Advertisement

Looking For A Few "Good" Plan Sponsors

You’ve probably heard or seen the Marine Corps ad – “Looking for a Few Good Men.” Well, I am starting a search for a few “good” plan sponsors.

Many plan sponsors have themselves been searching for a payout or “decumulation” solution. Today, more than ever before, participants are leaving assets in the plan after separation. That’s a big shift compared to the early 1980’s when many elected lump sum distributions in part to capture the tax preference from 10-year forward averaging.

Plan sponsors for individual account retirement savings plans have considered annuities, the 4% rule, guaranteed withdrawal benefits and other options. Most have yet to act. Some are concerned about the fiduciary exposure of making a choice for their participants. Perhaps that describes you.

We’ve seen more and more plans add new post-separation payout options – ad hoc and installment payouts, provisions allowing participants to repay loans and to initiate a loan post separation, etc. Of course, your plan probably has a “default” payout option - the Required Beginning Date (RBD) for Minimum Required Distributions (MRD). Failure to commence payout(s) in the appropriate amount(s) by the time a separated participant reaches April 1st of the calendar year following the year the participant turns 70 1/2 may trigger a 50% excise tax penalty (See: Internal Revenue Code (IRC) §§ 401(a)(9), 4974(a)).

Note: In my last plan sponsor role, we asked a top benefits consulting firm to recommend changes that would raise retirement readiness without adding cost - the “holy grail” of 401(k) design. They suggested account aggregation/consolidation and payout strategies (annuities, etc.) could increase replacement rates without adding cost.

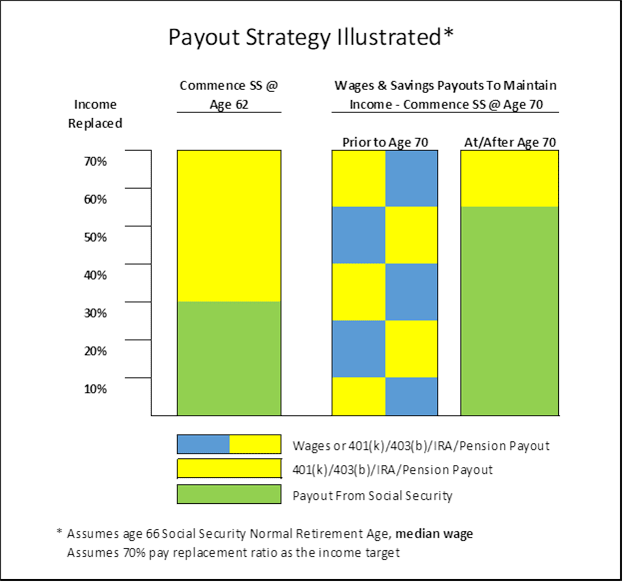

Recent research by the Stanford Center on Longevity (SCL), collaborating with the Society of Actuaries (SOA), identified a straightforward payout strategy for individual account plans (401(k), 403(b), IRA, etc.) that may be optimal for most middle-income retirees. This payout strategy delays Social Security until age 70 for the primary wage-earner and uses the RMD payout process to back into how much to distribute from savings. This payout strategy may be optimal for participants and plan sponsors focused on maximizing guaranteed income in retirement. The negative? This payout strategy may substantially reduce other assets and liquidity throughout retirement.

I am old enough and have been in the retirement benefits industry long enough to think of this as a “level income option” with a twist. The goal continues to be a consistent level of income replacement, but the target is the maximum amount of guaranteed income. This is also an opportunity to educate participants with regard to retirement income needs. The twist is that instead of separating before age 62, accelerating payout of pension or savings and then commencing Social Security benefits at age 62, here the strategy is for workers to continue employment, or, when employment stops, cash out savings so as to defer commencement of Social Security until age 70.

So, I am looking for plan sponsors who are looking for a payout option solution to offer participants who commence prior to the RBD. Are you interested in considering a payout strategy determined to be one of the best available by members of the Society of Actuaries and the Standard Center on Longevity? If so, if you are interested in innovating and improving retirement preparation outcomes, please contact me at [email protected].