Advertisement

But I Repeat Myself–You Should Offer a Fully-Insured, Retiree-Pay-All, Employer-Sponsored, Medicare Advantage Option to Retirees

Yes, yes, yes … offer both an HSA-capable option to workers1 and a Medicare Advantage option to retirees.

While many American workers live paycheck to paycheck, almost all can afford to contribute to the employer sponsored retirement savings plan and to a health savings account. It is the exception when a worker’s medical expenses, student loans and other debts preclude saving.2 So, yes, I believe every employer should provide access to plans that qualify for tax preferences – individual account retirement savings plans like the 401(k), HSA-capable medical coverage and Medicare Advantage options. When those and other benefit options are offered, “people have within their own hands the tools to fashion their own destiny.”3

Why Offer a Fully-Insured, Retiree-Pay-All, Employer-Sponsored Medicare Advantage Option?

Needs/Lifetime Medical Spending of Retirees: Retiree medical premiums and out-of-pocket expenses have been described as “tail risk,” a catchphrase for a dramatic outlier event that upends the best laid plans for retirement.4 Cost estimates vary; one estimate is an average of $122,000 (age 70 to death), while another is $280,000+ for a couple, both age 65 and eligible for Medicare in 2018 (excluding potential costs from Long Term Care).5 No matter the estimate, we’re talking big money here.

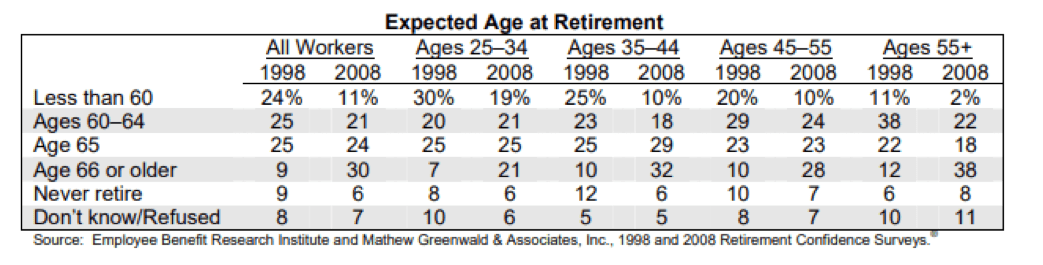

Facilitate Retirement Decisions: More and more workers are planning on working past age 65, with 57 percent citing access to health insurance as a primary reason.6

When surveyed, employers confirmed that facilitating orderly retirement is important – 83 percent indicated a need for the “orderly transfer of knowledge,” 60 percent have “concerns over workforce productivity” and about one-third pointed to “roadblocks in promoting younger employees,” -while costs were cited by just 20 percent of surveyed employers.7 However, anecdotal discussions with employers/plan sponsors often cite cost as a top issue for workers who delay/defer retirement.8

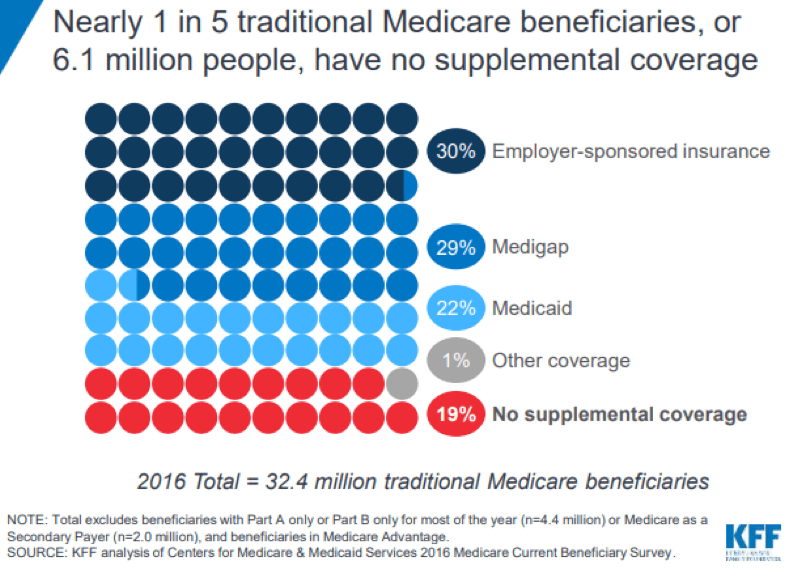

Coverage Supplemental to Medicare: Most retired workers and their spouses are eligible for and enrolled in Medicare. However, according to a Kaiser Family Foundation Report, only 81 percent of retirees in traditional Medicare purchased Medicare Supplement coverage in 2016.9 Obviously, many millions of retirees have decided to self-insure the risk of out-of-pocket expenses.

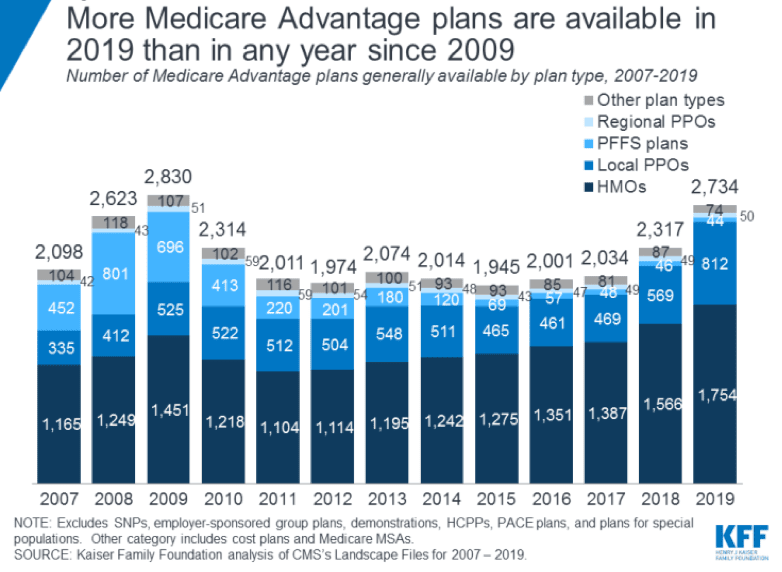

For comparison, almost all Medicare Advantage fill some/all of the point of purchase cost sharing gaps in traditional Medicare. In 2019, 2,734 Medicare Advantage plans will be available nationwide - an 18 percent increase (417 more plans) from 2018 and the largest number of plans available since 2009.10 Many of these same options are available as employer-sponsored coverage options through an exchange.

Why?

Why fully insured? So that there is no risk to the employer.

Why retiree-pay-all? So that there is no retiree medical liability under FAS 106 / FAS 158.

Why employer-sponsored coverage? So a retiree’s payment of premiums will be eligible for tax free reimbursement using HSA assets. For comparison, premiums for individual Medicare Supplement coverage (not sponsored by the employer) are not currently eligible for tax-favored reimbursement using HSA assets.11

Why Medicare Advantage? A number of programs are already in place that employers can adopt which offer a choice of Medicare Advantage options.12

Anything else? Yes, the employer can limit access to this retiree coverage by defining eligibility criteria, or who is a “retiree.” Some employers adopt minimum age and completed service requirements. Further, an employer may expressly condition enrollment in this alternative retiree coverage on the qualified beneficiary’s waiver of COBRA coverage, and, the employer can limit the offer of retiree coverage only to those who waive COBRA.

I leave you with a better question - Why Not?!13

1J. Towarnicky, But I Repeat Myself – You Should Offer a Health Savings Account-Capable Health Option, 10/12/18, Accessed 12/19/18 at: https://www.psca.org/blog_jack_2018_47

2J. Towarnicky, Impediments to Saving for Retirement – The Barriers, Part 1, 11/05/18, Accessed 12/18/18 at: https://www.psca.org/blog_jack_2018_50

3Murray D. Lincoln, Vice President In Charge of Revolution, McGraw-Hill, 1960

4C. Farrell, The Truth About Health Care Costs In Retirement, Forbes, 6/28/18, Accessed 12/18/18 at: https://www.forbes.com/sites/nextavenue/2018/06/28/the-truth-about-healt...

5Fidelity, A Couple Retiring in 2018 Would Need an Estimated $280,000 to Cover Health Care Costs in Retirement, 4/19/18, Accessed 12/19/18 at: https://www.fidelity.com/about-fidelity/employer-services/a-couple-retir...

6J. McDonald, Expected Age of Retirement … and Working in Retirement, EBRI, 6/11/18. “… the percentage planning to retire at age 66 or older has increased for almost every age group. …” Accessed 12/19/18 at: https://www.ebri.org/docs/default-source/fast-facts/fastfact_86-rcs4_11j...

7J. Manganaro, Employers Struggling to Understand Retirement Patterns of Employees, 12/13/18. “Most organizations appear to underestimate the financial challenges facing older workers, and thus the likely timing of retirements, Willis Towers Watson says.” Accessed 12/19/18 at: https://www.plansponsor.com/employers-struggling-understand-retirement-p...

8Mass Mutual, Is delayed retirement impacting your bottom line? 2017, Accessed 12/19/18 at: https://wwwrs.massmutual.com/retire/pdffolder/rs9342.pdf, See also: Prudential, Why Employers Should Care About the Cost of Delayed Retirements, 2017, Accessed 12/19/18 at: https://www.prudential.com/media/managed/documents/rp/SI20_Final_ADA_Cos...

9J. Cubanski, A. Damico, T. Neuman, G.Jacobson, Source of Supplemental Coverage Among Medicare Beneficiaries in 2016, Kaiser Family Foundation, November 2018. Accessed 12/19/18 at: http://files.kff.org/attachment/Data-Note-Sources-of-Supplemental-Covera...

10G. Jacobson, A. Damico, T. Neuman, Medicare Advantage 2019 Spotlight: First Look, 10/16/18, Accessed 12/19/18 at: https://www.kff.org/report-section/medicare-advantage-2019-spotlight-fir...

11IRC §223(d)(2)(C)

12T. Beaton, Employer-Sponsored Medicare Advantage Enrollment Up 12% for 2019, 11/7/18, Accessed 12/19/18 at: https://healthpayerintelligence.com/news/employer-sponsored-medicare-adv...

13Your comments regarding this blog post are welcomed and encouraged – email me at: [email protected].

We are providing this information to you solely in our capacity as individuals with knowledge and experience in the retirement industry and not as legal advice. The issues presented here may have legal implications. We recommend discussing these matters with your legal counsel before choosing a course of action. This memorandum (email, publication, etc.) was prepared to support the informational needs of the Plan Sponsor Council of America on the issues discussed. If this memorandum is shared, recipients should understand that (1) the memo focuses on the needs of our association and the issues of interest to association members, and (2) it is not (and you/others should not use it as a substitute for) legal, accounting, actuarial, or other professional advice. IRS CIRCULAR 230 NOTICE: Any advice contained in this document was not intended or written to be used, and cannot be used by the recipient or any other person, for the purpose of avoiding any Internal Revenue Code penalties that may be imposed on such person [or to promote, market or recommend any transaction or subject addressed herein]. Recipients of this document should seek advice based on their particular circumstances from an independent tax advisor.