Advertisement

Risky Business - Retirement Risk Taxonomy

Carol Bogosian will present the results of Society of Actuaries post-retirement risk analysis at the PSCA's 71st Annual National Conference.

Many Americans envision a retirement of leisure and travel – financed by federal entitlements like Social Security and Medicare and participation in retirement savings plans. Plan sponsors rightfully focus on risks that would defeat participants’ retirement preparation such as failure to participate, to save enough, to select appropriate investments, or other factors within their control. Solutions plan sponsors increasingly deploy include automatic features and qualified default investment alternatives.

Plan sponsors and participants often limit our focus on retirement risks where there is a readily available solution – something we can control. However, the risks we face are much more diverse. Many are unknown, and perhaps unknowable, part of a very uncertain future environment that is not easily dealt with by plan sponsors or participants. As a plan sponsor, you may want to reconsider all of the risks participants face in their preparation that are uncontrollable - with an eye on addressing issues through advocacy, as well as plan design, communication and administration.

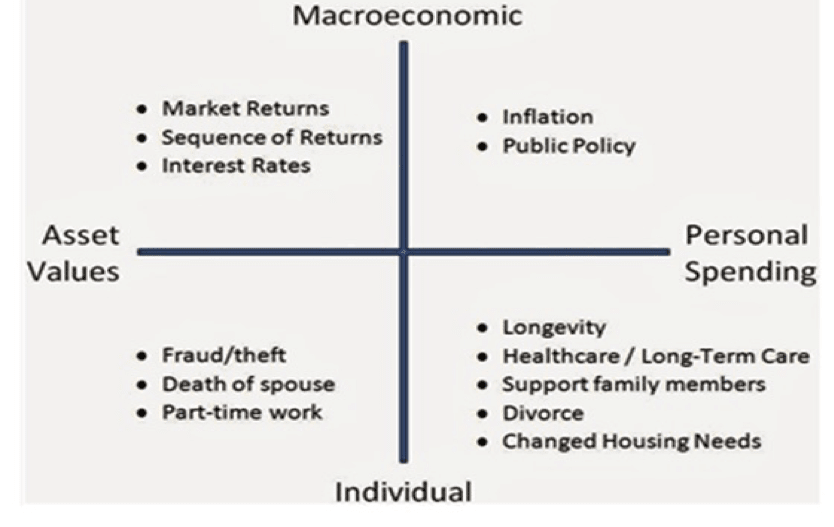

A taxonomy is a scheme of classification. The following example presents a model of risks to retirement preparation:*

Horizontally, this taxonomy distinguishes risks based on which side of the balance sheet is put into jeopardy (asset accumulations or retirement spending). Vertically, risks are separated by whether they are macroeconomic (impacting society as a whole) or individual specific. Plan sponsors and participants may fail to consider many of these risks because we may be unable to directly influence them. But these risks are real and potentially significant.

In the upper left, you have macroeconomic risks to the asset side of the balance sheet. Poor market returns, especially poor market returns near or shortly after the date of retirement, can matter a great deal. In the upper right you have inflation. Historically, pre-retirement inflation risk was often addressed by wage increases commensurate with increased experience and productivity. This is less likely in today’s global economy. Dealing with post-retirement inflation may involve deferring benefit commencement.

In the lower right, microeconomic risks include longevity, individual physical/mental health, mobility/frailty/cognitive challenges as well as changes in family needs and status. Asset retention in a plan subject to fiduciary protections may become a more prevalent strategy. Increasingly, plan sponsors are developing strategies that leverage the tax preferences only available through Health Savings Accounts as a method for funding post-retirement medical premium, out of pocket and long-term care expenses. Sure, we can all look up IRS life expectancy, but each of us, our actual length of life on an individual basis is truly unknown.

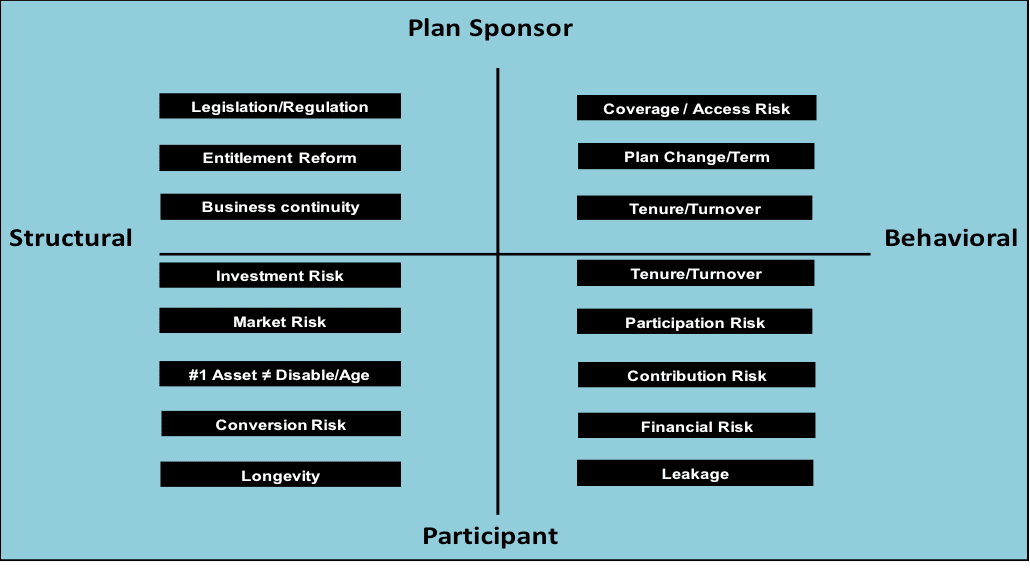

Consider the second retirement risk taxonomy below.** Horizontally, the continuum is from structural to behavioral risks. Vertically, the taxonomy differentiates issues affecting plan sponsors and participants.

In the upper left are broad, structural risks. As health reform, tax reform, entitlement reform, other legislation and regulation confirm, these could significantly disrupt a participant’s retirement preparation - including decisions made long ago. It makes advocacy in favor of our voluntary retirement system an imperative. At the same time, the exposure from business continuity is somewhat lessened by the erosion in defined benefit plans, though substantial risks remain due to historical, deliberate underfunding of public and multi-employer pension plans.

In the upper right, keep in mind that many employers do not sponsor plans. And, even where a plan is available, individuals may not participate. For example, for the past 36 years, all wage earning Americans have had access to a tax preferred retirement savings vehicle that would enable them to successfully prepare for retirement – the Individual Retirement Account (IRA). Perhaps your new hires last worked for an organization that did not sponsor a plan. Or, maybe your new hire was not eligible or may have been a member of the “gig” economy. Importantly, over the past 40 years or so, the average tenure or length of service among American workers is just over 5 years. So, chances are that most workers will have one or more periods of employment without access to an employer sponsored plan. Does your plan pursue asset rollovers from predecessor employer plans and IRAs? Does your plan welcome and pursue post-employment IRA contributions, and rollovers from IRAs and subsequent employer plans? That is, does it seek to reduce leakage through account consolidation and aggregation?

In the lower right, many workers fail to enroll when first eligible, don’t contribute enough and some have other, more current or pressing financial priorities. Then there is the substantial risk of pre-retirement leakage, a risk recently increased by legislation which will remove impediments to hardship withdrawals. Some plans avoided this leakage - some never added hardship withdrawal provisions while others eliminated that provision.

And, finally, in the lower left are investment, market, conversion and longevity risk. Few workers can effectively manage an investment portfolio, the challenge of equity investment volatility after retirement (affecting the payout rate) and conversion risk (the interest rate risk when converting savings to income at retirement).

Add to that the risk participants face in terms of their #1 asset, their ability to earn an income – potentially impacted by disability and age, as recently demonstrated by the results of the 2009 recession and our modest recovery. Workers increasingly express a desire (and/or need) to continue employment beyond historical “normal” retirement ages and face what some call “re-employment risk”. Society of Actuaries studies confirmed that 90+% of those ages 58 – 62 work full time, however, the percentage who were working for the same employer they had at age 50 declined from 70% (1983) to 46% (2006). Increasingly, if you want to continue employment, it may be necessary to change employers. Have you reexamined your available policies that will successfully transition workers into retirement as one means of addressing or transferring longevity risk?

Bottom line, when it comes to retirement planning, even in situations where plan sponsors have some control, we all lack a crystal ball to predict most of the risks our participants face - legislation, turnover, regulation, recessions, business continuity, and changes in participant behavior.

* Wade Pfau, MarketWatch, Wall Street Journal, 3/24/14, “Breaking Down Retirement Risks,” Accessed 20180320 at: https://www.marketwatch.com/story/breaking-down-retirement-risks-2014-03...

** Author’s analysis; incorporating: Wade Pfau, MarketWatch, Wall Street Journal, 3/24/14, “Breaking Down Retirement Risks”; Alana Semuels, LA Times, 2/22/14, “Detroit bankruptcy plan includes deep pension cuts”; David Laibson, Harvard University, Institutional Investors, 2011; Craig Copeland, EBRI, Employee Tenure Trends, 1983–2016, September 2017, Vol. 38, No. 9, Accessed 20180320 at: https://www.ebri.org/publications/notes/index.cfm?fa=notesDisp&content_i...