Advertisement

Graded or Fixed? Why is the question.

Sponsored by Allianz Life Insurance Company of North America

There are an infinite number of ways that a company can structure the employer contribution to the retirement plan (ok, not infinite , my math brain is saying there is a finite number out there some where, I just don't know where it is), whether it be a match on employee contributions, a non-matching/profit sharing contribution to all, or both. There are almost as many theories about what is “best” as there are possible formulas, but the decision is a decidedly individual one as the company weighs their corporate philosophy, participant demographics, administrative complexity and resources, and financial capability. We read a lot of theory on this, but I was curious what plan sponsors would tell us was the reasoning for the employer contribution formula, if they knew what it was.

We asked what type of formula (fixed or graded) was used and why. What’s interesting is regardless of the formula, many indicated the reason was fairness for employees, with ease of administration another commonly stated reason. In PSCA data, we consider a formula that is tiered for any reason, including the safe harbor formula of $1 per $1 on the first 3% of pay and $0.50 per $1 on the next 2%), to be a “graded” formula because the contribution has multiple levels to it based on contribution rate, even though it applies to all participants, whereas a fixed formula only has one set formula ($1 per $1 on the first 6% of pay).

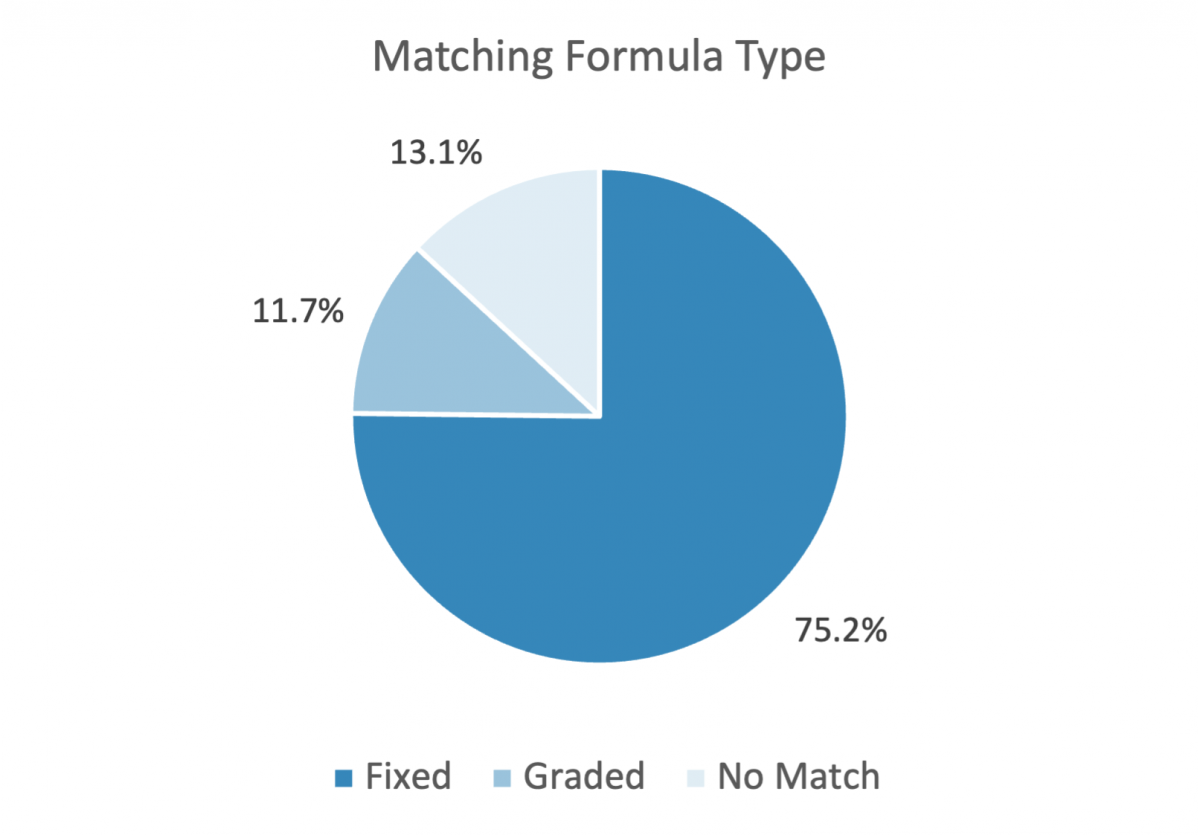

Three-quarters of respondents stated their company provides a “fixed” match, 12 percent a “graded” match, and 13 percent no match (most provide a non-match instead, many a safe harbor 3%). There is no right or wrong answer to this, but the answers are illuminating as to the philosophy and priorities of plan sponsor companies. Select comments follow.

Fixed formulas:

- Able to budget estimated match

- Applying a fixed formula ensures fairness and transparency for everyone regardless of seniority, status or length of service.

- Best for employees

- Compares with our benchmark group, fits within our cost structure, met safe harbor rules.

- Competitive, simple to administer and easy for participants to understand.

- Determined by State Legislature based on budgetary considerations.

- Ease of administration

- Ease of calculation was our main thought.

- Easy to predict, budget for and forecast company cost over time.

- Equitable across all employees

- Fair and equitable

- Fairness for all contributors

- Fairness for everyone. No downside for those who can't afford higher contribution rate to receive a stretch match.

- For our purposes the fixed formula is easier to understand by employees and provides a fair basis for allocation.

- Has been in place. We continue to match all with full vesting.

- It is a fair formula, and it keeps us competitive with other companies.

- It's easier to manage. Everyone is treated the same.

- Less chance of error and fair for all

- Less complexity often means fewer mistakes.

- Offering match and at the same time promoting increased deferral by employee owners as well.

- Our formula encourages employees to spread contributions throughout the year. It also contains a dollar amount cap.

- Our match is .50 on the dollar up to $2,000. This match formula allows everyone to get the same match based on their contributions and not on their compensation. Match based on compensation allows higher paid employees to receive more match even if their contributions are at the same level as lower paid employees (which is not equal for all participants).

- Safe Harbor; equality for all associates

- Simplicity. We review variations of the match formula every year, but always seem to go back to the fixed.

- The goal was to encourage a total, baseline savings rate of 14.5% of pay (i.e., total of employee deferrals and employer contributions). The fixed formula has been highly effective in achieving that goal within the parameters of our corporate budget.

- The more you contribute, the more you get in match

- This fixed formula was chosen to maintain consistency for all employees.

- This was administratively the easiest to track.

- To increase participation - we had 100% match up to 3% and so the 50% up to 6% has prompted our employees to increase their contribution levels.

- To qualify for Safe Harbor protection.

- Unfortunately, I do not know why this formula was chosen.

- unsure

- Very old plan. This is legacy criteria and it is set up according to what was most popular at the time.

- Wanted to be equitable for all.

- We chose a fixed, it is easy to calculate and to communicate.

- We did the most we could afford while remaining compliant with the Safe Harbor Plan design.

- We do have varying formula for various unions based on union contracts, but all non-union employees have same formula.

- We felt fixed was more equitable for the employees. Additionally, this is the most administratively friendly option for our HR/PR teams.

- We have both matching contributions as well as a non-matching contribution - seemed reasonable to incent savings to have matching.

- We match a fixed amount but the match occurs within our ESOP. We match up to 4% but depending on the company's performance, we may provide a higher percentage.

- We use a discretionary match, but each year it has been the same for everyone. We believe this is the fairest solution and it encourages employees to save at least 6% to maximize the match. It has worked well to keep our ADP/ACP tests in compliance with a 95% participation rate!

- We use a Safe Harbor 4% match. We would not pass testing without SH and we do not have the budget for auto enroll.

- We wanted to reward our employees for saving

- We're a Safe Harbor plan with automatic enrollment so the QACA design and match formula was chosen to ensure Safe Harbor compliance.

- When we first established a 401(k) from the formerly trustee managed profit-sharing plan, we were informed that a $1 match on the first 3% was safe-harbor. We didn't feel this was enough savings and chose to incent participants with $1 on first 3% and $0.50 per dollar on the next 4% and 5% and set the default contribution rate to 5%. The 5% did not dissuade participants and we try to automate all participation activity we can to use the positive power of inertia to our participants' advantage.

Graded:

- 100% of first three percent contributed; 50% of 4th & 50% of 5th percent. This satisfies Safe Harbor Plan rules.

- Non-Pension Eligible: 100% of the first 5% plus 3-7% based on Age+Service; Pension Eligible: 50% of the first 6.5%

- Safe harbor formula - 100% on the first 2% and 50% on the next 4% for a 4% match on a 6% contribution and vested in two years.

- To award longevity

- To encourage employees to save more

- To encourage higher levels of contribution

- To encourage retention and long-term relationship

- X% for 0-14 years of service; Y% for 15 years or more

Non-matching contribtuion only:

- Safe Harbor and ensures all individuals are accumulating assets for retirement.

- Administrative ease

- Recruitment. We provide an 11% of compensation contribution after 1 year of service

- The company wants to contribute to employee retirement even if employees do not participate.

- We are a very small company with a safe harbor plan

- We hire a lot of younger individuals that historically have not prioritized saving for retirement. By providing an automatic company contribution that is not tied to their personal contribution, we hoped to get their "nest egg" started for them even if they were not able to contribute at this time.

- Compliance testing

- Meet all testing requirements.

- We provide a Safe Harbor contribution and a Discretionary contribution.

- We provide a 3% safe harbor contribution exempting non-discrimination testing.

- We contribute 3% of gross income, regardless of employee participation

- Safe Harbor Non-elective contribution

- We have a profit sharing plan.