Advertisement

Mind the (Coverage) Gap

Today they are your employees. With few exceptions, they had a different employer(s) in the past. And, chances are, most will work somewhere else, someday. So, start minding the coverage gap for all your employees.

In 2016, 64% of workers ages 26 to 64 participated in an employer-sponsored retirement plan either directly or through a spouse.1 So, 36% did not participate in an employer-sponsored plan. That 36% includes some of your current workers, others who worked for you in the past and some future hires.

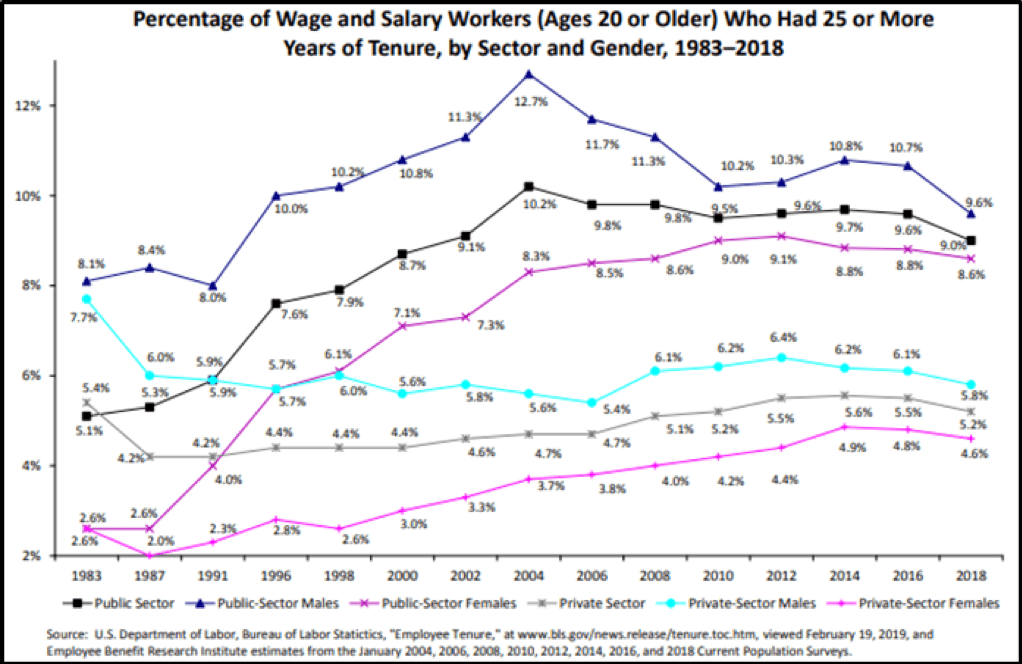

More importantly, less than 5% of your past, current and future workers are or will be “prototypical retirees” – those who complete 25 or more years of service and retire (stop working) upon leaving your firm.2

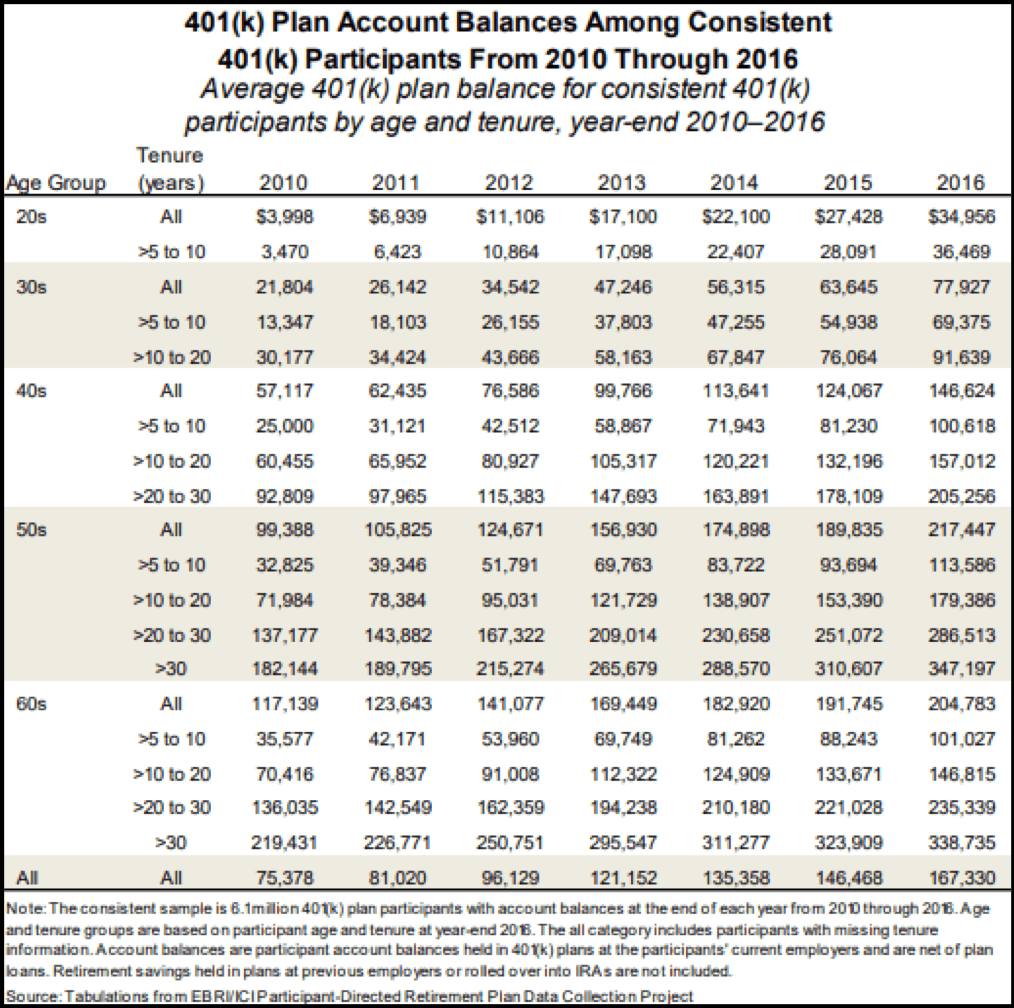

While the past is not predictive of the future, 401(k) plan experience to date shows that participants have successfully prepared for a retirement at “normal” retirement age after saving for 25 or 30 years.3

Out of Sight, Out of Mind?

Obviously, the objectives of your retirement savings plan are not solely focused on helping only those workers who will complete 25+ years of service and separate upon attaining “normal” retirement age. Yet, many, perhaps most plan designs fail to accommodate the needs of those who won’t be “prototypical retirees.” Consider:

- Adding Deemed IRAs (traditional & Roth) so participants can:

o aggregate/consolidate all retirement savings in your plan, and

o contribute to your plan after separation from employment. - Accepting rollovers from:

o other employer-sponsored plans, including assets accumulated by participants who worked elsewhere after leaving your firm, and

o individual Retirement Accounts. - Minimizing leakage from plan loans by:

o adding provisions to encourage post-separation repayment (electronic banking, etc.), and

o facilitating rollover of an outstanding/defaulted loan balance from a prior employer’s plan.4

Mind the coverage gap to achieve a superior result – for all participants.

1Investment Company Institute, Who Participates in Retirement Plans, 2016, Vol. 25, No. 6, August 2019. “… Tabulations of administrative tax data offer an alternative source for retirement plan participation statistics. The need for a more reliable measure of retirement plan participation has increased given recent changes to the survey that provides the most commonly cited statistics on retirement plan participation, the Annual Social and Economic Supplement (ASEC) to the Current Population Survey (CPS). Comparisons with tax data suggest that the ASEC understated the participation rate by about 5 percentage points from 2008 to 2013. Between 2013 and 2016, the difference increased to 18 percentage points following a revision to the survey questionnaire used for the ASEC. …” , Accessed 8/16/19 at: https://www.ici.org/pdf/per25-06.pdf See also: N. Adams, Half a Chance, 8/1/19, Accessed 8/16/19 at: https://asppa-net.org/news/browse-topics/half-chance, and N. Adams, Data ‘Minding’, 10/1/18, Accessed 8/16/19 at: https://www.asppa.org/news/browse-topics/data-%E2%80%98minding%E2%80%99

2C. Copeland, Trends in Employee Tenure, 1983–2018, Employee Benefits Research Institute, 2/28./19. Accessed 8/16/19 at: https://www.ebri.org/docs/default-source/ebri-issue-brief/ebri_ib_474_te...

3J. VanDerhei, S. Holden, L. Alonzo, S. Bass, What Does Consistent Participation in 401(k) Plans Generate? Changes in 401(k) Plan Account Balances, 2010 – 2016, 11/6/18, Accessed 8/16/19 at: https://www.ebri.org/docs/default-source/ebri-issue-brief/ebri_ib_464_lo...

4Examples of a three-step and five-step “loan rollover” process implemented by the author:

• Example 1: The new hire has an account balance in the predecessor employer’s plan of $20,000 of which $8,000 is an outstanding loan. Step #1: Participant rolls over $12,000 to the new employer’s plan. Step #2: Participant takes $8,000 loan from the new employer’s plan. Step #3: Participant uses those loan proceeds to complete rollover of the outstanding loan principal. Participant now has a $20,000 account balance in the new employer’s plan, with an $8,000 outstanding loan balance.

• Example 2: The new hire has an account balance in the predecessor employer’s plan of $30,000 of which $13,000 is an outstanding loan. Step #1: Participant rolls over $17,000 to the new employer’s plan. Step #2: Participant takes a $10,000 loan from the new employer’s plan. Step #3: Participant uses loan proceeds to rollover $10,000 to the new employer’s plan. Step #4: Participant takes a $3,000 loan from the new employer’s plan. Step #5: Participant uses loan proceeds to rollover $3,000 to the new employer’s plan. Participant now has a $30,000 account balance at the new employer’s plan, with a $13,000 outstanding loan balance.