Advertisement

A Bucket List for Retirement?

Buckets May Be An Unnecessary Impediment to Retirement Preparation and Spending

Bucket lists for retirement are not solely about places to see and things to do.1 Some financial experts recommend buckets for investment and spending in retirement2, others for investment and saving in preparing for retirement.3 Beware…

Investment and Spending in Retirement

Are we at the cusp of another major market correction – the Great Recession II? Volatility is up. However, volatility is not predictive of market swings – up or down.4

This again is of interest as we acknowledge the 10-year anniversary of the 2008 financial storm. Those who were in their 50s during the Great Recession may be considering retirement today. Many are concerned about retiring in a down stock market. Many are invested in 2020 target date funds - some of which still have 55-60 percent equity allocations.5 Others are concerned about sequence of returns risk.6

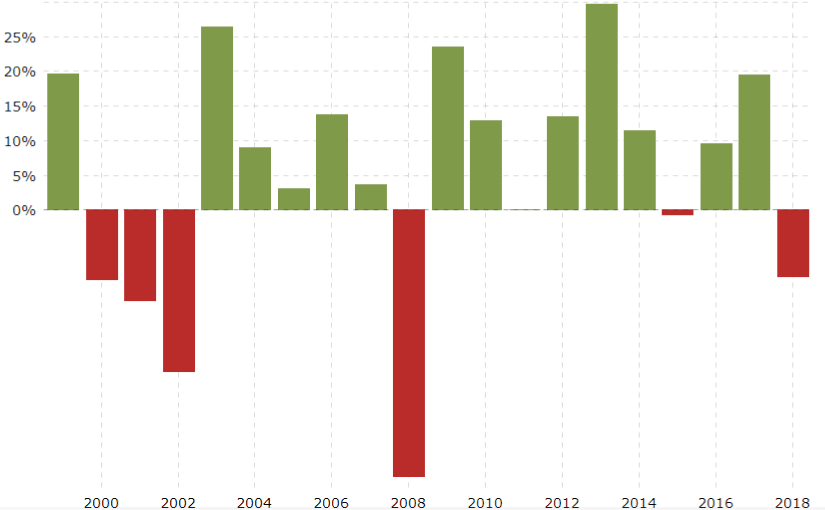

To counter those challenges, some financial experts recommend a bucket approach for retirement savings, preparation, investment, and spending. A bucket you say? Yes, this is a case in which you set aside a few years’ worth of spending in cash or fixed income investments then invest the remainder of the portfolio more aggressively. So, when an investment portfolio suffers a market correction, a retiree uses money from the cash account – so the investment portfolio has time to recover.7 Consider the year-over-year percentage changes in S&P 500 investment performance:

When the market correction occurred in 2008, it took more than four years to fully recover – and only for those who stayed invested in equities, those who stayed the course.

The bucket approach can also be implemented using mental accounting. You allocate/separate assets based on their specific purpose/need. It’s popular, feels good and is plausible. It is easy to implement and it reduces anxiety. But, it is suboptimal:

“The evidence shows that a bucket approach underperforms static strategies; however plausible, comforting, consistent with mental accounting and easy to implement the bucket approach may be, simple static strategies, with periodic rebalancing, and are just as easy to implement and leave retirees better off.”8

Just as important, there is significant upside potential from using a “total return” approach.9

Investment and Saving in Retirement Preparation

A bucket approach or envelope savings system for retirement preparation is an ultra-complex process:

- First, you have to identify all of your savings goals.

- Second, you have to identify how much money you must have for each need, which also involves projecting future prices and inflation.

- Third, you’ll have to identify when you will need those monies.

- Fourth, you will have to identify and select the right “envelope” (savings vehicle), since some investment options have access and penalty limits.

- Fifth, you’ll have to decide on an investment strategy for each need.

- Sixth, you’ll have to evaluate, no less frequently than annually, your progress regarding achieving each goal.

- Seventh, you’ll have to adjust your savings rate and/or adjust your investment allocation for any overage or shortcomings.

And then, what if your goals for savings change? What if “they” “move the goal posts” without asking your permission (such as raising taxes, curtailing Social Security benefits, etc.)? What if you change employers or your employer changes their retirement savings plan’s provisions?

Most importantly, what if you are living paycheck-to-paycheck, so that at the end of each month, before you get to the retirement savings bucket or envelope, all you have left are bills?

Know that workers who live paycheck-to-paycheck need your help. Not only should you discourage them from pursuing a bucket or envelope approach, you also need to reconsider your own plan’s liquidity provisions.10 Make the changes necessary so that workers who live paycheck-to-paycheck can re-deploy their individual account retirement savings plan (401(k), 403(b) or 457) as a holistic, lifetime financial instrument.11

Alas, my recommendation: avoid the bucket! Avoid the bucket!

Note: Some retirement experts use the term “bucket” to separate retirement assets by tax status – Roth (401(k), 403(b), 457(b), IRA), tax deferred (401(k), 403(b), 457(b), IRA), after tax (401(a), employer contributions (401(a)), tax preferred (e.g., Health Savings Account, 223) and taxable (e.g. brokerage, banking, etc.) Each has a different tax treatment – both in terms of the contributions and the distributions. I use/prefer the term “source” to differentiate these various retirement assets. So, when saving and spending retirement assets, incorporating consideration of the tax treatment for each source is important – for both the contribution and the distribution, as well as the impact on the investment portfolio.

1The Bucket List, 2007, Accessed 12/24/18 at: https://www.imdb.com/title/tt0825232/

2C. Benz, The Bucket Approach to Retirement Allocation, Morningstar, 9/19/16 Accessed 12/24/18 at: https://www.morningstar.com/articles/714223/the-bucket-approach-to-retir...

3J. Compton, The ridiculously simple way to save money: envelopes, 5/29/18, Accessed 12/24/18 at: https://www.nbcnews.com/better/business/how-save-money-using-envelope-sy... See also: M. Singletary, Budget By the Old Envelope System, 6/10/07, Accessed 12/24/18 at: http://www.washingtonpost.com/wp-dyn/content/article/2007/06/09/AR200706... See also: R. Cruze, The Envelope System Explained, Accessed 12/24/18 at: https://www.daveramsey.com/blog/envelope-system-explained

4J. Towarnicky, Retirement Investing At The Summit – Investing When Equity Markets Are At All Time Highs, 11/30/18, Accessed 12/24/18 at: https://www.psca.org/blog_jack_2018_54

5All TDFs generally use age 65 as the target date – the date when payouts from the individual account retirement savings plan are expected to commence. However, there are noticeable differences among equity holdings at age 65 – Vanguard at 49%, T. Rowe Price at 55%, Fidelity at 55%. Also, many TDFs use a “through” retirement glide path where equity allocations don’t reach their minimum, the landing percentage, until long after the target date - Vanguard at age 75, Fidelity at age 80, T. Rowe Price at age 95. See: R. Wohlner, Target Date Funds Comparison – Aren’t They All The Same? 8/22/18. Accessed 9/17/18 at: https://investorjunkie.com/48359/target-date-funds-comparison/

6M. Kitces, Retirement Date Risk – The Impact Of Sequence Of Returns Risk On Those Still Accumulating For Retirement, 2/24/16, Accessed 12/24/18 at: https://www.kitces.com/blog/retirement-date-risk-how-sequence-of-returns... ; See also: M. Kitces, Understanding Sequence Of Return Risk – Safe Withdrawal Rates, Bear Market Crashes, And Bad Decades, 2/24/16, Accessed: 12/24/18, https://www.kitces.com/blog/understanding-sequence-of-return-risk-safe-w... See also: M. Kitces, How Do You Actually Create A Steady Retirement Paycheck From A Volatile Retirement Portfolio? 10/31/18, Accessed 12/24/18 at: https://www.kitces.com/blog/retirement-paychecks-diversified-total-retur...

7M. Kitces, The Portfolio Size Effect And Using A Bond Tent To Navigate The Retirement Danger Zone, 10/5/16. “This allows the portfolio to take shelter in the tent during the riskiest years of being exposed to the portfolio size effect – not because bonds have an appealing return, but simply because they reduce the volatility risk that becomes so severe at the portfolio’s maximal size. “ Accessed 2/21/19 at: https://www.kitces.com/blog/managing-portfolio-size-effect-with-bond-ten...

8J. Estrada, The Bucket Approach for Retirement: A Suboptimal Behavioral Trick?, 12/8/18, Accessed 12/24/18 at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3274499

9M. Kitces, The Extraordinary Upside Potential Of Sequence Of Return Risk In Retirement, 2/20/19, Accessed 2/21/19 at: https://www.kitces.com/blog/url-upside-potential-sequence-of-return-risk...

10J. Towarnicky, Impediments to Saving for Retirement – The Barriers, Part 1, 11/5/18, Accessed 12/24/18 at: https://www.psca.org/blog_jack_2018_50 See also: J. Towarnicky, Impediments to Saving for Retirement – The Solutions, The Right Kind of Liquidity, Part 2, 11/9/18, Accessed 12/24/18 at: https://www.psca.org/blog_jack_2018_51

11J. Towarnicky, My Financial Wellness Solution: The 401(k) as a Lifetime Financial Instrument, 2017, https://www.soa.org/essays-monographs/financial-wellness/2017-financial-...