Advertisement

QOTW: Lifetime Income Safe Harbor

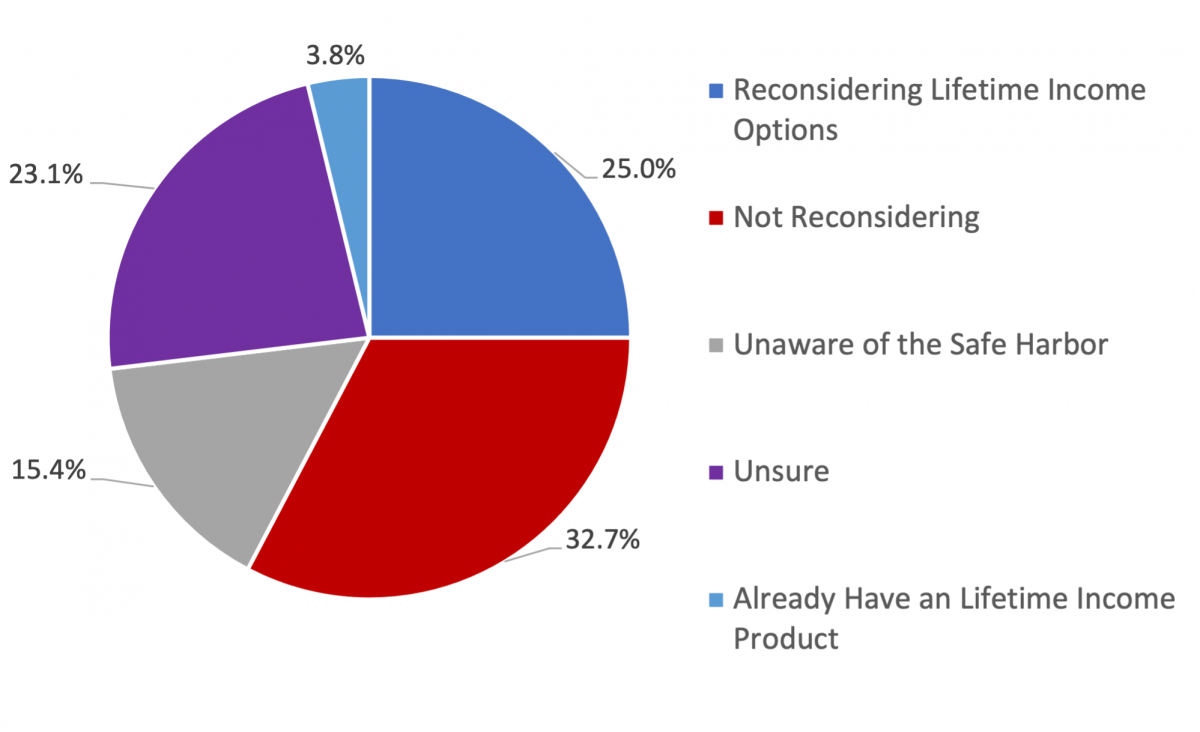

Lifetime income options in retirement plans continue to be a “hot topic” in the industry, but plan sponsors are still hesitant to add them, and uptake remains low. This week we asked members if the Safe Harbor provision in the SECURE Act regarding selection of a Lifetime Income provider has prompted them to reconsider adding a lifetime income option to their plan.

A quarter of respondents indicated that they are currently reconsidering lifetime income options, though a nearly a third are not, 15.1 percent are unaware of the safe harbor provision, and nearly a quarter of respondents are unsure. Comments from sponsors follow.

Those reconsidering:

- It is a growing interest to provide stable income over time.

- This is now on my 2022 list to dive deeper into.

- We have been evaluating this topic for months and will recommend options to our committee before year end.

- Will need to add features to plan for different types of distributions for retirees.

- With an open pension plan, we do not feel this product is appropriate for our population at this time. However, if the pension were to close, having this safe harbor in place makes the decision easier.

Those not reconsidering:

- (still) too complicated, too expensive, too risky.

- Concerned about the additional Plan Sponsor and Fiduciary risks that selection, monitoring and education of an annuity investment option would include.

- Our defined contribution plan is a voluntary supplemental plan to a mandatory defined benefit plan.

- We are offering a partial withdrawal and recurring payment option for terms/retirees starting next year where they can "mimic" the impact of a monthly payment similar to an annuity without losing out on commissions or fees from a financial planner.

- Worried about potential liability.

Other comments:

- Along the lines of annuity, generally not a good option.

- Question has prompted me to research this option a little more

- It sounds like a good option but still too new to consider. Would need more education and research.

- We discussed the possibility earlier this year, but we feel it is a little too soon and we are uncertain at this point if it is something that our retiring participants want.

- We have not yet discussed it.

- We haven't made it a priority to review at this time.

- While I like the idea of adding a lifetime income product, there are a number of factors that need to be worked out prior to adding to the investment lineup. Cost, education and portability are a few topics that come to mind.

0 Comments

Discussion Policy

Sign In to Comment