Advertisement

Why the 401(k) Will Prevail - and How

Recent criticisms of the 401(k) plan have understandably centered on the painful market-related losses of 2008. It has also been argued that, aside from being vulnerable to the vagaries of the markets, participants in defined contribution plans have made poor investment choices and have contributed too little to their accounts. A Time magazine article went so far as to suggest that employees would be better off covered by traditional pension plans or a form of government-sanctioned retirement insurance scheme.

While these critiques are well intended, they overlook three critical points. First, corporate America won’t — can’t afford to — return to the expensive and paternalistic era of traditional pensions, which undercut their competitiveness in a global economy. Second, the government’s principal retirement program — Social Security — is already stressed by the prospect of baby boomers retiring en masse. (Its capacity to replace pre-retirement income for this group is actually shrinking.) In a time of ballooning fiscal deficits, Congress will not relish asking taxpayers to shoulder additional liability for an expanded national retirement program. Third, and by happy contrast, the private-sector 401(k) program has the ability to adapt and improve. Its replacement capacity is rising due to the major reforms of 2006, and plan sponsors and providers are already finding ways to protect participants from a repeat of 2008.

401(k)s will continue to adapt and evolve

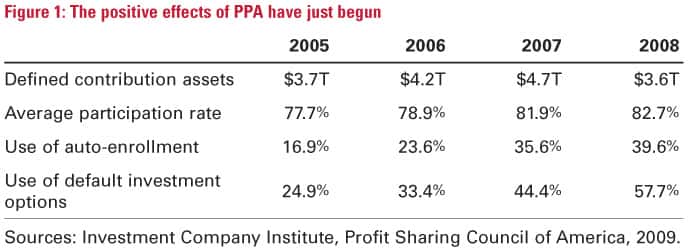

From a tiny presence in the early 1980s, defined contribution plans grew to enroll well over 70 million working Americans today, representing $3.7 trillion.1 This achievement is all the more remarkable, given that the first generation of DC plans was purely voluntary. Both plan sponsors and participants had to “opt in” by choosing to offer plans or by deciding to take part, respectively. In fact, this voluntary, multi-choice plan design required multiple decisions from participants: first, to enroll; second, to choose a deferral rate; and, third, to structure their own retirement investment portfolios from a growing array of options. Each choice was heavily dependent on expensive communication and education programs.

The ability of the 401(k) plan to adapt and evolve is key to its success. As workplace savings grew to represent a major commitment of assets, a wave of competition from mutual fund companies, insurers, and other providers drove continuous improvement in features and services — from daily valuations and online transactions to the creation of target-date funds.

The Pension Protection Act has much more to contribute

Even with rising markets — and maybe because of them — participation rates and deferral rates in defined contribution plans hit a ceiling in the first few years of this decade. While many people saw their accounts grow dramatically, investors were beginning to rest on their laurels or just tune out, and participants’ asset allocation decisions were frequently poor. Indeed, the underlying assumption that plan sponsors, providers, and advisors could somehow turn nearly every working American into a skilled pension manager seems overly idealistic today.

The passage of the Pension Protection Act (PPA) in 2006 was a major breakthrough because it endorsed some of the tactics that were actually having a positive effect on the health of the most progressive and far-sighted plans — features like auto-enrollment and auto-escalation, and diversified default options. One of the key lessons incorporated in the PPA based on participant behavior and the experience of cutting-edge plans was that inertia, defaults, and design determine results. The explicit endorsement of these features in the PPA was a recognition that many investors can’t manage, don’t enjoy managing, or simply don’t have time to manage their money effectively.

It’s important to point out that these features were already being implemented by a minority of plan sponsors. But fear of litigation made most others hesitate to adopt these ideas. By giving its blessing to these plan elements, and by granting legal safe harbor from litigation for employers who adopted them, Congress took these cutting-edge ideas into the mainstream.

In the years since the passage of PPA — despite the worst market declines since the Great Depression — we’ve seen enrollment rise, deferral rates increase, asset allocation improve, and participants remain steadfast. See Figure 1.

With the endorsement of these key design features, Congress essentially upgraded the first generation of workplace savings from an ad hoc, supplemental option to something resembling a fully fleshed out retirement savings system. The full benefit of the PPA was just being discovered when the market crash of 2008 swept through the system. With a growing perception that the worst of the markets could be behind us, Congress should recognize the protective benefits of these auto features and — just like seat belts or air bags — make them a fact of life through more robust legislation.

Addressing volatility can lead to better outcomes in retirement

One element that requires the most urgent response is protection from market volatility, which can no longer be written off as an unfortunate by-product of market-based 401(k) plans. We simply can’t afford another 2008. And although it was one of only three years since 1825 in which large-cap stocks fell more than 30%, it underscored a pattern of increasing volatility, with four down years — 2000, 2001, 2002, and 2008 — all occurring in the past decade.2

The fact that there will always be the possibility of future setbacks is why there must be a focus on volatility reduction in the next stage of workplace plans. And here is where the 401(k)’s inherent adaptability will shine.

For starters, we know that many providers across the industry are adopting a more conservative equity cap on mature-stage life-cycle funds. Although some target-date funds had conservative allocations of as little as 28% equity in their mature-stage portfolio, we know that many leading target-date funds held equity exposures well above 50%.3 Since 2008, a movement toward more conservative allocation has clearly occurred.

We also expect the industry to incorporate in 401(k) plans the kinds of actively managed asset allocation strategies traditionally employed by professional pension managers. In addition, this approach will be augmented by adding absolute return strategies into the glide paths of life-cycle funds. What makes absolute return strategies different — and therefore useful as a diversification tool — is that they provide for complete flexibility to invest across asset classes in pursuit of specific return goals, and they use active hedging to seek to limit downside volatility. Essentially, they strive to limit extreme variance in performance while pursuing more predictable results, which we know can result in greater income in retirement.

Assured income products will play a role

In addition to a focus on reducing volatility, we believe there will be a newfound embrace of assured lifetime income products, both in the form of annuities and non-annuity income solutions. In fact, this idea has already emerged in at least two bills introduced in Congress this year. The Lifetime Income Disclosure Act, for example, would require plan sponsors to estimate post-retirement income much as the Social Security annual statements do — and thereby encourage annuitization at the point of retirement.The Retirement Security Needs Lifetime Pay Act is more direct, letting retirees take a portion of their retirement savings in the form of an annuity, and allowing a 50% tax exclusion from certain annuity contracts for up to $10,000 a year.

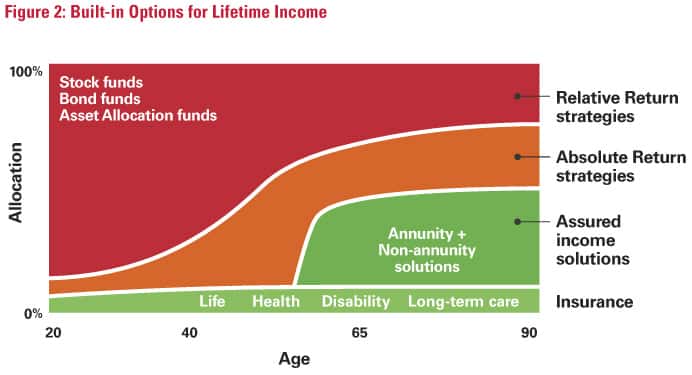

We also could see an assured income product embedded right into the glide path of a target-date portfolio (see Figure 2), with a rising share of a participant’s assets taken “off the table” and allocated into a guaranteed income vehicle as the participant nears retirement.

Of course, there will also be a greater focus on communicating the idea of retirement income directly to participants. At Putnam, we already talk to plan participants about projected monthly income rather than focusing on account balances. We believe this kind of orientation will encourage participants to use their plan data in a more actionable framework that connects their choices on savings rates and allocations to their real goal: post-retirement income. Rather than pursuing what may seem like an unattainable account balance, plan participants can strive to give themselves a raise in retirement. As the Lifetime Income Disclosure Act suggests, expressing retirement goals in this way will likely also encourage more participants to choose guaranteed income options.

Competition will continue to drive greater transparency and lower costs

On the business side, fee transparency will become a competitive advantage. This is another area where we see firms in our industry already stepping forward with innovative solutions such as providing a custom fee transparency commitment to each potential client once the economics of the plan are understood.

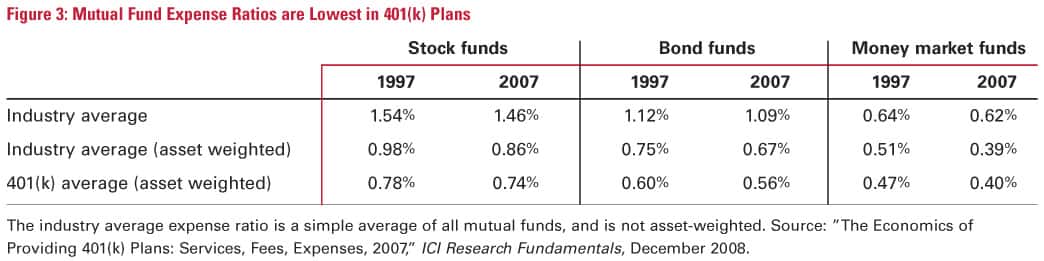

And today’s initiatives around fee transparency should only further the progression toward lower fees we’ve seen over the past decade. Figure 3 shows how fund fees have come down across stock, bond, and money market funds. And inside 401(k) plans, we find that fees are even lower on average than those in the industry at large.

Coverage will be extended to more Americans

Finally, as Congress continues to debate financial industry reform in 2010, we hope to see legislation that will include creative, cost-effective ways to extend coverage to all working Americans. Cost and complexity are the primary reasons why many small employers don’t offer plans. The solution will likely mean compensating companies with tax incentives to cover the costs, designing streamlined, low-overhead savings models — with minimal red tape — and offering workers matching grants on their savings, perhaps from general government revenues.

Industry innovation and policy support will make it happen

The evolution of the 401(k) has been marked by a partnership of plan sponsor desire for improvement, industry innovation, and policy support. That partnership is infused with a sense of urgency today as we debate the future of our retirement system. It is time again for plan sponsors and providers to continue that tradition of innovation and to begin acting to pioneer the best practices that will lift workplace savings to a new level.

The 401(k) plan should prevail despite its detractors because it is the only system that harnesses the historically positive upward trend of the markets; because it makes corporate America more competitive, not less; because it places no additional burden on our country’s stretched budget; and because it can improve — and has improved — over time. Let’s make 2010 a Year of Retirement Innovation.

1 Investment Company Institute, 2009.

2 Ibbotson/Morningstar 2009 Yearbook.

3 Putnam research, 2009.