Advertisement

Limiting Loans and HSW Money Sources

Sponsored by: MFS Investment Management

How much access plans allow to retirement assets during employment through loans and hardships is variable and sponsors are often trying to strike a balance between allowing access in emergencies and preserving assets for retirement. Knowing that they can access their money during emergencies can often help employees be more willing to save for retirement. For plans that allow loans, some limit the criteria under which participants can access a loan, some limit the number of loans allowed, some limit the dollar amount. But what about limiting the money sources for loans and hardships? Plans can limit it to participant contributions only, or participant contributions and vested amounts, or they can allow access to all money sources. This is not a question we have asked before so we asked members in last weeks QOTW.

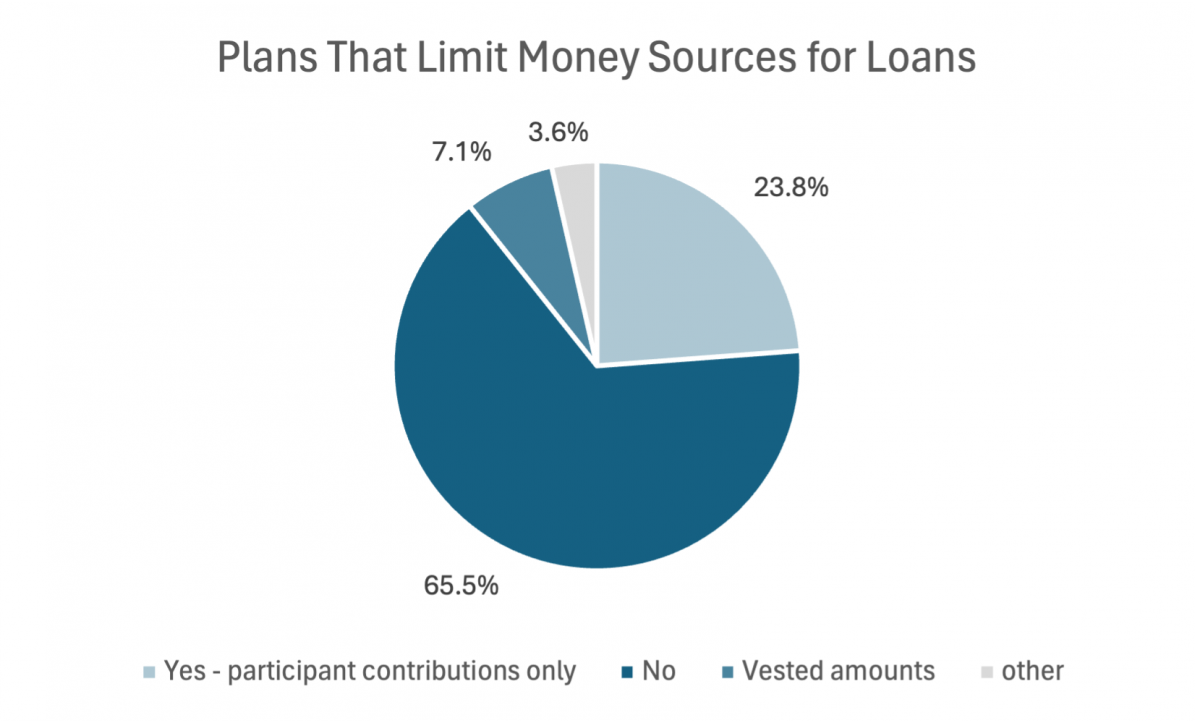

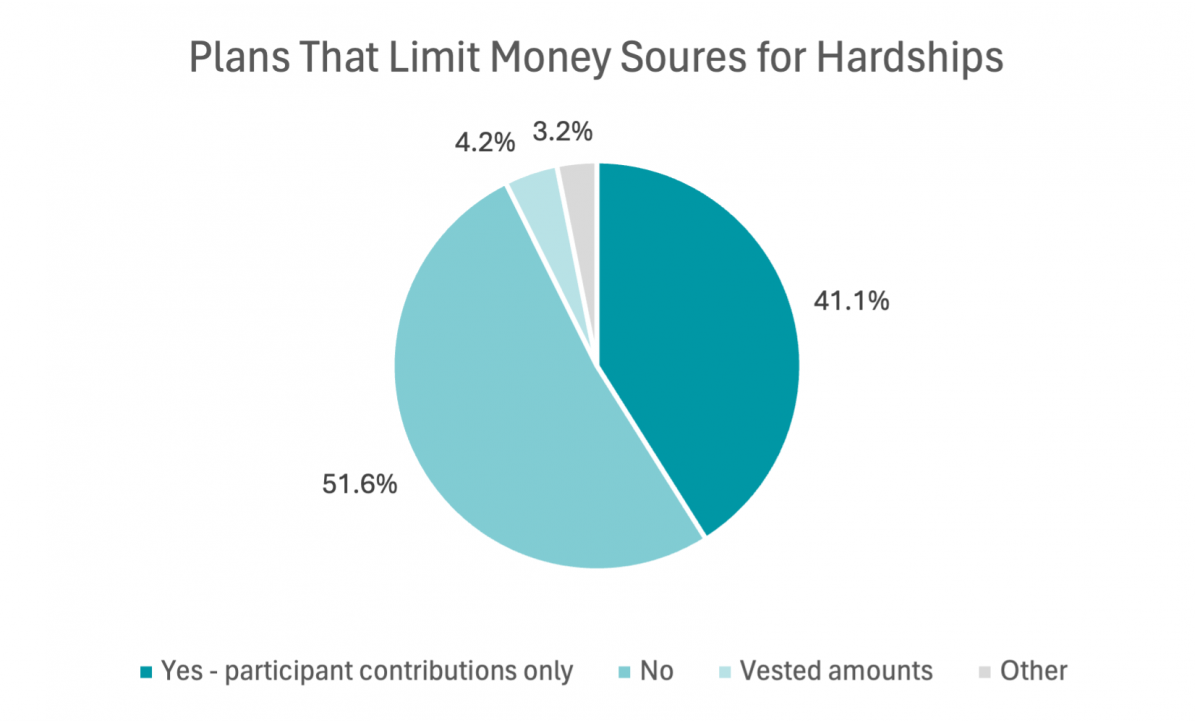

A third of plans do limit money sources for loans – 24% limit them to participant contributions only, while seven percent limit it to vested amounts only, and three percent have other limitations. More plans limit hardships to participants contributions only – 41 percent, with four percent limiting it to vested amounts and three percent with other limitations.

Comments follow.

- All vested balances are available

- As long as the participants are vested, they have access to all sources.

- Can take up to 50% of total vested balance with a max of 2 loans at a time.

- Funds are taken pro-rata from account balance.

- I did not know that was an option. However, we have had employees tell us they were going to quit to get full access to their 401(k) knowing they would be heavily penalized for cashing it out early, but when someone needs money they need money.

- Keeping it simple and providing some future financial security to our employees, as the plan is intended to do. Win-win. [Participant contributions only].

- Our employee contributions and employer contributions are in two separate plans; we only allow loans from the plan with employee contributions. We do not allow hardship distributions at all.

- Our plan does not, but I would love to consider this limitation.

- Participants are able to take loans and hardships from all vested sources; however, we have seen an exponential increase in hardship withdrawals since the 2019 changes that removed the waiting period for contributions after taking one, so we recently limited the number of hardships available per year.

- they are fully vested once they start contributing, so we don't limit the money sources.

- This has not always been the case [Participant contributions only]. Plan bleed was pretty high, but has been reduced since moving to EE contributions in November 2022

- Trying to find that balance of helping people through crisis and preserving retirement resources. [participant contributions and a % of vested with a cap]

- We allow hardships to be taken from 401(k) Pre-Tax and 401(k) Roth Employee Contribution sources.

- We do not have loans as a provision with our plan. However, we do allow for hardship withdrawals. The money sources for hardship withdrawals is limited to participant contributions and the vested portion of their employer provided profit sharing balance. They are not able to take hardship withdrawals from the employer Safe Harbor contributions.

Loan limitation comments:

- In this order: after tax, AT rollovers, Roth rollovers, pretax rollovers, vested employer contributions, in-plan conversions not subject to restrictions, restricted in-plan conversions, pretax, pretax catch-up, Roth, Roth catch-up, QNECs.

- Loans not allowed on Roth deferrals and earnings

- Participant's Vested Account

- Roth contributions are not allowed for loans

- Vested amounts only

- Vested balances, if applicable. Then only participant contributions if not vested.

Hardship limitation comments:

- ppt 401k contributions & ER profit sharing contributions are avail for h/s. ER 401k contributions are not.

- Only allow Pre-tax, Roth and/or QNEC contributions for hardships

- Participant's Vested Account

- Vested balances, if applicable. Then only participant contributions if not vested.