Advertisement

Plan Priorities and Pain Points

This quarter sponsored by: Nuveen, a TIAA company

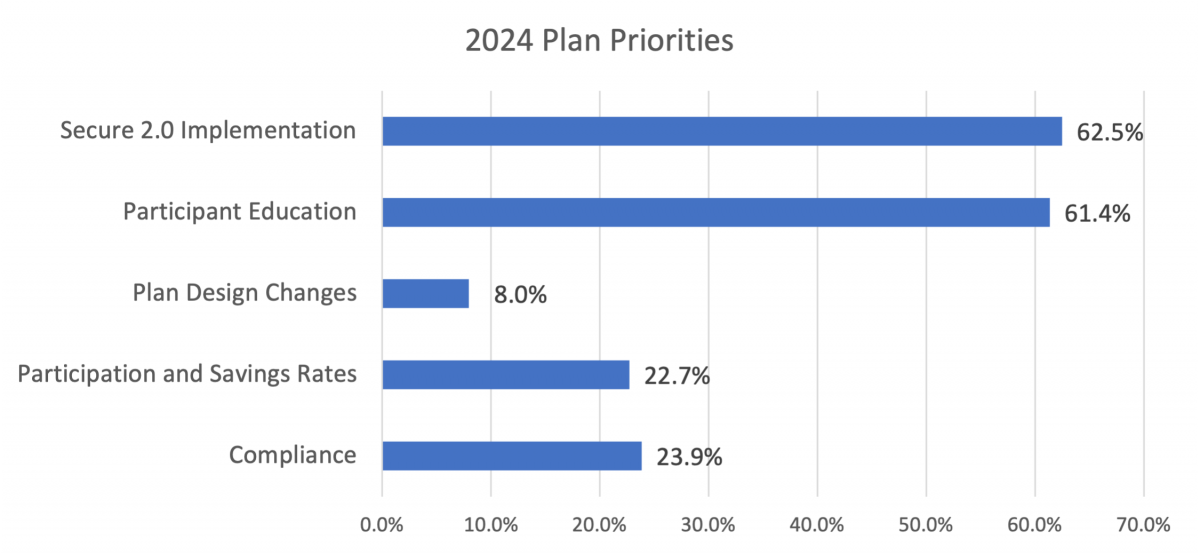

As we look ahead to next year, we asked plan sponsors what their plan priorities are for 2024, their expected pain points, and how PSCA can help.

Though the most pressing of SECURE 2.0 provisions has been delayed for two years, bringing a collective sigh of relief from the industry, implementation of SECURE 2.0 provisions remains a top priority for nearly two thirds of plan sponsors. More than 60 percent are also focused on educating their participants about plan features and looking for ways to engage their participants. About a third of respondents are focused on compliance concerns and increasing participation and/or deferral rates.

Anticipated plan administration pain points generally line up with priorities:

- Evaluating Optional SECURE Provisions

- Compliance/testing

- Increasing participation/deferral rates

- Participant education

Resources plan sponsors would like to see PSCA offer to support them next year included continued webinar, conference topics, and communications related to SECURE 2.0 as well as handouts and participant education materials they can use easily and quickly with employees (you may want to visit the 401(k) Day page and the 401(k) Tool(k)it for some resources currently available). Comments on pain points and resources follow.

Anticipated 2024 pain points:

- Adapting to changes, trying to increase participation and education.

- Auto enrollment and encouraging our employees to participate in our 401k

- Company discretionary match

- Compliance concerns

- Compliance testing

- Compliance, being sure employees know options.

- Current concern is the high utilization of loans. Future (and current) concern is the low contribution rates of our hourly employees.

- Current integrations are not efficient when it comes to capturing new hires and terminations.

- Deciding which ones to roll out [SECURE Act provisions]

- Eligibility changes and more education for existing and new enrollees to increase participation.

- Employees do not understand the importance of putting money away for retirement, or preparing their household for the financial impact retirement can have on their household finances.

- Employees don't seem to retain knowledge of what the plan features are and how to utilize them in a retirement savings strategy.

- Employer education/compliance with the Age 50 Roth CU provision.

- Ensuring appropriate updates to our plan for the latest legislated plan changes.

- Ensuring that we are correctly implementing SECURE 2.0 policies

- Fund selection & expense ratios

- Gather materials to distribute to all eligible participants

- Getting auto enroll and auto escalation started.

- I would like to get more participation into our plan by educating our employees on the plan and features of it.

- Increased participation

- Keeping up with compliance and changing plan rules

- Low deferral rates

- low participation rate among hourly work force

- None at this time (since Section 603 was delayed)

- Participants not engaging in educational materials.

- SECURE 2.0 implementation

- Secure 2.0 may not be priority as some of the Sections have been delayed and we plan to delay as well. We plan on implementing in-plan conversion to replace treatment of employer contributions as ROTH as it achieves the same thing without the complexities.

- Testing

- the new Roth provision for catchup, hoping our payroll software will come up with a solution

- To increase company match

- To increase participation of employees

- Too many regulation changes

- TPA transition, same TPA, but they were purchased

- Training the plan admin on SECURE 2.0 so they can critically evaluate the recommendations offered by our recordkeeper and TPA

- We are just getting ready to sit down with legal to wade thru what has to be done and what optionally could be done.

- We recently acquired 2 companies and lower participation in those two plans is bringing our overall participation rates down. Don't want this to be an issue for our HCE's and non-discrimination testing.

- Would like to see our team defer a higher percentage

Desired PSCA resources:

- A free webinar to send to our employees to help them understand the importance of proper planning for retirement.

- Checklist of all items, of what is required versus optional, and or pro/cons of when it is the plan sponsors choice.

- Clear, concise guidelines would be so helpful! Plus workshops at the 2024 PSCA Conference would be great! Thanks, PSCA!

- Continue to provide relevant information

- Continued topics presentation/education on required changes (which you have been providing).

- Create handouts to distribute.

- Educational materials

- how are HRIS/payroll services working on programming (specifically the Roth CU issue)

- I think PSCA is already tackling this with webinars and articles about the upcoming changes.

- Ideas to spark retirement saving interest

- Keeping us the community updated on any changes or clarification is important.

- less strict compliance testing

- More Resources/Education on understanding investment (Fund selection, fund class identification, etc.)

- Our Third Party Administrator is very good at providing education resources (documents and in-person meetings).

- Participant education materials

- Perhaps some engaging flyers or information sheets.

- The information, especially consolidated calendars of bullet points for things upcoming has been helpful.

If any of these suggestions resonate with you or you have additional suggestions, send them to [email protected].