Advertisement

QOTW: Small Distributions

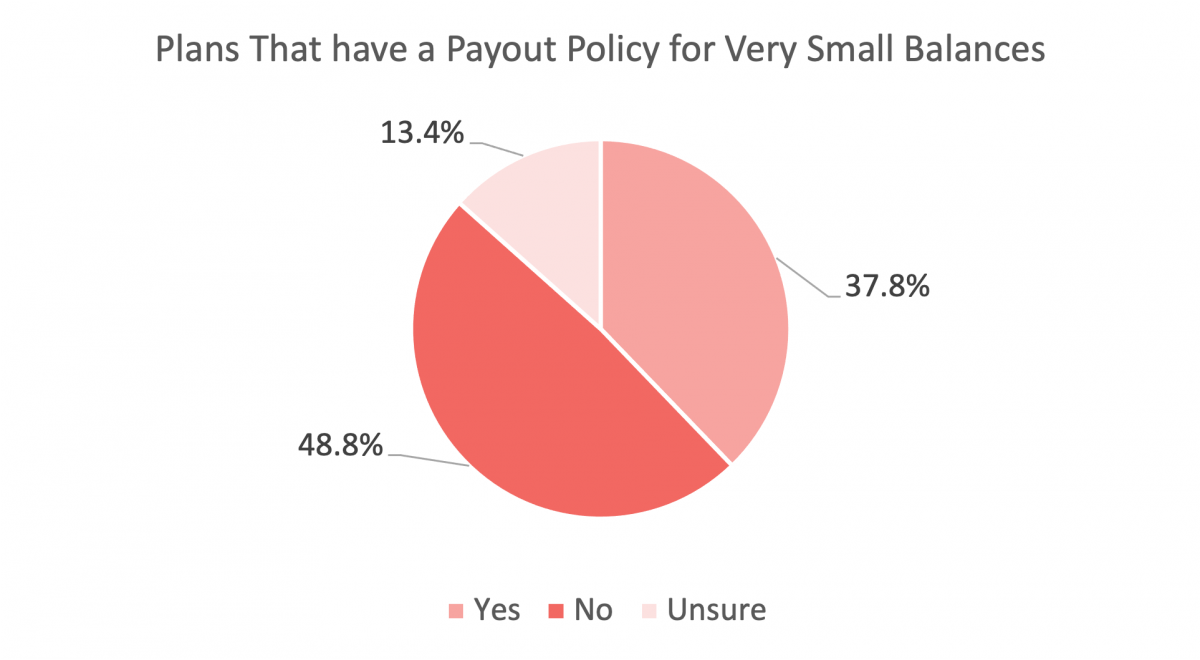

A PSCA member reached out wondering what other plan sponsors do about paying out very small plan balances. They have a significant number of terminated employees with a plan balance less than $10, which is more than it costs to process and distribute the balances, and very often participants don’t cash very small checks which creates an additional administrative burden. We asked members if they have a policy in place regarding this issue in last week’s QOTW. Nearly half of respondents (48.8 percent) indicated that they do have a policy in place and 37.8 percent do not. Several respondents indicated that they have a similar problem but lack clear guidance on what an acceptable cut off limit is.

Comments follow.

- $5.00 or less balances are forfeited.

- Best practice should be to do what's right, not what is most efficient or economical. Therefore, if the policy is to close out small balances, those balances should be sent to the participant.

- Commentary that we have received from our recordkeeper is that clients do this but the law doesn't dictate what to consider diminimus so technically not distributing a penny could put the plan at risk.

- I also would like further guidance on this, I have to track down unclaimed checks for balances of $.49, and I don’t think payouts should be processed for less than a certain dollar amount. I have never been advised of what dollar amount would be acceptable to not pay out. I hope you post the response on this question.

- I believe the monthly fee would eliminate the balance after approximately 4 months.

- I wish we did but I haven't found any clear guidance allowing this except in the case of Plan termination. They get forced out annually but often end up as uncashed checks, another nuisance.

- I'd still pay it out - get them out of the plan counts, etc.

- If employee is active, yes we pay out the balance. If inactive, this is considered forfeiture

- If participant's vested account balance does not exceed $5,000, a distribution of participant's vested account balance will be made to participant, regardless of whether participant consents to receive it, as soon as administratively feasible following termination of employment.

- If the distribution amount is less than the distribution fee, the balance is swept to fees and the account closed.

- If the plan charges a participant record keeping fee the account will be absorbed by the fee.

- If we have a good address we automatically process the distribution, regardless of the amount. If they are a lost participant, and we still can't find them after our normal search process is completed each year, we may forfeit balances under $75 eventually. We take a look at it each year. Also, when doing corrections, depending on the correction, we may forfeit de minimis amounts, as allowed.

- Increase minimum contribution to $100.

- Many complain when they receive their distribution not realizing there are fees that are taken out and don't understand why a check for a minimum amount would be processed to begin with

- Our plan has a minimum account balance requirement for terminated participants of $1,000. Annually, those folks are forced out. The plan can't keep their money.

- Our policy is that when an employee terminates, if their plan contains less than $5000, the amount is paid out. This policy would apply to even very small plan balances.

- Perhaps the small balance definition could be higher, ie: starting at $25...

- Possibly try a limit: 10 years post termination?

- That's a good point. The distribution is paid out by the plan sponsor, so I haven't thought about this.

- The record keeper can easily manage this. I would discuss the options they have available, look at how many are out there, and pick the most cost effective option. Amend the plan and don't worry about it anymore. It also becomes an issue with the lost participants and I don't want to pay to search for people with balances under $10. Get them out of the plan ASAP.

- We actually distribute the balance without regard to the cost. These are infrequent.

- We consider even very small balance payouts to just be a cost of doing business. We also cover the recordkeeping fees for balances under $1,000.

- We consider this a cost of running the plan. Additionally, it is our anticipation that such an occurrence is fairly infrequent so the overall cost to the plan for such distributions is minimal.

- We do not distribute if balance is less than $25 dollars. Because the participants pay the administration fee, the account balance is ultimately reduced to $0.00 after a few months.

- We do not have a policy for paying out very small balances, but this question prompted consideration of it.

- We do not have a process but have many members that have unclaimed checks for less than $1.00 and they refuse to cash them because they are so small.

- We do not pay out small balances.

- We have a De Minimus of $5,000 in where inactive participants are transferred to an IRA with the Plan TPA; however, if the inactive participant has a small balance of $1000 or less, they are contacted via email or preferred contact method on file to notify them that a check will be distributed to them by a specific date. They are given an opportunity to select a Rollover to another qualified plan or to have the money distributed to them via EFT or check. If the inactive participant is not responsive, the funds will be remitted in a check via USPS to the address on file.

- We have a policy that pays out if the balance is under $ 1000 automatically. No reference is made regarding a lower limit so I presume it would be paid out.

- We have a practice when it comes to uncashed checks that are less than $10 but no policy around paying out very small balances beyond the automatic force out process. A change in fee structure charging per capita could be a way to eliminate the small balance.

- We have not discussed this topic with our RK, but will ask at our next meeting.

- We just have it as an automatic upon termination and it is anything under $5000

- We pay it out down to $1

- We payout regardless of how small the amount.

0 Comments

Discussion Policy

Sign In to Comment