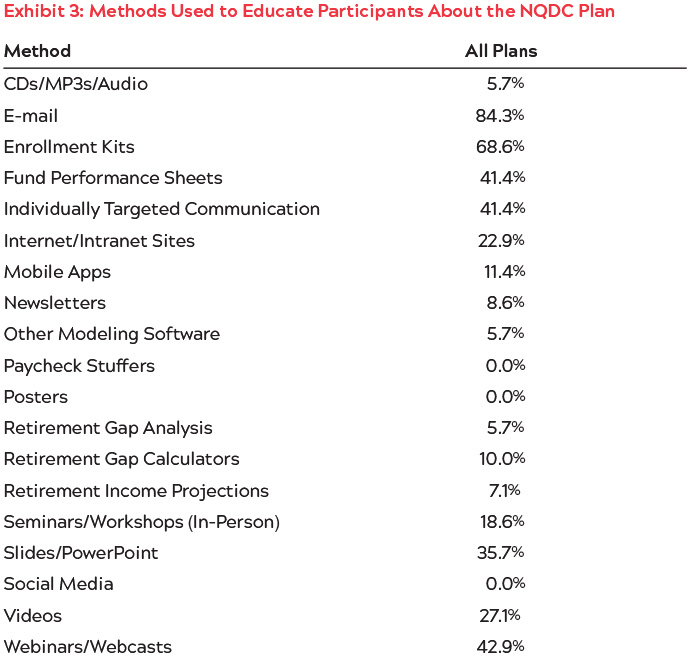

4. Adopt commonly-used education methods: The most prevalent methods used today to deliver NQDC plan participant education are:

- email (84 percent)

- enrollment kits (68 percent)

- webinars and webcasts (42 percent)

- fund performance sheets and individually-targeted communication (41 percent each). (See Exhibit 3.)

In addition, plan education is provided most often by the current plan provider (66 percent) or the plan sponsor (63 percent).

In addition, plan education is provided most often by the current plan provider (66 percent) or the plan sponsor (63 percent).

Whether the goal is to offer a competitive benefits package, help eligible executives to accumulate assets, or enable HCEs to defer the same proportion of their income as other employees, it is vital for employers to communicate the NQDC plan’s value. In addition, companies should focus on delivering executive communication initiatives that extend beyond the annual enrollment period. Education and communication should be an ongoing process, as the plan is essential to long-term financial planning.

By proactively communicating plan benefits and timely responding to executives’ concerns, employers can cost-effectively attract and retain top talent while helping key personnel navigate financial challenges.

NQDC plan sponsors should align themselves with an expert who can help them navigate the complexities of educating participants on the rules and risks inherent to NQDC plans.

Terry O’Prey is Principal & Senior Consultant at Vinings Management Corporation and a member of PSCA’s Non-Qualified Deferred Compensation Committee.