Advertisement

Narrowing Retirement Savings Gaps

How Eligibility and Vesting Impact Retirement Savings

Historically, workers experienced significant gaps in retirement benefits due to eligibility and vesting provisions. Throughout the past 45 years, those gaps have been significantly reduced by a combination of legislation and plan design changes.

61st Annual Survey Results

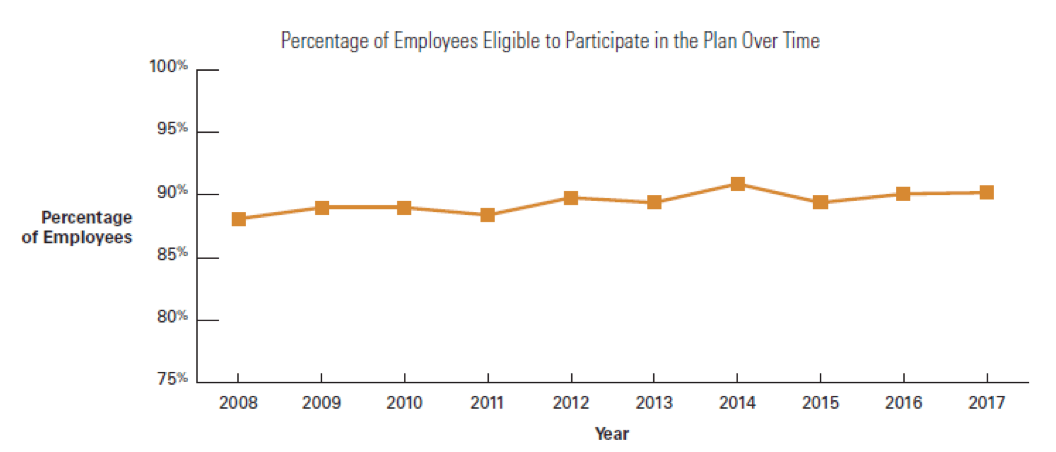

The percentage of employees in an eligible class has remained relatively constant over the past decade.

Twenty years ago, only 40 percent of companies let their employees join their 401(k) plans within three months of hire. Today, 60.1 percent allow employees to start contributing at hire – a 50 percent increase! Many plan sponsors made this change as part of their adoption of automatic enrollment features – as identified in earlier posts.

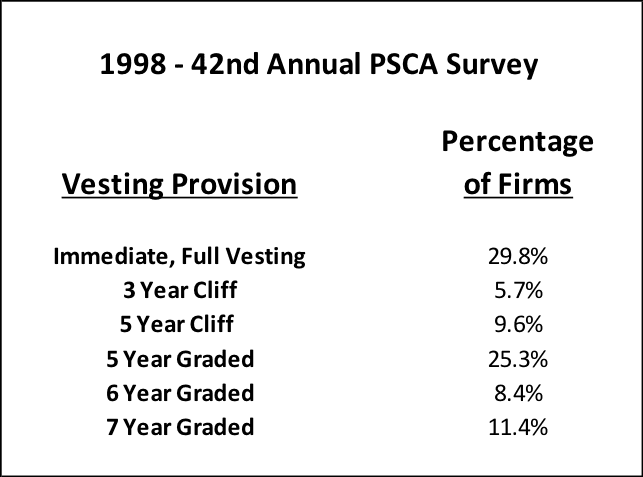

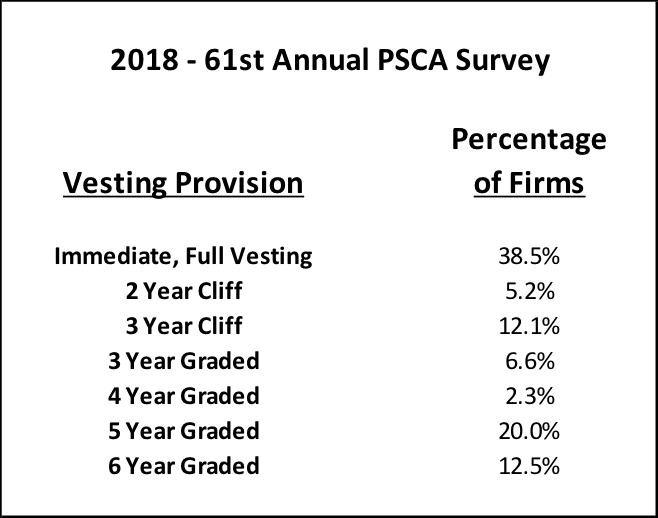

Throughout the past 20 years, the percentage of plans with immediate vesting has increased 29 percent – from 29.8 percent to 38.5 percent. And, the percentage of plans that fully vest workers after three or fewer years of service has increased from 35.5 percent to 62.5 percent – a 76 percent increase!

Prior Legislation

ERISA: Recognizing the twin challenges of funding and vesting, Congress passed the Employee Retirement Income Security Act of 1974 (ERISA)1 that was signed into law by President Ford on Sept. 2, 1974. ERISA required tax-qualified plans to change eligibility provisions to either:

- The later of attaining age 25 and completing one year of service, or

- Completing three years of service (if the participant is 100 percent immediately vested at that time).

ERISA added new vesting requirements for employer contributions – one of three alternatives, either:

- 100 percent vesting upon completion of 10 years of service,

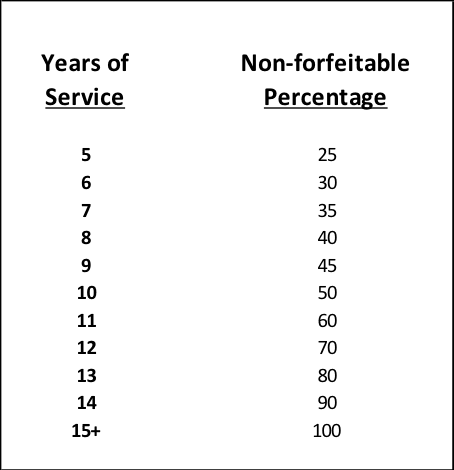

- A graded vesting percentage based on completed years of service:

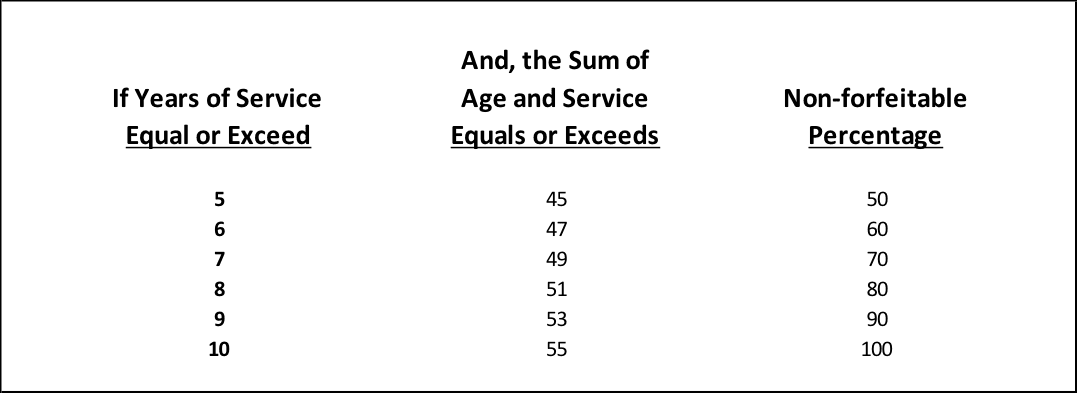

- A graded vesting schedule known as “the rule of 45,” where an employee has completed at least five years of service where the sum of his age and service equals or exceeds 45:

ERISA also applied new vesting rules for breaks in service and for workers who attained normal retirement age.

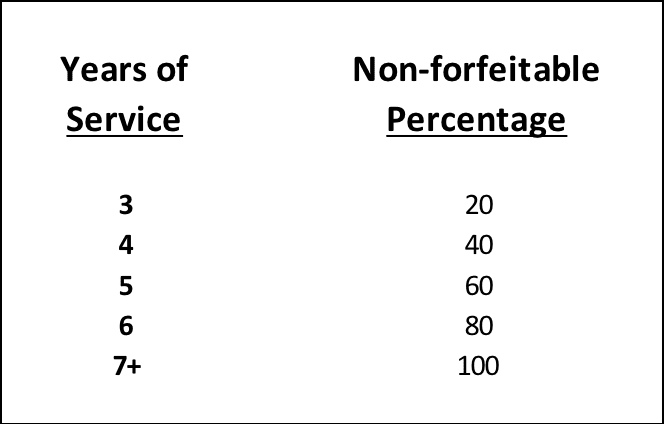

Tax Reform Act of 1986: In 2018, we celebrated the 40th anniversary of the Revenue Act of 19782 which added Internal Revenue Code Section 401(k) (§401(k)). However, it wasn’t until the Tax Reform Act of 1986 (TRA’86)3 when Congress again updated eligibility and vesting requirements regarding §401(k) plans:

- Eligibility: The maximum eligibility service for §401(k) plans was reduced to one year.

- Vesting: One of two rules must be satisfied:

- Five year cliff vesting – 100 percent, or

- Graded vesting:

TRA’86 also eliminated vesting by class year.

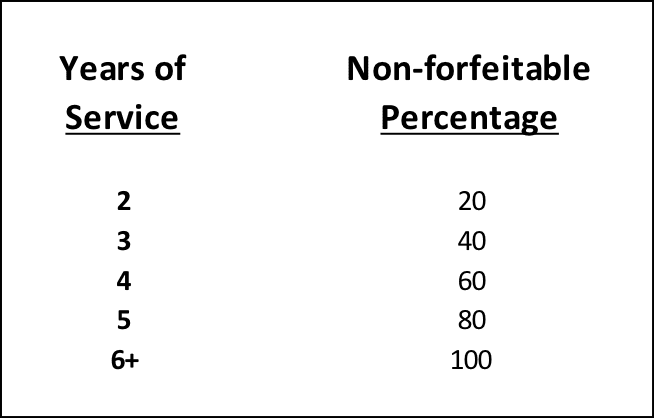

Pension Protection Act of 2006: The Pension Protection Act of 2006,4 further shortened the vesting service requirements for individual account retirement savings plans like the §401(k):

- Vesting: One of two rules must be satisfied:

- Three year cliff vesting – 100 percent, or

- Graded vesting:

Is More Legislative Change Coming, Necessary?

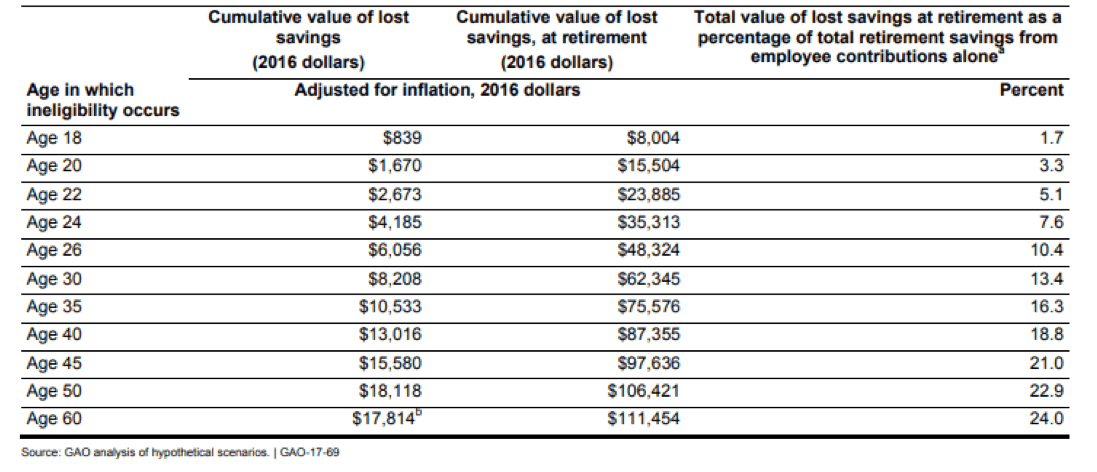

In 2016, the Government Accountability Office (GAO) issued a report that estimated the impact on eligibility and vesting provisions on workers’ retirement savings.5 With respect to the minimum age 21 requirement, they estimated the “lost” savings for two example workers (one with medium earnings and average wage growth, the other with lower earnings and less wage growth) as a decline in lifetime retirement savings of 5 percent and 11.5 percent, respectively:

GAO also estimated the impact of repeatedly applying the one year minimum service requirement for a worker with 11 different employers during a working career – estimating a “lost” savings of $111,454 or 24.0 percent of lifetime retirement savings.

Finally, the GAO study and projections also suggested that vesting policies significantly reduce lifetime retirement savings. They constructed an example where the worker leaves two jobs after two years, at ages 20 and 40, where the plan requires three years for full vesting – estimating that the forfeited employer contributions could be worth $81,743 at retirement (or $22,143 in 2016 dollars).

Here are my thoughts on the GAO study:

- First, one comment was that: "today’s workers may be likely to change jobs frequently." That is just not true; studies show that turnover/tenure has not changed throughout the past five decades.

- Second, vesting's effectiveness has been emasculated by legislative changes. In my last plan sponsor role, I estimated that more than 80 percent of all employer contributions end up benefiting individuals who do not ultimately retire from my employer – those who terminate before reaching retirement age or completing significant service.

- Third, curtailing a plan sponsor’s ability to limit employer contributions to those employed as of the last day of the plan year will raise plan administrative costs (for all who receive allocations after separation).

- Fourth, most worker turnover is voluntary. It is the employee, after considering all factors, who decides to change employers and suffer another eligibility period or forego unvested employer contributions and earnings thereon.

- Fifth, an employer can provide for immediate eligibility. However, age 21 and one year of service eligibility provisions are not a bar to retirement savings in any way as workers can contribute to an IRA.

- Sixth, many plans do provide for immediate eligibility – facilitated by specific nondiscrimination testing provisions.

- Seventh, employers are free to adopt 100 percent immediate vesting if they believed such practices were in their best interests. Obviously, many don't believe that is appropriate with regard to their workforce.

- Eighth, whether a plan uses forfeitures to increase the allocation to workers who remain employed or they use the forfeitures to reduce an employer's future contribution (moderating the cost of the plan), further limits on vesting will likely trigger some other offsetting change or reduction in employer financial support - within the retirement savings plan, in another benefit plan, in direct compensation or some other rewards program.

Bottom line, some would assert that too much employer financial support is already diverted to workers who will not remain with the employer and ultimately retire from the firm. Because plan sponsors have voluntarily adopted eligibility and vesting limits, any new mandates that would increase the portion of rewards allocated to younger, short service workers would be inconsistent with a plan sponsor’s existing rewards strategies and preferences.

1§§202, 203, Pub. L. 93-406, enacted 9/2/74, Accessed 2/19/19 at: https://www.govinfo.gov/content/pkg/STATUTE-88/pdf/STATUTE-88-Pg829.pdf

2§135, Pub. L. 95–600, enacted 11/6/78, Accessed 2/19/19 at: https://www.gpo.gov/fdsys/pkg/STATUTE-92/pdf/STATUTE-92-Pg2763.pdf

3§§1113, 1116, Pub. L. 99-514, enacted 10/22/86, Accessed 2/19/19 at: https://www.govinfo.gov/content/pkg/STATUTE-100/pdf/STATUTE-100-Pg2085.pdf

4§904, Pub. L. 109-280, enacted 8/17/06, Accessed 2/26/19 at: https://www.govinfo.gov/content/pkg/PLAW-109publ280/html/PLAW-109publ280...

5GAO, 401(K) PLANS, Effects of Eligibility and Vesting Policies on Workers' Retirement Savings, GAO 17-69, October 2016, Accessed 2/26/19 at: https://www.gao.gov/assets/690/680568.pdf