Advertisement

Growing Retirement Savings Gap: Impact of Income and Race on Older Workers

A recent Government Accountability Office (GAO) report examines the disparities between retirement accounts of older workers in low-income and high-income brackets. The findings suggest that federal tax incentives may not benefit the broader demographic as intended.

Key Findings:

Key Findings:

- Growing Disparities Over Time: The gap in retirement savings between low and high-income households (aged 51-64) grew from 2007 to 2019. Only one in 10 low-income households had retirement savings in 2019, down from one in five in 2007. Meanwhile, nine in 10 high-income households had a retirement account balance consistently from 2007 to 2019.

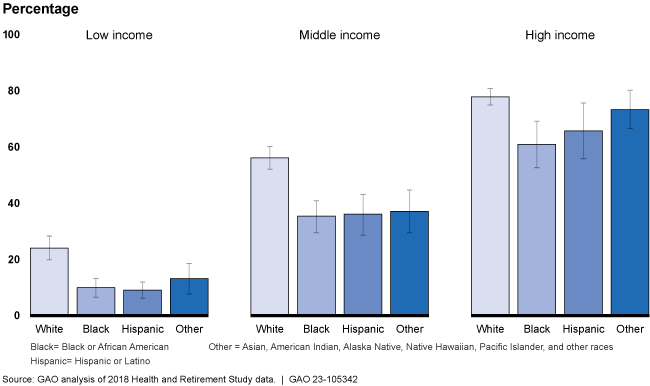

- Racial Differences: White households lead other racial groups in retirement account balances. They have both a higher percentage with balances and about twice the median balance of households of other races.

- Factors Influencing Disparities: The main factors driving disparities in retirement savings are income, job-related factors, and race. High-income households saved a larger portion of their income and received bigger employer contributions. Both education and job tenure had roles. Worryingly, non-White households and households with children had notably smaller balances — around 28% and 20% less, respectively.

- Effectiveness of Retirement Saving Strategies: Strategies to enhance workplace retirement savings vary in effectiveness by income group. Although automatic enrollment may increase the participation of low-income older workers, only a small portion of this group has access to a workplace retirement account. On the other hand, raising the contribution limits mainly benefits high-income workers.

Why This Matters:

The implications are significant. In 2022, tax incentives encouraging workers to put money in tax-preferred retirement accounts led to an estimated $200 billion revenue shortfall for the federal government. As concerns mount that these incentives might favor the wealthy, it's vital to understand the distribution of retirement savings across income brackets.

Conclusion:

Data indicates disadvantages for a significant number of older workers, especially those in the low-income category and those from non-White backgrounds. Addressing these issues will demand a united effort from policymakers, financial institutions, and the wider community.

The GAO's study on retirement savings disparities is concerning. Understanding the distribution of retirement account balances can shed light on the retirement stability of households across different income brackets.