Advertisement

QOTW: Managed Accounts

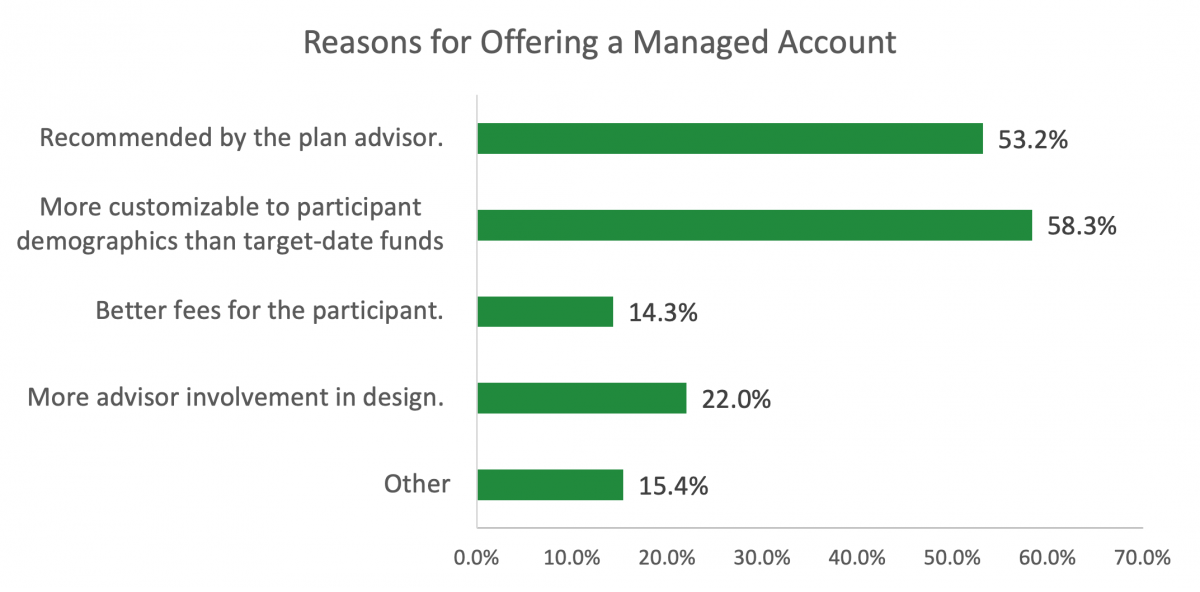

More than half (54 percent) of respondents said they offer a managed account solution to participants. That is significantly higher than the 43.6 percent of plans that indicated they provide one in our 64th Annual Survey. It will be interesting to see if that percentage increases when the 65th Annual Survey is published later this year. The most commonly cited reason for offering a managed account was that they are more customizable to participant demographics (58.3 percent of respondents), followed by “it was recommended by the advisor.” No plans chose it because they prefer the collective fund platform.

Comments from respondents were split, but seemed generally more favorable of including a managed account in a retirement plan lineup than the split responses in a similar poll of retirement plan advisors from PSCA sister organization NAPA.

Comments from plans that offer a managed account:

- Believe this type of account meets the participant where they are and is dependent upon the amount of risk they are willing to take on regardless of their age.

- Certain participants like to take advantage of investing in additional funds beyond our plan offerings.

- Critical to meet the needs of participants with a broad understanding of investing and plans. Also, those who want to make their own choices rather than the Target-Based Funds.

- Excellent options for the more sophisticated investor - full choices

- Extremely worried that there is quid pro quo on these and that this is the next opioid crisis

- For those that do not want to worry about their 401k plan this is a good option.

- I think they are a good option for people who might be late to the game of retirement savings because a TDF is not going to help them reach their retirement goal. The TDF will be too conservative for their age group. With a managed account there is someone who can guide you into more aggressive yet not too aggressive funds that may get them closer to their retirement goal.

- It's great for those with little investment savvy or experience and/or those who just want someone else to manage their account holdings. We offer it for an additional fee, but managed account users hold about 1/4 of the plan assets.

- On the recordkeeping platform it is an option besides choosing a target date fund or choosing your own investments so it just another option for participants who want to pay for investment advice/management.

- Provides an additional choice to participants that would like additional assistance with selecting from available fund choices.

- They can be quite beneficial to participants. The data I've seen proves that typically the participant balance outcome is more favorable than a Target Date fund or their own investment selections over a long enough period of time. Our plan offers them, but managed account isn't the QDIA so engaging our participants to partake has been a struggle, even though it is free to them!

- They could be valuable if the fund lineup is robust enough. If the fund lineup is simple, then managed account, IMO, is not of value for a ptpt - especially if there's a TDF available.

- Though these are often positioned as more customized to the individual, ours are really not - more a risk-based allocation. Harder to explain and benchmark. And, while not currently more expensive, I think a target-date set would work just as well.

- Very lightly utilized by our participants, but we have it in case they want the option.

- We believe in giving participants the opportunity to have their funds professionally managed within the Plan. There are two ways they can do this - (1) Advice (free of charge) - which tells the participant what the manager would suggest and then the participant executes themselves, and (2) Professional Management (for a fee) - which allows them to put the Advice on auto-pilot and rebalances once a month.

- We offer a brokerage link to make other investment options available that are not included in core line-up. We exclude our common stock, penny stocks and UBIT investments from the brokerage link.

- We offer target retirement date funds for people to use as a 'managed account' but we also offer both digital and personal advice services for people who want broader investments but need the advice to have the right investment mix.

- While it's not required, it's nice to provide the option for those employees who would like to engage additional help.

Comments from plans that do not offer a managed account:

- Could be helpful in retaining assets for some employees.

- Given the somewhat typical lack of financial acumen many employees have, this is a risky option that could fall back on the company.

- Has access to the Plan Financial Advisor for financial advice and investment allocations.

- I personally would like to see it but we make most decisions for the masses and don't feel it fits in with our plan at this time.

- In my experience a 'managed account' option in a 401k plan generally is used by the highly-comped employees, and not by the non-HCEs. And, at my last company with over 10,000 employees, only a handful used the managed account option. In my current company, with far fewer employees, the ones who would be inclined to use a managed account option, already have financial advisers outside of the 401k plan.

- It has not been requested by participants and our 3(21) advisors have not suggested it.

- It is not something that participants are ready for without education.

- It's coming under discussion.

- Looking into this.

- Ours is a governmental plan, and it supplements a mandatory defined benefit plan. Managed accounts isn't a priority for us at this time, and participants haven't been asking for them.

- Ours is a governmental plan. Managed accounts would add cost for participants. Participants haven't expressed interest in managed accounts.

- They are a great saving vehicle for employees who understand them and retirement goals.

- They are a nice idea but can be costly to the member. Between the QDIA and target date or other similar types of funds, most members will be in good shape. In the past with managed accounts, I have heard it recommended for an employee to sign up for the first quarter then drop it and sign up once each year to get their accounts updated.

- They are generally oversold and the "customization" element of them doesn't materially impact the asset allocation for most American workers who do not input spousal and/or external accounts. Don't let (perceived) perfection be the enemy of good (at 3-10x the cost).

- Too expensive.

- Typically, low utilization, however, I believe they are another tool in the toolbox and can be beneficial for some participants. Fees have come down recently, so that's a good thing too.

- We are considering a product through Morningstar that will provide advice in which the participant has to take action (for free) or a managed account option if they should choose.

- We do have a 3(38) partner to manage the investments of the overall plan but at this time we do not have managed account options for individual participants.

- We reviewed various managed account offerings and our committee decided not to offer this option in our 401k plan.

- We would have to educate our participants more to have this option.