Advertisement

The Sky is Not Falling on Older Americans

Widespread Poverty Among America’s Seniors? No.

Just a couple of weeks ago, a few publications ran stories predicting that older Americans reaching retirement age were in “worse financial shape than the prior generation for the first time since Harry Truman was president.” Academics were suggesting today’s and tomorrow’s seniors would soon be living a life in poverty. One study stated: “Based on current trends, we will soon be facing rates of elder poverty unseen since the Great Depression. By 2035, nearly 20 million retirees will be living in poverty or near-poverty. By 2050, that number will reach 25 million.”

Who or what is to blame? The same study confirmed that: “The decline of pensions and increase in 401(k) … plans is one reason many seniors aren’t as ready for retirement as the previous generation,” and, “For many Americans facing a less secure retirement than their parents, the biggest reason is the shift from pensions to 401(k)-type plans.” It just isn’t so. Studies suggest that poverty among older Americans, which was once greater than 30%, is as low as it has ever been. Some estimates place poverty among older Americans at rates approaching 5%. Vested, accrued pension benefits were never all that prevalent.1

But yes, some older Americans will be poor. Some will have been poor all their lives and will enter older ages in the same status. And the reasons for that poverty are more complex than reported.

Half of All Bankruptcies in America are Medical Bankruptcies? No.

In addition to the decline of pensions and increase in 401(k) plans, the other factor that comes in for much of the blame, for poverty and bankruptcy among older Americans, is out-of-pocket medical expenses. You heard a lot about that during the run up to passage of health reform.

Specifically, with respect to Medicare beneficiaries, it is important to note that the average annual increase in point-of-purchase cost sharing under Medicare (deductibles, copayments, etc.) has increased about 3% per year during the past 35 years (since the early 1980s) while out-of-pocket spending on drugs has dramatically declined due to the Medicare Modernization Act of 2003 and the Patient Protection and Affordable Care Act of 2010.

Further, approximately 20% of the elderly are dual eligible – Medicare and Medicaid – meaning their premiums are often waived as are many cost-sharing features.2

Most personal bankruptcies are NOT the result of unpaid medical expenses, and that is certainly true for older Americans.

Two such studies were used to justify the Patient Protection and Affordable Care Act of 2010 – also known as health reform. For example, in the 2005 report studying 2001 medical bankruptcies,3 a bankruptcy was deemed to have a medical cause if:

- the survey respondent said so;

- there were uncovered medical bills exceeding $1,000;

- a household member lost at least two weeks of work-related income due to illness or injury;

- or home equity was used to pay medical bills.

Therefore, the high percentage of medical bankruptcies resulted from using a gerrymandered definition. The 2009 report that studied 2007 bankruptcies wasn’t much better. The average discharged indebtedness for a medical bankruptcy was $44,622. Non-medical bankruptcies had an average indebtedness of $37,650.

Medical bankruptcies discharged an average of $4,988 of medical debts. Ask yourself this question: would everyone have avoided filing for bankruptcy if their indebtedness had been "only" $39,634 ($44,622 - $4,988)? Conversely, would everyone still have declared bankruptcy if they only had the $4,988 of medical debts to discharge and no other outstanding debts?

Both studies were hopelessly flawed. The authors failed to note that most of the debts discharged by bankruptcy were NOT due to medical expenses (although it is possible that some of the credit card and other debt was incurred to pay medical expenses).

Most of those same researchers studied so-called "medical bankruptcies" in the years after Massachusetts added its Connector and concluded, "Health reform has not decreased the number of medical bankruptcies, although the medical bankruptcy rate in the state was lower than the national rate both before and after the reform."5

Simply, those researchers used the wrong objects of comparison in the study - they should have identified individuals with comparable medical expenses, medical insurance, and out-of-pocket cost sharing and compared those who filed for bankruptcy and with similarly situated individuals (in terms of medical expenses) who did not file for bankruptcy.6

Soaring Bankruptcy Rates Among America’s Seniors? No.

More recently there is a study claiming dramatic increases in the number of American seniors who declare personal bankruptcy.7 The authors state that Americans age 65+ are “increasingly likely to file consumer bankruptcy, and their representation among those in bankruptcy has never been higher.”

The study notes “a two-fold increase in the rate at which older Americans (age 65 and over) file for bankruptcy and an almost five-fold increase in the percentage of older persons in the U.S. bankruptcy system.”

In addition, “Comparing … data between 1991 and now shows significant increases.” And “The changes are so great that the broader trend of an aging U.S. population can explain only a small proportion of what is happening in the bankruptcy courts.”

Is that so? After a quick review, it again appears more like gerrymandering to me.

Table 2 of the study shows filing rates per 1,000 individuals in the population8:

- For individuals ages 65-74, the bankruptcy rate was 1.2 individuals per 1,000 in 1991 and 3.1 in 2001 (10 years later – a substantial, average annual increase of 10%!) However, in 2016, the rate was 3.6. So, the last 15 years saw a moderation in the increase in bankruptcy filing – a minimal, average annual increase of less than 1% per year!

- For individuals ages 75+, the bankruptcy rate was .3 individuals per 1,000 in 1991 and 2.3 in 2001 (10 years later – a substantial, average annual increase of 22.5% per year!). However, in 2016, the rate was 1.3. So, the last 15 years saw a reduction in bankruptcy filings – a decline of 3.5% per year!

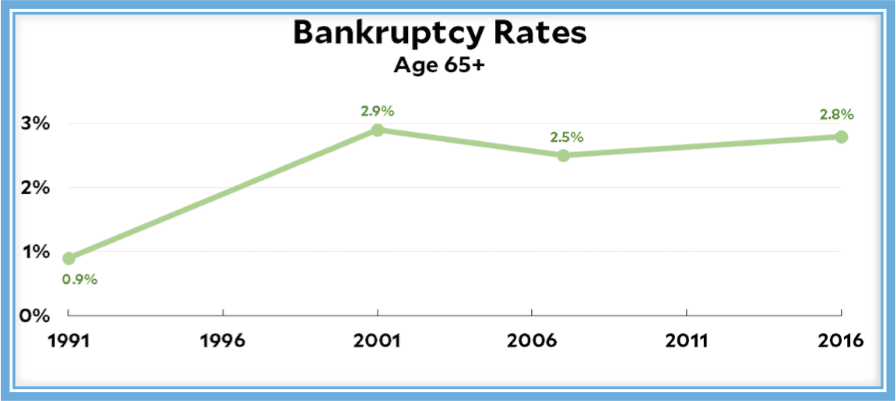

The statistics for bankruptcy for those age 65+ were somewhat consistent as for other ages. When the data for all ages greater than 65 is combined, the graph shows how rates have been mostly unchanged the past 15 years, despite the total re-write of the federal bankruptcy code in 20059:

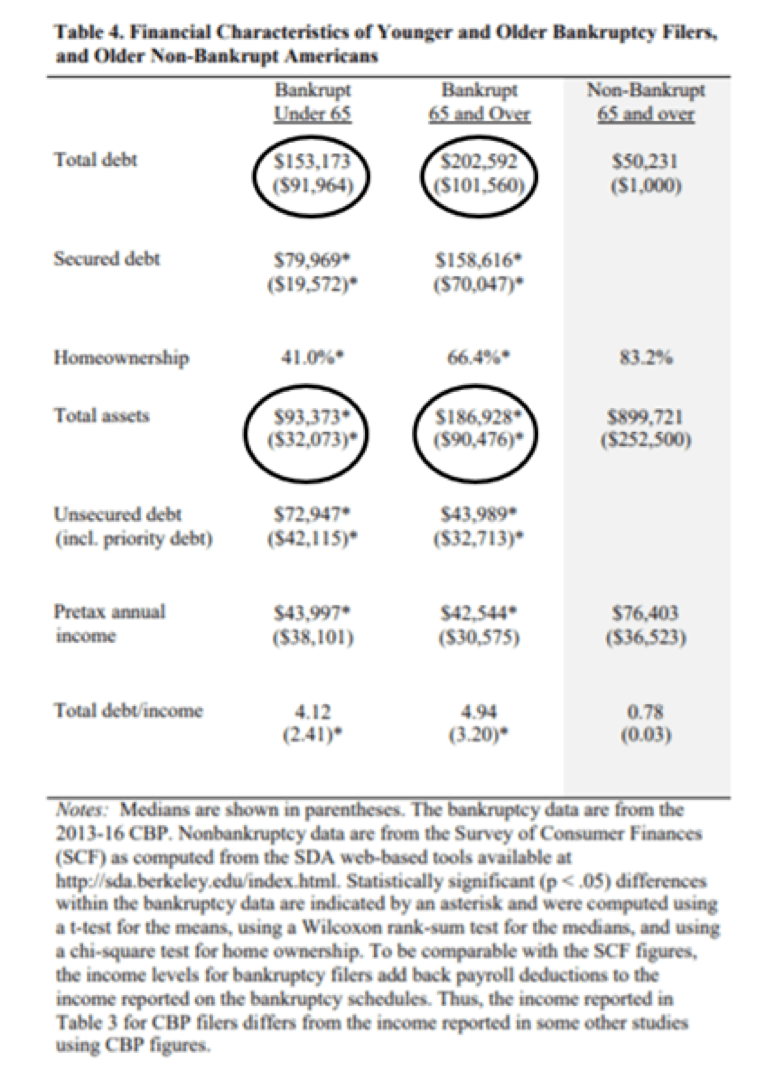

See also Table 4 from that study:

From what I gather when comparing medians, the bankrupt individuals younger than age 65 have a median net worth of ($59,891): ($32,073 of assets - $91,964 in debts). However, the bankrupt individuals age 65+ have a median net worth of ($11,084): ($90,476 assets - $101,560 debts).

Much of the debt for older bankrupt individuals is secured debt (an average of 66.4% here). However, a home, ERISA retirement plan assets, and IRA assets are generally protected under bankruptcy laws.

I also am aware that there are very, very diverse federal and state laws when it comes to bankruptcy, and various chapters (7, 13, "20" - 13 followed by 7). The 2005 federal law does provide for an exemption of $1.283MM for IRAs, unlimited for ERISA plans. Another complexity are the 15 or so states that have tenancy by the entireties.10

When an older individuals are in financial trouble, a bankruptcy attorney might suggest trying to outlast the creditors because almost all assets are protected:

- Often creditors will move on to other, younger targets, and just as importantly;

- For many creditors, the threat of bankruptcy in the future is worse than an actual filing (given the six or seven years that must elapse before filing a second time);

- And medical expenses immediately prior to death are often substantial, so, individuals may want to keep their powder dry.11

Given that older Americans’ assets mostly consist of retirement plan accounts, IRAs, and home equity, I am not really sure why more older individuals are claiming bankruptcy protection given that median net worth and the significant amount of protected assets. I'm no actuary, nor am I a bankruptcy attorney, so, perhaps I don't understand the table.

Finally, note that bankruptcy is intentionally part of our financial system. It allows an individual to discharge debts while retaining protected assets. Bankruptcy exists, in part, to enable us to take risks, attempt to innovate, and grow. Bankruptcy or debt forgiveness has been an accepted concept for thousands of years. And, seldom is it immoral - there is a significant difference when individuals incur debts they intend to pay, but who now cannot make those payments, and those individuals who have no intention of payment.

We need to encourage the academics and policy wonks to be more careful with the data and stop spreading fear about poverty and bankruptcy among older, retired Americans.

1J. Towarnicky, Retirement in America - A Life of Poverty? 6/29/18, Accessed 8/20/18 at: https://www.psca.org/blog_jack_2018_32 See also: J. Towarnicky, Retirement in America - Individual Account Retirement Savings Plans ARE Good Enough! 7/5/18, Accessed 8/20/18 at: https://www.psca.org/blog_jack_2018_33 See also: Andrew Biggs, The Media's Coverage of Retirement Saving Really is Terrible, Forbes 7/2/18, Accessed 8/20/18 https://www.forbes.com/sites/andrewbiggs/2018/07/02/the-medias-coverage-...

2Kaiser Family Foundation, Accessed 8/20/18 at: https://www.kff.org/tag/dual-eligible/

3D. Himmelstein, E. Warren, D. Thorne, S. Wollhandler, Illness and Injury as Contributors to Bankruptcy, 2/9/05, Accessed 8/20/18 at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=664565

4D. Himmelstein, D. Thorne, E. Warren, S. Woolhandler, Medical Bankruptcy in the United States, 2007: Results of a National Study, The American Journal of Medicine, August 2009, Accessed 8/20/18 at: https://www.amjmed.com/article/S0002-9343(09)00404-5/fulltext

5D. Himmelstein, D. Thorne, D. Woolhandler, Medical bankruptcy in Massachusetts: has health reform made a difference? Am J Med. March 2011, Accessed 8/20/18 at: https://www.ncbi.nlm.nih.gov/pubmed/21396505

6Todd J. Zywicki, July 17, 2007 testimony, before the US House of Representatives, Committee on the Judiciary - Hearing on “Working Families in Financial Crisis: Medical Debt and Bankruptcy”, https://www.mercatus.org/publication/written-testimony-medical-debt-and-... , See also: Ning Zhu, "Household Consumption and Personal Bankruptcy", 3/21/08, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=971134 See also: C. Dobkin, A. Finkelstein, R. Kluender, M. Notowidigdo, Myth and Measurement – The Case of Medical Bankruptcies, New England Journal of Medicine, March 2018, Accessed 8/20/18 at: http://economics.mit.edu/files/14892 See also: D. Himmelstein, D. Thorne, S. Woolhandler, Medical Bankruptcy in Massachusetts: Has Health Reform Made a Difference? The American Journal of Medicine, March 2011, Accessed 8/20/18 at: http://www.pnhp.org/sites/default/files/docs/2011/AJM_Mass-Reform-hasnt-...

7D. Thorne, P. Foohey, R. Lawless, K. Porter, Graying of U.S. Bankruptcy: Fallout from Life in a Risk Society8/18/18, Accessed 8/20/18 at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3226574

8N. Adams, Happen ‘Stance’, Napa-net.org, 8/14/18, Accessed 8/20/18 at https://www.napa-net.org/news/managing-a-practice/industry-trends-and-re... , See also: A. Biggs, Does America Face A 'Boom' In Retiree Bankruptcies? 8/10/18, Accessed 8/20/18 at: https://www.forbes.com/sites/andrewbiggs/2018/08/10/does-america-face-a-...

9K. Drum, Just Stop It. The Elderly Are Doing Fine, Mother Jones, 8/6/18, Accessed 8/20/18 at: https://www.motherjones.com/kevin-drum/2018/08/just-stop-it-the-elderly-...

10https://www.nolo.com/legal-encyclopedia/retirement-plan-bankruptcy-chapt... , https://www.nolo.com/legal-encyclopedia/supreme-court-rules-inherited-ir...

11E. French, J. McCauley, M. Aragon, P. Bakx, M. Chalkley, End-Of-Life Medical Spending In Last Twelve Months Of Life Is Lower Than Previously Reported, Health Affairs, July 2017, Accessed 8/20/18 at: https://www.healthaffairs.org/doi/full/10.1377/hlthaff.2017.0174