Advertisement

Make Retirement Plans Great Again?

In a recent article which suggests America would be great again if it adopted a number of economic and employment policies prevalent in the 1960’s1, Alan Blinder states that: “Back in the 1950s and 60s, many workers had traditional defined-benefit pension plans (DB plans).” Well, I’m not sure about Mr. Binder’s definition of “many,” but in the timeframe he mentions and well into the 1970s, less than one third of private sector employees worked for an employer that sponsored a DB plan.

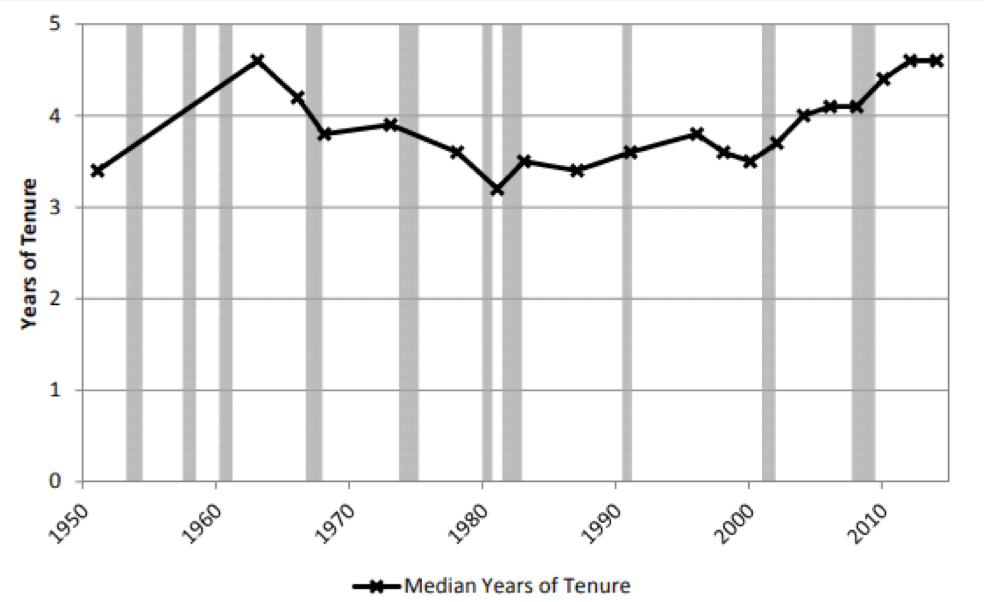

Worse, most workers didn’t become eligible until they met age, service, and eligible class requirements. For example, a number of plans limited participation to workers age 35 or more. Further, most DB benefits were not earned (vested) until a person retired or completed 15 or more years of service. Median tenure has consistently been around five years for workers age 25 – 64 for more than the past four decades.2

Finally, many of those DB plans were inadequately funded. So, even where an employer offered a DB plan, most workers never became eligible, most never vested, and only a small minority actually received a benefit. Perhaps Mr. Blinder forgets all of the Studebaker and Packard workers who did not receive their DB pensions?

Pension promises without funding are mere dreams.

In contrast, all defined contribution (DC) plans are fully funded. And, almost all fully vest employer contributions after less than five years of service. Workers at a growing number of employers are eligible and vested on their hire date. As a result, a supermajority of today’s workers have earned tangible retirement benefits. And, today’s 401(k) plan is nothing like the original 1981 version. It often features automatic enrollment, escalation, and investments – using an age-appropriate, professionally-designed asset allocation.

We have more than 100 million individual retirement savings accounts (401(k), 403(b), 457(b) and IRAs). And, individual account retirement savings (DC) assets have grown 680 fold from less than $25 Billion in 1975 to more than $17 Trillion in 2018!3

It’s one thing to remember the past – it’s another to see it through a rose-colored prism of what one wishes it had been.

1A. Blinder, What if Trump Really Wanted to Make America Great Again? WSJ, 12/4/18. Mr. Blinder is a professor of economics and public affairs at Princeton University and a former vice chairman of the Federal Reserve. Accessed 2/10/18 at: https://www.wsj.com/articles/what-if-trump-really-wanted-to-make-america...

2BLS, DOL, Employee Tenure in 1998, 9/23/98, Accessed 12/10/10 at: https://www.bls.gov/news.release/history/tenure_092498.txt See also: EBRI, Employee Tenure Trends, 1983 – 2016, 9/27/17, Accessed 12/10/18 at: https://www.ebri.org/docs/default-source/ebri-notes/ebri_notes_v38no9_te... See also: H. Hyatt, J. Spletzer, U.S. Census Bureau, The Shifting Job Tenure Distribution, February 2016. See Figure 1. Accessed 12/10/18 at: http://ftp.iza.org/dp9776.pdf

3J. Poterba, S. Venti, The Transition to Personal Accounts and Increasing Retirement Wealth: Macro- and Micro-evidence, NBER, June 2004. See Figure 1.2 Accessed 12/10/18 at: http://www.nber.org/chapters/c10340; See also: ICI, Retirement Assets Total $28.3 Trillion in Second Quarter 2018, 9/27/18, Accessed 12/10/18 at: https://www.ici.org/research/stats/retirement/ret_18_q2