Advertisement

QOTW: Sidecar Accounts

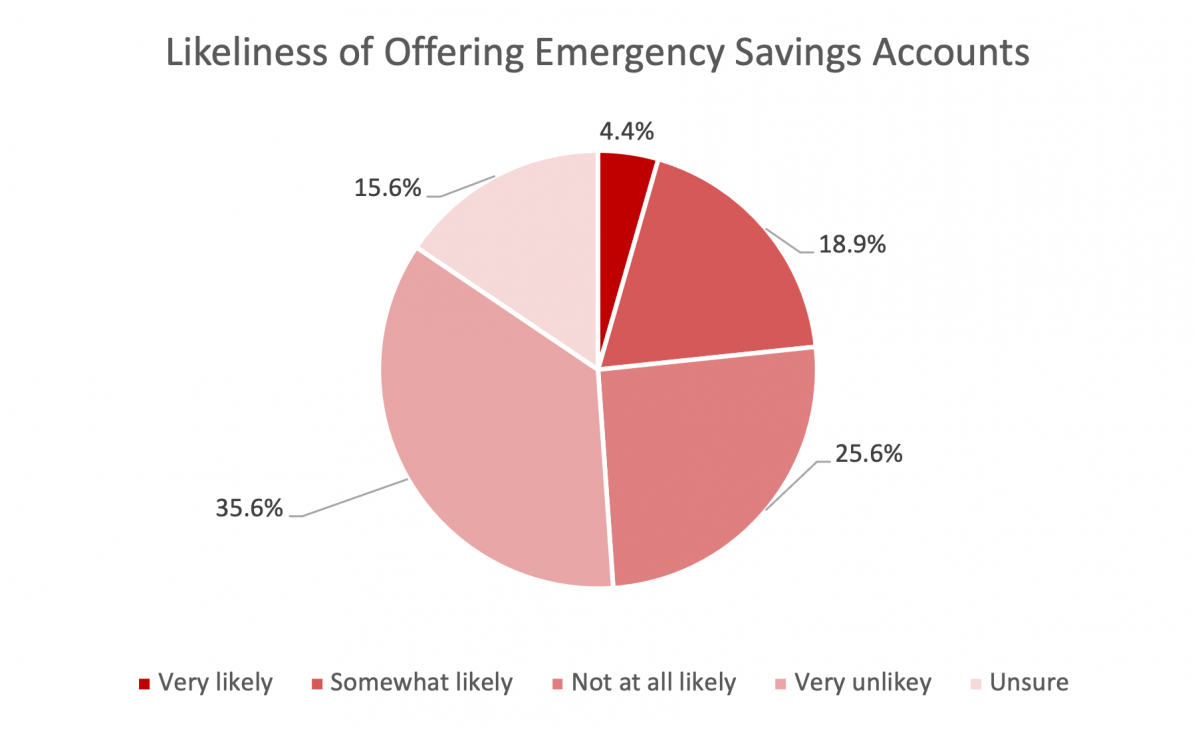

A few weeks back we mentioned legislation that would permit the establishment of emergency savings “sidecar” accounts that would, if established, require that those emergency savings contributions (which could be withdrawn for any purpose with no penalty or restriction) be matched. Under this legislation, the Rise and Shine Act – now passed out of the Senate Health, Education, Labor and Pensions (HELP) committee for consideration by the full Senate, employers choosing to offer these emergency savings side-car accounts would be required to match the emergency savings contributions following the same matching contribution formula that applies to traditional 401(k) contributions. This week we asked members how likely their organizations would be to adopt such a provision if it is passed. Only four percent of respondents stated their organization is very likely to adopt the provision, with 61 percent stating their organization is very unlikely or not at all likely to adopt it.

Comments included:

- Amazing idea - great opportunity

- [Not at all likely] At least at first, we might eventually offer as we have been considering Emergency Savings, but the programming changes to our payroll system calculating the match would be too time consuming to be an early adopter

- Do not want the additional match burden.

- Does this mean in the 401(k) plan? We are VERY unlikely to do so, in that case. But, if they mean 'out of plan' as a standalone ESA, we are very likely to do so.

- Emergency savings has not yet been discussed, but given the focus on retirement readiness, I suspect this would not be offered. The match requirement could be a significant deterrent to offering an emergency savings account.

- Given that organizations have a limited budget, employees are likely to have to make decisions in the future on where to spend their employer dollars.

- I can support this, but not as it is now. There is too much "free" money and with immediate access. I don't think employees would actually use these accounts to save.

- I hope not. The intent of a retirement plan is to save for retirement. Funds can be withdrawn but only in critical situations. Our plan already offers loans for any reason up to 50% of the account balance. Loans require repayment which in turn protects retirement balances. The Side Car concept will divert employee contributions away from traditional 401(k) and encourage (by pointing out the availability) reducing funds available when they retire.

- I like the idea, but not the match requirement.

- Not having seen the formal version details yet, I would still say that we'd rather make changes that were more positively impactful on participant retirement success. There's not enough real data out there on how this impacts savings in the K and how often it is tapped before 59 1/2. I'm assuming it would still have a penalty? In any case, we'd rather look at options like matching student loan payments than something like this. There's nothing stopping a participant from opening a bank savings account if they sincerely want to save for emergencies.

- Not sure this will get more people involved however. It will just increase the savings of those already participating

- Our committee has been intrigued with idea of offering a savings account within our retirement plan. I don't know how our committee would react to a mandatory match on these 'sidecar' savings accounts.

- Our company believes in caring for the individuals in need of assistance, so I believe it is likely they would offer this.

- Our company has been researching out emergency saving plans.

- Our intention is to boost retirement savings not emergency savings and we do offer hardship withdrawals, 59 1/2 in-service withdrawals and loans already.

- Perhaps, we are always looking for ways to support our employees.

- The employer requirement is a deal-breaker and there is already hardship rules in place

- the employer shouldn't be required to match for a fund intended for non-work related issues.

- This legislation could have a significant negative impact on retirement savings account balances---leaving employees unable to retire.

- This question draws attention to how woefully unprepared and irresponsible people are. People spend and borrow and don't save in an emergency fund, then expect others (parents or the government) to bail them out. We are in bad shape as a country.

- This would be useful benefit to keep employees from raiding their 401k accounts.

- We are a small business trying to survive through all the horrible government decisions that are causing skyrocketing inflation. No Way can our business afford to do this. AND, right now, it is unlikely anyone would participate. People are struggling to keep gas in their cars and food on the tables.

- we currently don't match

- We don’t offer a match in our 403b, so I don’t see us adding this to our plan if it is based on a matching contribution

- We have 96-98% participation in our plan. I wouldn't want to do something to erode that figure.

- We have been discussing how to encourage employees to save to reduce the amount of loans taken from the Savings Plan, however I do not believe there would be an appetite to set up this particular type of account if matching with the same formula was mandatory. It seems this design would encourage abuse and would be counterproductive to its stated cause. Plan Sponsors should have the autonomy to decide if a match is appropriate for that vehicle and how much to match if so - that decision would need to be considered as part of a holistic approach to the overall benefits package.

- We have discussed it and are leaning towards not offering if passed

- We offer a safe harbor plan with no match.

- We want to emphasize HSA savings and 401(k), and its hard to ask employee's to put $ in so many different funds.

- We want to encourage any savings habits that we can among employees as long as our efforts to track and manage this benefit are not excessive.

- We will monitor what other employer's do to determine the value in offering this plan

- We would take a wait and see approach from what other plan's were doing and what our providers system capabilities were

- Where's the accountability? People get a paycheck, they can put some of it directly into a savings account. If we start providing a matched opportunity for savings, what is there impetus for saving? They get free money and they get to use theirs when they want. If we set it up for them to save, should we also set up automatic mortgage payments? credit card payments? when does it stop and people become accountable for their financial lives. BEST... educate early and often starting in elementary school. At work offer financial coaching, budgeting classes, etc. Offer a credit union account. Help them set up their paycheck to deposit directly into multiple accounts. We give them a match so they can have more towards their retirement that they save for that purpose.

- While only about half of our employees defer to max our match, perhaps some would increase their deferral if they knew the side car money could be withdrawn for any purpose with no penalty or restriction.

- While we have been looking for ways to encourage emergency savings, if the requirement was to match at 401(k) rates we would just add more money to our 401(k). We do provide funds not dependent on the employee contribution, it is unclear if the proposal would require that and what if any tax incentives would be available, too many unknowns to give a really good answer as to our interest.

- with so many using their 401k account as a savings accounting it would not be prudent for our workforce or our plan

- Would the employee be responsible for taxes on the match? We already make short term loans to our employees.