Advertisement

Access: The HSA In Your Future: Defined Contribution Retiree Medical - Part 2 of 3

A month ago, I previewed one of my presentations at the World at Work, Total Rewards Conference.

Back in 2004, I predicted: “Twenty five years ago, no one had ever heard of 401(k), twenty-five years from now, everyone will have a HSA!” If you offer health coverage and/or an individual account retirement savings plan like a 401(k) or 403(b), but you do not offer an HSA-qualifying health option, your workers are missing out on America’s most lucrative benefits tax preference. An HSA is a kind of a combination of a Health Flexible Spending Account (FSA) and 401(k) or 403(b) plan. It may be better than either. The HSA offers great value today and tomorrow. Plan sponsors should reconsider any decision not to offer a HSA-capable option because an HSA can add significant value to your Total Rewards package.

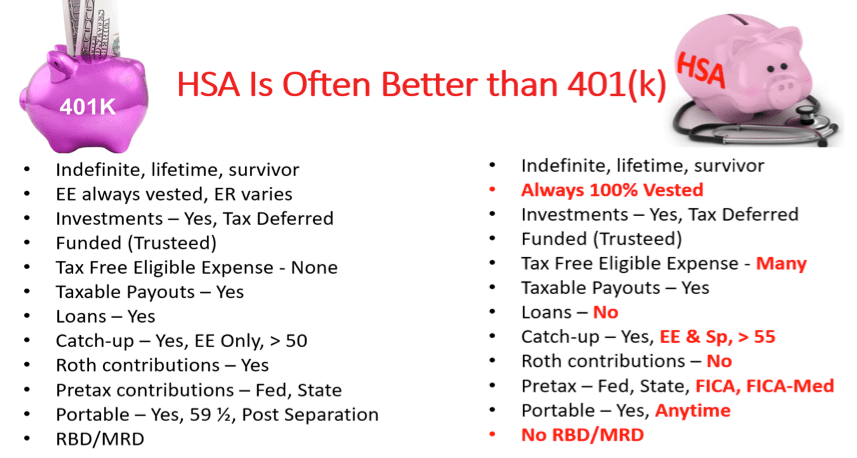

HSA Compared to a 401(k) and Health Flexible Spending Account (FSA)

The HSA’s tax preferences coupled with current and future use options may make it more valuable to workers than contributing a similar amount of take home pay to a 401(k) or 403(b) – with differences highlighted in red:

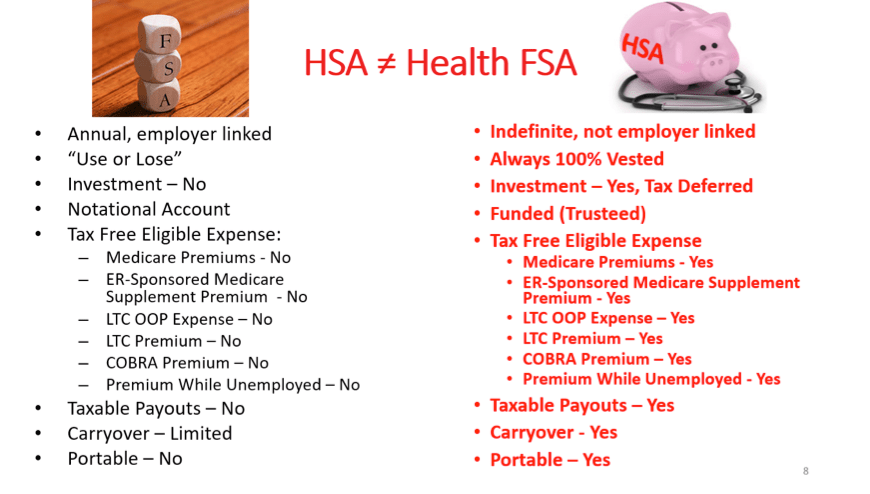

And, the HSA is different from and generally superior to a Health FSA. The HSA is not limited to be a “Super FSA” – again, with differences highlighted in red:

HSA Access is Lacking – So, Most Workers Miss Out

Only a minority of workers have access to an HSA-qualifying health option. Only a subset of those eligible actually select the HSA-capable option. Even fewer who select that option contribute to the HSA. And, only a miniscule minority of those who contribute invest HSA assets. For comparison, workers who do not have access to an employer-sponsored retirement savings plan can at least save and invest using a tax-favored Individual Retirement Account. Detail:

- Only 17% of private sector employers offer an HSA-capable option.1

- Only a subset of the eligible are enrolled in an HSAs-qualifying option.2

- While there are 22 Million HSAs accounts, 20% had a zero balance at year-end 2017.3

- Only 48% of HSAs received employee contributions and only 4% of HSAs accounts had non-cash investments.4

Reconsider the two comparison charts. That is, if you offer health coverage or if you offer a 401(k) or 403(b) plan, your workers may be better served if you also offered access to an HSA-capable health option. Now that we have fourteen years of experience with HSA-capable health options, employers also have access to well-developed transition options. The third and final post regarding The HSAs in Your Future will focus specifically on using a Health Savings Account to accumulate assets for retirement, and especially to maximize the tax preferences available for retiree medical expenses.

1 Kaiser/HRET Survey of Employer Sponsored Health Plans, September 2017

2 AHIP, Health Savings Accounts and High Deductible Health Plans Grow as Valuable Financial Planning Tools, April 2018

3 Devenir, 2017 Year-End HSA Market Statistics & Trends, February 2018

4 EBRI, Trends in HSAs Balances, Contributions, etc. 2011-2016, July 2017