Advertisement

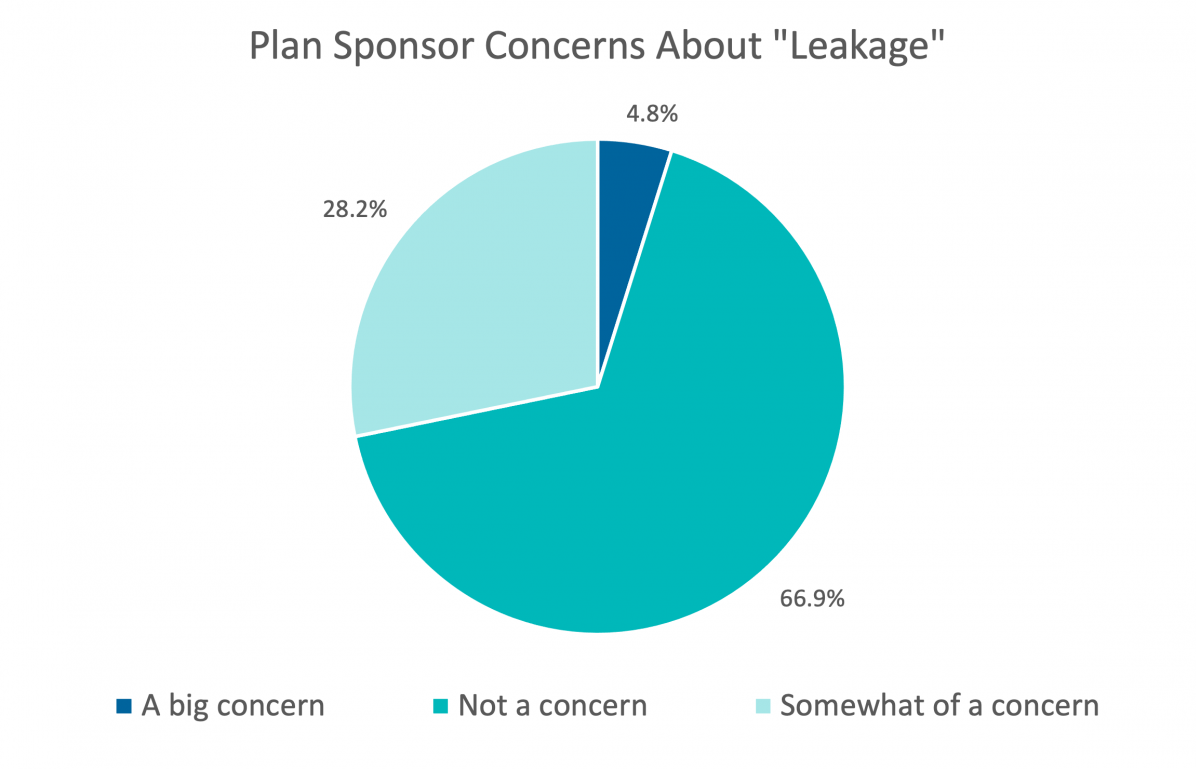

Leakage: A Big Concern but Not a Big Problem

Sponsored by MFS Investment Management.

We hear a lot of concern in the industry about leakage from the system in terms of loans, distributions, and missing participants and there are some solutions underway to help address it (particularly with automatic rollovers). We can recognize “leakage” from the system in terms of cash outs, loans, and missing participants as a concern at the macro level, but I wondered how much of a concern/problem it is at the individual plan level. Is this something plan sponsors are trying to address?

As one respondent very clearly stated it, “It is a big concern, but not a huge problem.” And that I think sums it up, and as you see in the comments below, some sponsors are concerned about participants using their retirement accounts as spending accounts and not saving enough for retirement, but in terms of plan administration, it is not really a problem. Some plan sponsors proactively address it by not allowing loans or withdrawals at all, or restricting access.

- Although we have had no more than 1-2 loans outstanding at a given time, we view 401(k) loans as a terrible idea and truly robbing from the employee's future.

- CARES Act Withdrawals, Loan defaults post separate, overuse of 401k loans.

- Demand for loans/distributions for our plan are very low.

- Distributions based on separations (e.g. rollovers out of the plan). But we get a lot coming in as well so we have balance.

- Don't have loans, lots of terminated people leave $ in plan.

- Employees not taking saving for retirement seriously. They want the money now.

- Excessive in-service distributions are a concern.

- Hardship and 59 1/2 withdrawals

- Hardship withdrawals

- Hardship/CARES Act withdrawals

- Hardships and Loans

- I believe that times are hard and inflation caught everyone. I see loan requests more frequently than before.

- I don’t get too concerned until loans hit 2% if assets. We’re not there and stay pretty steady.

- I'm not concerned right now. I think individuals who are taking money from the plan are attempting to pay off items while they have the money and are able to do that, rather than wait for everything to crash.

- In-service age 59.5 cash withdrawals, hardship distributions and participants who consistently apply for a new loan once they are eligible.

- It was never a concern before, but has become a little concerning recently only because we've experienced a few employees withdraw money. One example - an employee took early withdrawals (over 59 1/2) so not as concerning. Another example is one employee who has taken a few hardship withdrawals over the last couple years but we're not certain what is happening in their personal financial situation to necessitate it.

- It's just a bad financial decision

- Just taking the opportunity and the impact on the long term investments. Loan rates are especially high at this time.

- Leakage is more of a concern from the fiduciary standpoint, than generally for our Plan. And mostly from participants leaving and cashing out balances.

- Loan defaults

- Loans & pre 59.5 distributions

- Loans and cash out distributions. We do not allow any type of hardship and we have restrictions on loans, but there are still too many taken for non-emergency reasons (IMO).

- loans, we are double of our competitors with employees continuing to take loans.

- Lots of loans being taken, many of which default.

- No participants have taken any type of withdrawal since the start of our plan in 2020.

- One employee using his balance like a rainy day savings account

- Our loan and distribution activity changed very little in the past 3 years. Not an issue for us.

- Our loan and withdrawal activity appears to be in line with what is happening with peers.

- Our number of loans/withdrawals have remained steady, so no major concern at this time.

- Our plan does not have many loans or distributions.

- Our plan does not include Loans, but over the last 2 years we have had a large increase in hardship withdrawals.

- participants with large account balances retiring

- People who take serial loans

- plan does not offer loans

- Ptpts can use this plan as a 'savings' option instead of for retirement; but this is just a bigger "root cause" issue of people simply not saving money, period.

- Really haven't had inquiries or increased loan or withdrawal requests.

- Retirement planning is only one piece of the financial landscape. How are we to know if an employee is prioritizing putting a roof over their head, food on the table or debt consolidation over retiring in a couple decades? I'm more concerned about ensuring participants have the tools to understand the impact of their decisions (taxes, penalties, missed growth, etc)

- SECURE 2.0 withdrawal flexibility will make leakage a larger issue for plans. We are treading carefully on the optional features.

- Several years ago we addressed loan leakage by changing loan policy to only allow 1 loan at a time; down from 2. This helped.

- Since COVID, employees are taking out multiple loans/distributions and are going to be ill prepared for retirement as their plan balances shrink. If the government could create a qualified pre-tax emergency loan through employer payroll deductions, this could reduce the use of 401ks as payday loan vehicles.

- The 401(k) is meant to accumulate assets for retirement. There is a concern that participants may take start to withdraw funds from their 401(k) plan instead of looking at other options to fund daily expenses.

- The CARES Act provided participants with a way to withdraw a large amount of money from their 401(k).

- Its a big concern but not a huge problem. The driving concern is the retirement readiness of our employees who live paycheck to paycheck. Catastrophic events find them draining their retirement accounts.

- The fact that many of our employees don't have an emergency savings account is the biggest driver for us laxing our approach and concern around leakage.

- There haven't been a lot of loans or pre-retirement distributions.

- There not that many loans, therefore not a concern

- Too many loans and hardship withdrawals mostly from employees under 50. Many employees see their 401k as a savings account and not as a retirement account.

- tracking missing participants. Other: : Not much, but there are few participants who constantly take loans. When they pay one loan, they take another one.

- Very few loans right now (only one out of 70 employees).

- Very few participants take a loan.

- Very little usage of loans or hardship withdrawals among our participant base.

- We at this point do not have a large amount of loans taken out, but given the economic environment I could see it getting worse.

- We did see a slight increase in the number of participants requesting loans, especially during the pandemic, but conversely, we have also seen an increase in the number of participants which is encouraging

- We do allow hardship withdrawals, but we do not allow loans.

- We do not allow loans

- We do not foresee much activity on withdrawals.

- We do not offer loans and the only distributions allowed are for those over 59 1/2 or to person's leaving the company,

- We don't offer loans

- We don't offer loans. Majority of distributions are from terminated employees.

- We don’t offer loans on our plan

- We have a large number of employees with loans and have had 2 defaults in the past 18 months.

- We have eliminated loan provisions and focused our team that the 401k is a retirement vehicle and not a funding vehicle for shorter term goals. Hardship withdrawals are still permitted. These actions have reduced leakage and our participation numbers are still high.

- We have low usage.

- We have very few distributions

- We have very low loan utilization. We let people take loans but we offer it with education. We also let our terminated participants take out new loans - we'd rather that they have the option to pay themselves back for retirement than see permanent leakage.

- we haven't had any loans or withdrawals

- We haven't seen a change in the number/amount of loans and/or distributions

- We normally have a handful of loans which are paid back per schedule, no defaults. Distributions from the plan have only been RMDs which is to be expected and, for the most part, have only been for the RMD amount.

- We only allow certain hardship distributions, no loans. While the utilization is up from prior years, when we look at it as a total of plan assets, it doesn't amount to much.

- We only allow one loan outstanding at a time, and we don't allow hardship withdrawals, so under normal circumstances, it is not a major problem. However, hurricane harvey and CARES Act provisions opened up the floodgates, and I believe that there were a number of our lower-paid employees who raided their retirement for unrelated problems, and will not have what they need at retirement because of it.

- We only have 1 loan and did not adopt any Cares act provisions and have no hardship. Concern is they are repeat loan takers.

- We rarely have loan defaults so no concern there. Quite a few smaller balances get cashed out however and if there was an option available to us from our recordkeeper to use auto-portability to roll to another employer's plan we'd be interested in helping participants preserve their retirement savings.

- We still have a good amount of termed employee balances and missing participants.

- We trust our record keeping company to maintain the data integrity.

- While we have several "repeat" loan takers, we rarely have any defaulted loans. Terminated employees with larger balances tend to leave their balances in the plan rather than move them elsewhere.

- Withdrawals and defaults are not material at this time.